Same Day ACH: How It Works and Why It Matters for Modern Payments

In an era where every second counts, the speed at which money moves is incredibly important. As the world becomes more digitized, the demand for immediate access to one's funds has increased significantly for both businesses and consumers. This need has pushed "Same Day ACH" to the forefront as an effective solution that has reshaped modern electronic payments.

ACH, or Automated Clearing House, is a network run by Nacha that allows for a huge number of digital money transfers to occur. The amount of ACH payments, according to Nacha, has surged to $8.5 billion in the first three months of 2025. It has secured its status as a highly effective and safe payment method for everything from salaries to business bills.

As the need for faster processing of transactions is gaining importance, Same Day ACH meets this need efficiently. As Nacha stated, ACH enables payments up to $1 million to be processed in just a few hours, reaching virtually every U.S. bank account. This speed places significant responsibility on financial institutions to ensure that transactions are fast, secure, and accurate.

This article delves into what ACH is, its benefits, challenges, the process, and the future of these transactions.

What this blog covers:

- What Same Day ACH is and how it speeds up ACH transactions

- The processing windows, cut-off times, and settlement schedule

- Dollar limits, rules, and eligibility criteria for Same Day ACH

- Benefits and use cases for businesses and individuals

- Key challenges and risks in scaling Same Day ACH (fraud, reconciliation, bank participation)

- How Osfin automates reconciliation for Same Day ACH with precision and efficiency

- Frequently asked questions about Same Day ACH

Definition of Same Day ACH

At its core, the Automated Clearing House (ACH) refers to a centralized network that allows secure and efficient fund transfer between banks and other financial institutions. It can be thought of as the digital backbone for numerous financial transactions, from direct deposit of paychecks to automatic bill payments like rent to utilities. This network is managed by the National Automated Clearing House Association (NACHA). It sets the rules to ensure smooth and reliable operations for all the financial institutions involved. ACH payments offer a secure and cost-effective alternative to methods such as checks or wire transfers. It also provides flexible settlement options, from same-day to within two business days.

Same-Day ACH is a significant improvement made to the existing ACH network. It was designed to make eligible payments process at a faster rate. Same Day ACH was a response from Nacha to a strong customer and industry demand to replace a 2-3 day transaction process with a same-day service. With Same Day ACH, payments can now be started, processed, and settled all on the same business day, which significantly cuts down on the wait time for funds to be available.

How does Same Day ACH work?

A common question is, how long does Same Day ACH take? To answer that, Same Day ACH is usually completed within a couple of hours. It works by conducting transactions between financial institutions or individuals on the same business day instead of taking 2–3 days. After the sender sends a payment request, the system checks if the account has enough money and looks for issues. If the sender's information is validated, the payment is processed and it reaches the receiver within a few hours. Financial institutions must make sure that their systems can handle fast processing, real-time fraud screening, and near-instant reconciliation to maintain compliance and avoid costly delays.

