Choosing Between ACH and Wire Transfers for Business and Personal Payments

Are tedious payment reconciliations slowing down your finance team's close process?

Whether you're processing high-volume payroll via ACH or handling urgent, large-value wire transfers, the payment method chosen significantly impacts your back-office workload.

Understanding the fundamental ACH vs wire transfer differences—mainly how each demands a distinct reconciliation approach—is critical. Getting this right saves valuable time, reduces unnecessary transaction fees, and prevents costly accounting errors.

In this blog, we will demystify ACH and wire transfers. We’ll explore how they function and highlight the key differences in their reconciliation processes.

What is an ACH Transfer?

Automated Clearing House or ACH is an electronic network that processes large batches of credit and debit transactions for U.S. monetary institutions. It functions like a digital highway for bulk traffic, not single journeys.

ACH's main feature is its batch processing. Transactions are collected, sorted, and processed together at specific times throughout the day. This pooling makes it highly cost-effective, particularly for recurring or non-urgent payments. But, it's also where reconciliation challenges can surface, as payments often arrive grouped, sometimes lacking distinct reference details needed for straightforward matching.

Millions of businesses rely on ACH for payroll direct deposits, vendor payments, and customer debits precisely because of this efficiency. Evidence of its scale? NACHA, the governing body for the ACH network in the US, reported processing over 33.6 billion payments worth $86.2 trillion in 2024 alone.

What this blog covers:

- What ACH transfers and wire transfers are and how they differ

- Key factors: cost, speed, availability, settlement, usage

- When to use ACH vs when to use a wire transfer

- Risks and considerations for both payment methods

- How automation and reconciliation tools (like Osfin) support both ACH and wire workflows

Read More: ACH transfers Explained: How They Work and Why Reconciliation Is Essential

How ACH Transfer Works?

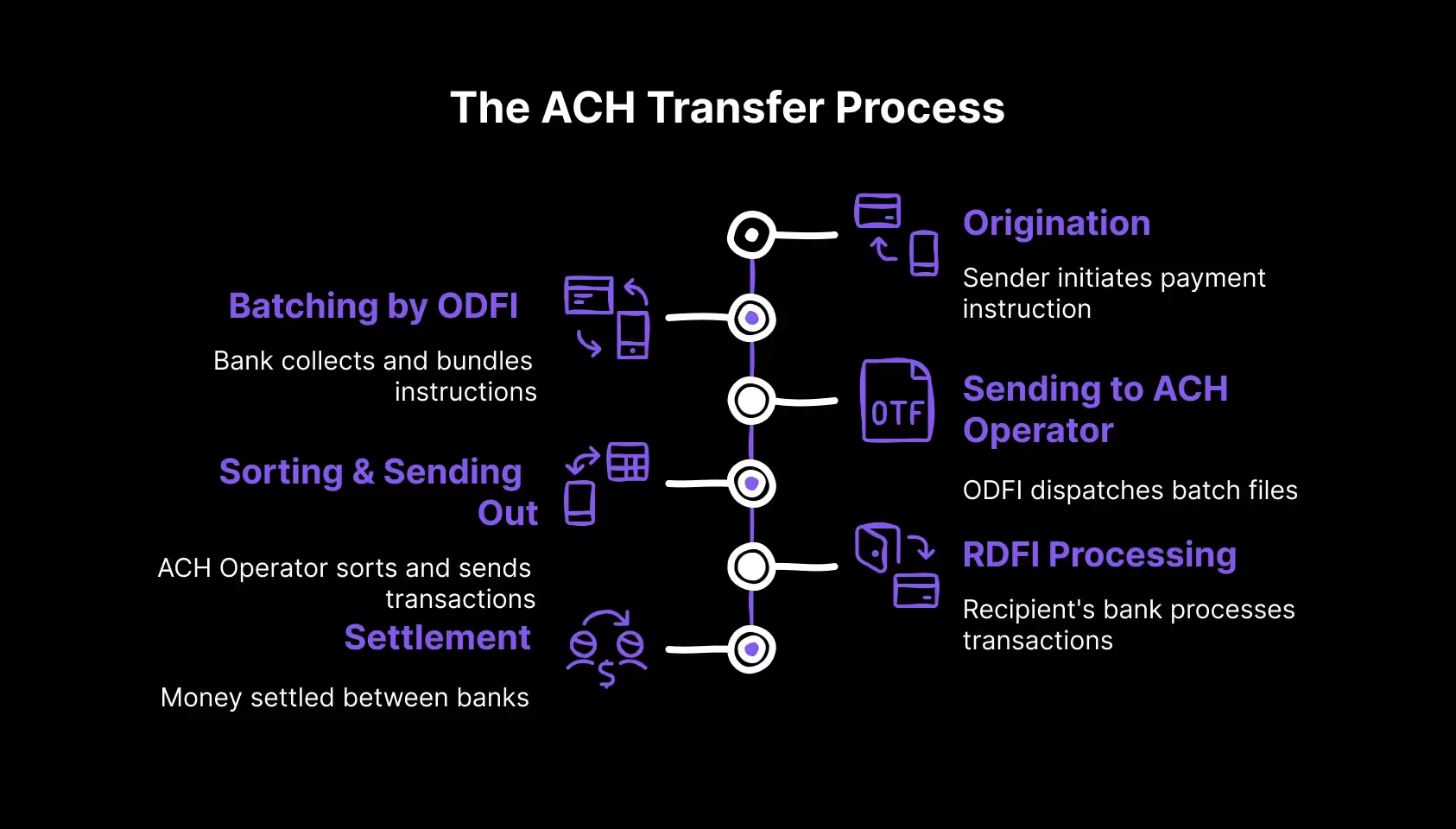

Understanding the ACH flow helps clarify why reconciliation differs from wires. The process generally follows these steps:

- Origination: The sender (Originator – e.g., your company paying a vendor) initiates the payment instruction, usually through their bank (Originating Depository Financial Institution—ODFI). This instruction includes details like the recipient's account number, routing number, amount, and often a reference code or remittance information.

- Batching by ODFI: The Originator's bank collects this instruction and many others throughout the day and bundles them into batch files.

- Sending to the ACH Operator: At set cut-off times, the ODFI dispatches these batch files to an ACH Operator, like The Clearing House (TCH) or the Federal Reserve (Fed).

- Sorting & Sending Out: The ACH Operator sorts the transactions by the bank they’re headed to (the Receiving Depository Financial Institution, or RDFI) and sends the right batches to each one.

- RDFI Processing: The recipient's bank gets the batch file and processes the transactions, adjusting customer accounts (like crediting a vendor's account) accordingly.

- Settlement: The money gets settled between the banks, usually the next business day or two, although you can use same-day ACH for quicker transfers.

Example: Imagine your company processing payments to multiple suppliers. On Wednesday evening, the finance department initiates ACH payments for 150 vendor invoices. The company's bank (ODFI) creates a batch file with these payments and sends it to the ACH Operator overnight. The Operator sorts payments by the vendors' banks (RDFIs), and by Thursday, the credits begin appearing in the vendors' accounts.

Reconciliation: The finance team sees a large debit for the entire vendor payment batch and must match this single line item to the detailed accounts payable file listing all 150 individual payments.

Similarly, if your company receives multiple ACH payments from various customers, they might arrive grouped, needing careful review of sender details and reference information. It helps match them with the corresponding outstanding invoices in accounts receivable.

What is a Wire Transfer?

A wire transfer is a faster method for moving money between banks, occurring almost in real-time. Unlike ACH, which processes transfers in bulk, wire transfers are done individually and are more expensive.

Wire transfers are mostly used for critical transactions, such as housing security deposits, business exchanges, or sending money abroad in emergencies.

In the US, the Federal Reserve Wire Network (Fedwire) handles domestic wire transfers. For international transactions, it’s all about SWIFT, the messaging system that lets banks globally exchange messages and payment instructions securely. These networks streamline fund information sharing between banks and financial institutions, making the process quick and efficient.