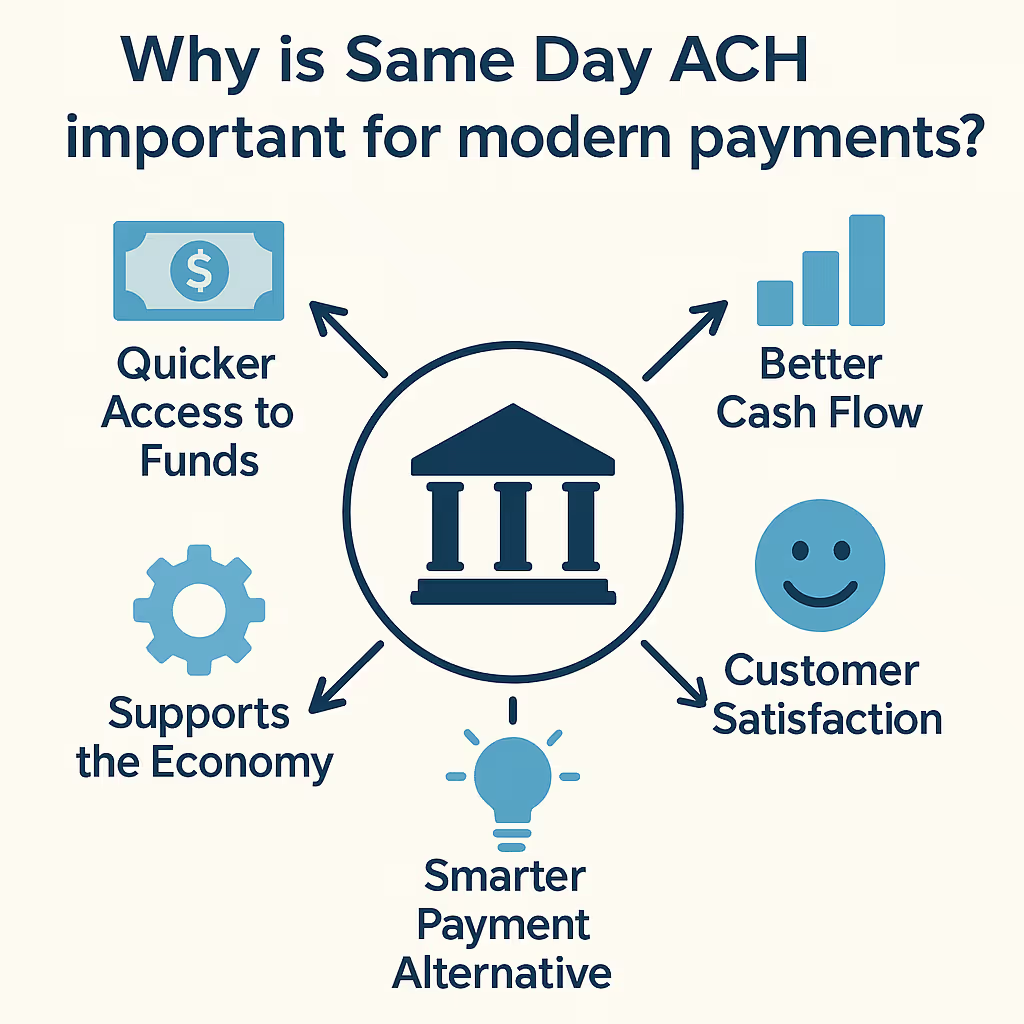

Importance of Same Day ACH in modern financial transactions

Same Day ACH has significantly reshaped how money moves in modern payments, bringing substantial developments and benefits. Its impact is visible in how it addresses the important needs of both businesses and consumers, as well as how it makes financial operations more effective and responsive. Here is why it is so important:

1. Quicker Access to Funds

Customers and businesses are paid much quicker, which improves companies' cash flow and provides individuals with immediate access to funds.

2. Better Cash Flow

Businesses can manage their finances better by receiving payments on the same day they need to make payments to their vendors or employees.

3. Customer Satisfaction

The speed and ease provided by Same Day ACH result in happier customers, which builds loyalty and trust in the financial services of a business.

4. Smarter Payment Alternative

Same Day ACH is usually cheaper than using cards, faster than using standard ACH, and more flexible than wire transfers. This can help reduce costs and manual effort for an organization.

5. Supports the Economy

Since Same Day ACH speeds up payments, businesses can adapt quickly to modern customer expectations and changes in the market.

For any financial organization, managing growing payment volumes properly is important. Osfin's capabilities can help institutions achieve operational excellence and ensure compliance in the fast-moving financial landscape.

Same Day ACH Processing Windows & Cutoff Times

Same Day ACH has three processing windows. The ODFI (Originating Depository Financial Institution) deadlines for each are 10:30 AM, 2:45 PM, and 4:45 PM Eastern Time (ET). The sender’s bank must submit the payment file to the ACH network before these deadlines in order for the payment to be processed through the respective windows. Some companies may have internal deadlines before the actual ACH deadline to ensure that funds are processed smoothly.

The Same Day ACH transfer time depends on when the file is submitted and in which window. If the funds are sent during the first window then settlement happens by 1:00 PM Eastern Time. The second window settlement time is 5:00 PM ET, and for the last window, it is 6:00 PM ET. This means that the money officially moves between banks, and the receiving bank is required to make the funds available to the recipient before the specified deadlines.

Same Day ACH Transfer Limits and Rules

As of now, there are three Same Day ACH processing windows, and the maximum amount for a single Same Day ACH payment is $1 million. The higher amount allows for a greater range of larger payments, which increases its use for businesses and consumers.

If any company misses the last cutoff time, then their payment is considered in the first window of the following day.

Process of Initiating a Same Day ACH transaction

Understanding how Same Day ACH works is important for financial institutions. Same Day ACH speeds up bank transactions by incorporating rapid checks and faster settlement times, at times within hours. Here's how the process looks:

Payment Initiation

The customer instructs their bank (Originating Depository Financial Institution or ODFI) to start a payment. The ODFI then gathers the necessary account details for the sender and receiver of the funds.

Pre-settlement Real-time Checks

The system immediately verifies whether sufficient funds are available in the sender’s account by using live information. It also scans for fraud risks, such as unusual spending patterns, to avoid failed payments.

Transmission to Operator

Once the verification is complete, the ODFI sends the payments to the ACH Operator as a Nacha file. Unlike older, slower ACH methods, Same Day ACH transfers ensure that near-immediate processing occurs within the selected window.

Clearing and Settlement

The ACH Operator forwards the payment file to the receiving bank. Funds are then removed from the sender's account and credited to the receiver's account on the same business day.

Funds Availability

The receiving bank must have the funds ready for the receiver by the settlement deadline of the processing window the sender has used.