How do Wire Transfers Work?

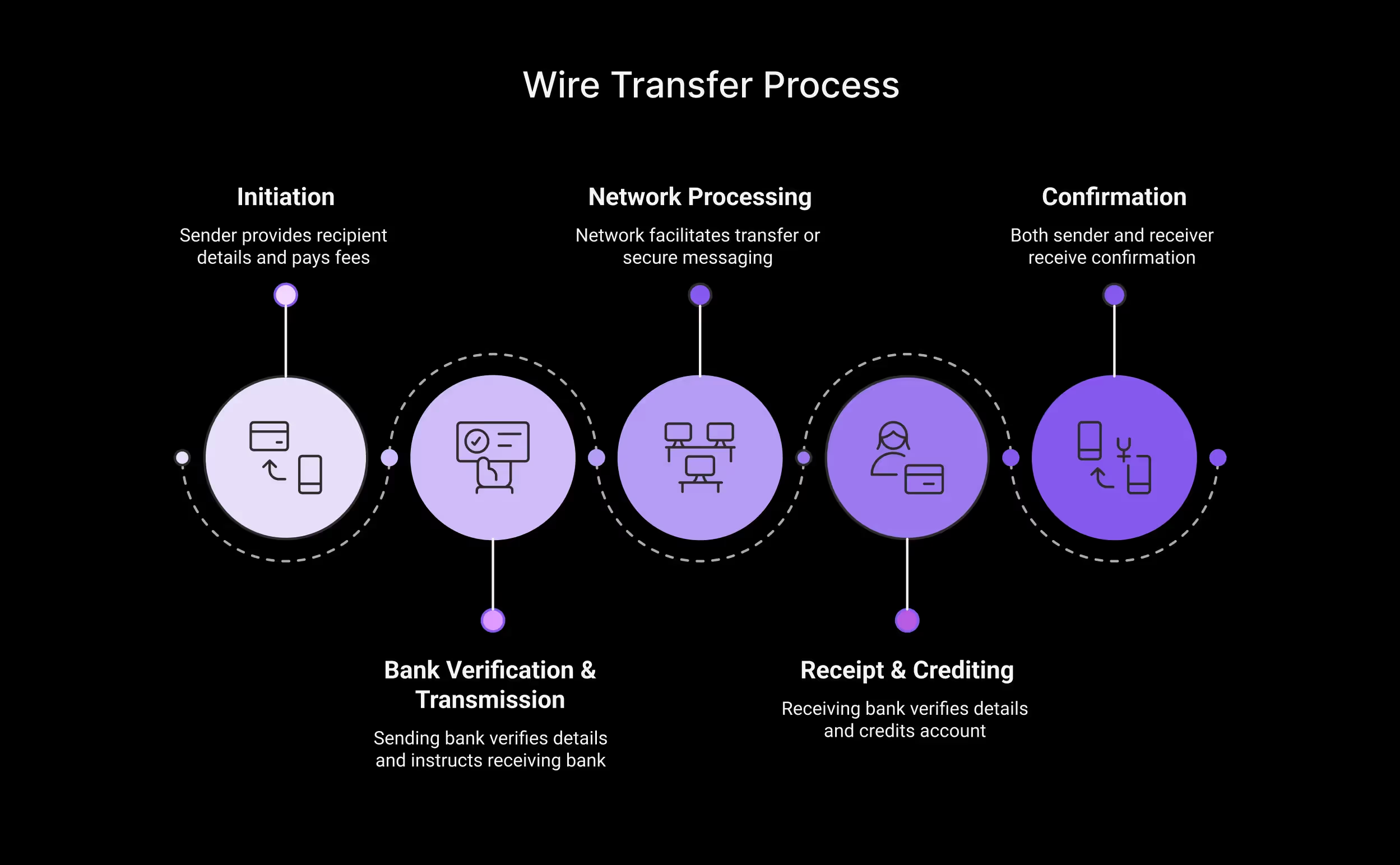

The wire transfer process is more direct:

- Initiation: The sender goes to their bank (or uses online banking) and provides the recipient's banking details (name, account number, IFSC/SWIFT code), the amount, and often a specific reference or purpose for the payment. They also pay the associated wire fee.

- Bank Verification & Transmission: The sending bank verifies the details and confirms the sender has sufficient funds. They then directly instruct the receiving bank, usually via a secure network like Fedwire or SWIFT, to credit the recipient's account.

- Network Processing: The network (Fedwire/SWIFT/RTGS) facilitates the immediate transfer of funds or secure messaging between the banks.

- Receipt & Crediting: The receiving bank gets the instruction and the funds (or confirmation via SWIFT message). They verify the recipient details and credit the amount to their account.

- Confirmation: Both sender and receiver typically get confirmation relatively quickly that the transfer is complete. This process usually happens within the same business day, often within hours, especially for domestic wires.

Example: Your business needs to make a large, time-sensitive payment to an international supplier by EOD to release an urgent shipment.

You request your corporate bank to initiate a transnational Wire Transfer via SWIFT, providing the supplier's bank details, the exact invoice amount, and the invoice number as a reference. After paying the wire transfer fee, your bank sends the instructions and funds directly to the supplier's bank via the SWIFT network.

The supplier's bank credits their account, typically within hours or by the next business day, depending on time zones and correspondent banks, and you receive a unique transaction reference number as proof of the transfer.

Reconciliation: It is simpler for wire transfers, as both parties see a clear, distinct transaction on their statements. The unique reference number (Fedwire/SWIFT reference) makes it simple to match the received payment to a specific invoice or expected transfer. Such guarantees a direct one-to-one match, like confirming receipt of an express courier package.

What are the differences between ACH and wire transfers?

Both send money electronically, but the core differences between ACH and wire transfers exist in their tracking methods. Knowing these differences improves financial process management..

Wires enable quick, often same-day, international transfers but can be costly (5$ - 50$+). Conversely, ACH transfers, typically slower (1-3 days), are much cheaper and suited for local, smaller payments. ACH offers some reversibility and comprehensive data, while wires are final once processed and ideal for large transactions. ACH is predominantly used in the US, with wires used globally.

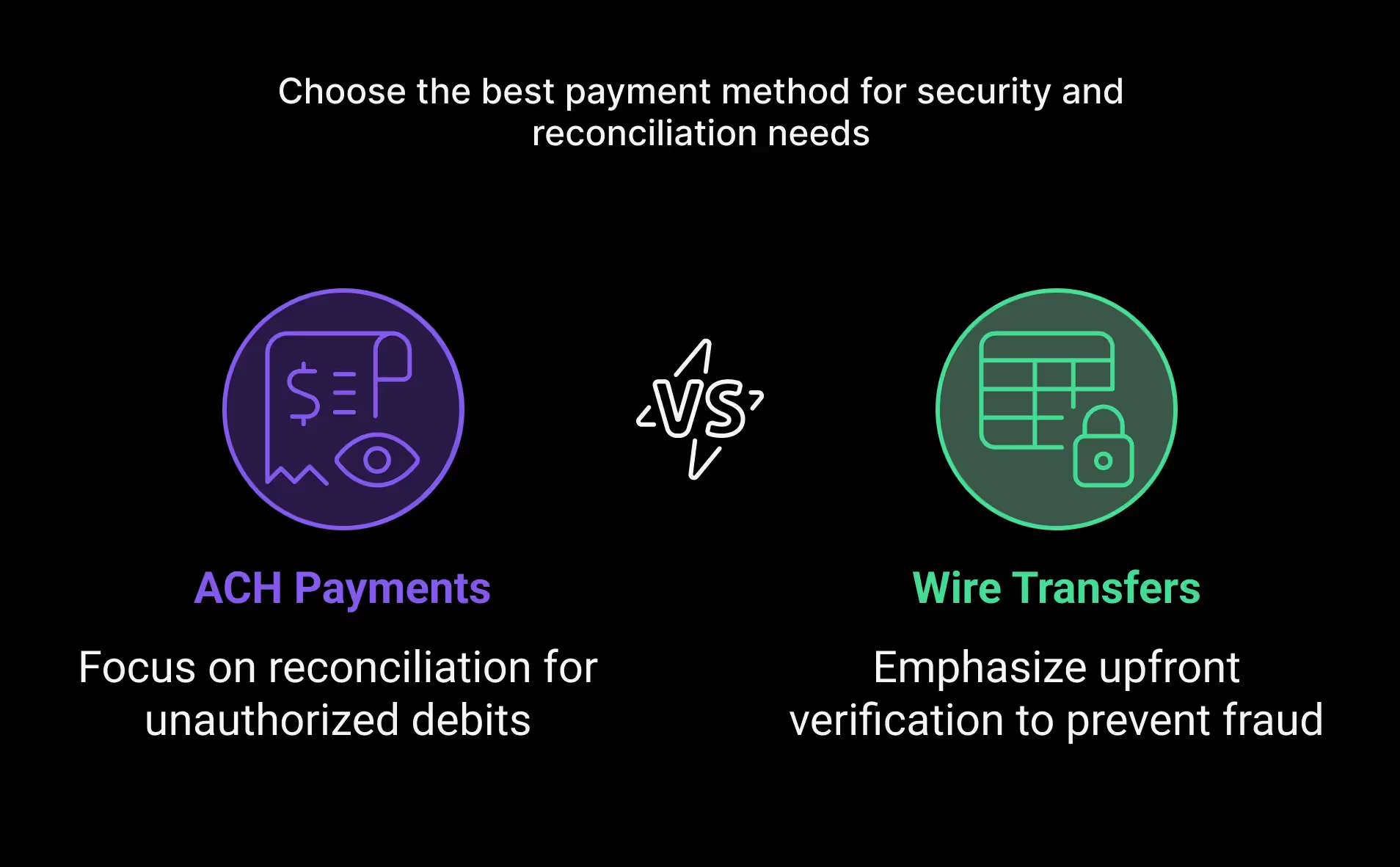

How Secure are ACH Payments & Wire Transfers?

Both ACH and Wire Transfers operate over secure banking networks and are considered safe methods for transferring funds when proper procedures are followed. Financial institutions employ robust security measures, including encryption and authentication protocols.

However, managing the security of these payments is intrinsically linked to diligent reconciliation. Here’s how the risks differ and where reconciliation plays a crucial security role:

- ACH Security: ACH payments carry risks of unauthorized debits. While consumer accounts (PPD marked) have protections with longer reversal windows, businesses using CCD and CTX formats face stricter rules. Keeping account details secure is vital, but timely reconciliation is your first line of defense. Using reconciliation tools allows for faster detection of oddities like unexpected debits, helping to take quicker action within the allowable dispute window. Spotting these quickly is critical.

- Wire Transfer Security: The primary risk here is fraud, especially Business Email Compromise (BEC) scams tricking staff into sending money incorrectly. Because wire transfers are fast and generally irreversible, getting wrongly sent money back is tough. Vigilant upfront verification (confirming details via a known, trusted channel) is paramount before sending. While reconciliation can't reverse a bad wire, automated reconciliation tools quickly confirm legitimate expected transactions (both sent and received), helping to rapidly flag discrepancies or missing funds that might indicate a prior security lapse or internal control issue.

ACH vs Wire Transfer: Differences Summed Up

- ACH: Think volume and value. It's the workhorse for numerous, predictable payments like salaries or recurring bills, where cost efficiency is key. Its batch nature means funds arrive predictably but not instantly. Reconciliation involves potentially matching multiple transactions within batches, requiring good reference data or systems.

- Wire Transfer: Think speed and certainty. It's the express courier for urgent, high-value, or critical one-off payments. You pay a premium for near real-time, direct transfer and finality. Reconciliation is typically straightforward—one wire sent, one wire received, easily matched with its unique identifier.

The pick isn't about which is "better," but which fulfills the transaction's needs for speed, expense, and ease of reconciliation.

ACH vs Wire Transfer: Which is Better for Business-to-Business (B2B) Payments?

Choose ACH (or NACH/NEFT equivalent) for:

- Payroll: Cost-effective and efficient for paying multiple employees regularly.

- Recurring Vendor Payments: Paying regular suppliers with predictable amounts.

- Collecting Customer Payments: Direct debits for subscriptions or services (with authorization).

- Lower Value, Non-Urgent Payments: Where saving on transaction fees is important.

- Reconciliation: Requires robust systems or processes, especially if receiving many ACH payments, to match them using remittance data (if provided) or reference numbers. Software integration is common.

Choose Wire Transfer (or RTGS equivalent) for:

- Large Value Transactions: Paying for major assets, M&A activity, significant inventory purchases.

- Time-Sensitive Payments: Meeting strict contract deadlines or closing deals quickly.

- International Payments: Often the primary mechanism (via SWIFT).

- High-Security Requirement (for Receiver): When the certainty of received funds and finality are paramount.

- Reconciliation: Simpler one-to-one matching, often preferred for high-stakes payments where immediate confirmation and easy tracking are vital. The speed justifies the higher fee, finality, and reduced reconciliation complexity for that single critical payment.

The optimal choice depends on the specific B2B payment scenario. Many businesses use a mix: ACH for routine operations, Wires for strategic or urgent transactions.

Is ACH or Wire Better for Personal Payments?

For individuals, the considerations are similar but scaled differently:

Choose ACH (or UPI/NEFT/IMPS equivalent in India) for:

- Receiving Salary: Most employers use ACH-like systems for direct deposit.

- Paying Bills: Setting up automatic payments for utilities, loans, credit cards.

- Sending Money to Friends/Family (via Apps): Many P2P apps use ACH or similar instant payment rails (like UPI in India) on the backend. These are typically low-cost or free.

- Reconciliation: Usually simple as personal transaction volume is lower. Matching involves checking the sender's name/reference on the statement.

Choose Wire Transfer (or RTGS/International Wire) for:

- Property Transactions: Making down payments or final settlement payments.

- Large Purchases: Buying a car from a private seller who requires immediate, guaranteed funds.

- Sending Emergency Funds: Especially internationally, where speed is critical.

- Reconciliation: Straightforward one-to-one matching, important for confirming large, critical payments have been received. The cost is often a necessary expense for these specific situations.

Cost is often the deciding factor for personal use, making ACH/equivalent methods preferred for everyday transactions, while wires are reserved for significant, urgent needs.

Conclusion

ACH and wire transfers each have their own processes. Sure, speed and cost usually get all the attention, but it’s really about the way they process—batch for ACH and real-time for Wires—that makes a big difference when it comes to reconciling later.

Manually managing these reconciliations, especially at a large scale, can be prone to errors. Osfin.ai simplifies these operations with security and compliance (SOC 2, ISO 27001, PCI DSS). Let’s discuss how we can streamline ACH/wire reconciliation for your finance team.

FAQs on ACH vs Wire Transfer

1. What is the key difference between ACH and wire transfer?

ACH processes transactions in batches, which makes it slower but cheaper. Wire transfers are quicker and more expensive due to individual processing.

2. Is ACH or Wire Transfer faster?

Wire transfers are undoubtedly faster. They complete within hours or the same business day. ACH transfers may take 1-3 days and have limited same-day options.

3. Which is cheaper, ACH or Wire Transfer?

ACH transfers are generally cheaper, often costing nothing at all. Wire transfers typically incur higher fees for expedited transactions through banks.

4. How are ACH payments reconciled?

ACH reconciliation often involves matching a single bank entry (the batch total) against multiple individual payments using reference codes or remittance data provided within the ACH file.

5. Are wire transfers easier to reconcile?

Yes, wire transfers are generally simpler to reconcile. Each wire appears as a distinct transaction, allowing straightforward one-to-one matching using its unique reference number.