Osfin's automation platform helps institutions manage the reconciliation of this high-speed process with 100% accuracy and unmatched speed. It makes things significantly efficient and ensures compliance by automatically handling data from any system or file.

{{banner1}}

Benefits of Same Day ACH for Businesses

Same Day ACH enables financial institutions to transfer funds more efficiently, with payment, operational, and financial planning advantages. It is an important tool for today's organizations. The following are the benefits:

- Faster payment to the customers, employees, and suppliers, which reduces delays.

- Improved cash flow management with same-day fund availability.

- Stronger vendor and supplier relationships through timely payments.

- Reliable processing for employee salaries, especially for gig, contract, or urgency-driven disbursements.

- Faster and cheaper than wire transfers and paper checks.

- Greater flexibility to handle urgent expenses, refunds, or last-minute payouts.

- Better financial control, supporting faster reactions to changes, and tighter timelines.

Use Cases for Same Day ACH

Here are some real-world use cases where Same Day ACH is quite beneficial:

- Payroll - Employees or gig workers can be paid faster. One-time payments, such as bonuses or expense reimbursements, can also be made using Same Day ACH.

- Insurance Payouts - Pay out claims can be sent to people quickly. This allows for faster access to funds for disaster help, refunds, or reimbursements.

- Bank Account Checks - Micro-verification by banks can be made faster by processing small test deposits on the same day.

Challenges in Managing Same Day ACH at Scale

While Same Day ACH has significant advantages, it is also important to be aware of its challenges. Knowing these challenges can help businesses manage their expectations and perform operations effectively.

- Potential for Fraud or Reversals: Although Same Day ACH is secure, it can still be vulnerable to fraud, especially initiated by human error or unauthorized activity.

- Risk of Unsecured Funds: Unlike credit card transactions, ACH payments don't place an immediate hold on the sender's account. This means that even if funds appear available at the time of initiation, they can be moved before the payment settles, creating a risk of non-sufficient funds or failed transfers.

- Variable Speed and Bank Involvement: Not all banks fully support Same Day ACH features. If a customer's bank does not participate, it can lead to slower processing, which defeats the whole purpose of Same Day ACH.

- Difficult Reconciliation: Managing and reconciling large volumes of ACH transactions accurately is a difficult challenge. Same Day ACH also has to follow Nacha's specific rules, which adds layers of complexity to already time-sensitive reconciliation workflows.

Even though there are various advantages, Same Day ACH also comes with certain operational and compliance challenges, such as fraud and bank variability. Financial institutions must be equipped to manage these expectations.

Reliable software solutions like Osfin help banks, financial services companies, and fintechs automate their reconciliation for all ACH transactions. Osfin’s industry-leading 100% accuracy ensures operational excellence and strict compliance with regulatory norms.

{{banner1.1}}

How Osfin Helps Automate Same Day ACH workflows?

Reconciling Same Day ACH transactions requires speed, precision, and real-time control. Since these transactions are complex and deal with a large amount of funds, they don’t leave room for error, and traditional tools cannot handle this fast pace.

That’s where Osfin comes in. It automates the entire reconciliation and reporting cycle to match the needs of modern payment.

Osfin, as a data source and format agnostic platform, connects directly to banking systems, payment gateways, and processors through its 170+ pre-configured integrations. Osfin’s reconciliation automation platform:

- Pulls data in near real-time and matches transactions accurately, even if the currencies or the format in which transaction data is presented are different.

- Matches transactions across systems using rules based AI ensuring 100% accuracy and supports partial, one-to-many, and multi-source reconciliation.

- In the event of any errors, it can identify issues at ingestion and route them for fast exception handling through automated tagging of such issues.

- Live dashboards display unresolved tasks and reconciliation status to help teams respond quickly and confidently.

- Protects reconciliation data using enterprise-level security measures, including 256-bit encryption, role-based permissions, and two-factor authentication, and ensures full compliance with SOC 2, ISO 27001, PCI DSS, and GDPR.

- Offers expert support for faster onboarding and quick resolution of doubts.

- It's a no-code platform that enables institutions to design or modify rules, workflows, and logic without requiring developers.

Same Day ACH is an efficient alternative to standard ACH settlements. It directly meets the demand and need for faster transactions. While it brings benefits like quicker fund access, improved liquidity, and happier customers, it also introduces new operational hurdles, from fraud risks to reconciliation complexity.

With Osfin’s automated reconciliation and real-time reporting capabilities, financial institutions can unlock the speed of Same Day ACH without compromising on control or compliance.

{{banner3}}

FAQs on Same Day ACH

1. What does ACH Same Day mean?

ACH Same Day meaning in context of ACH payments refers to the ability to send and receive payments that are processed and settled within the same business day, offering faster fund transfers compared to standard ACH which typically takes 1-3 days

2. Can Same Day ACH be reversed?

Same Day ACH payments can be reversed, but only in specific cases, such as duplicate payments, incorrect amounts, or unauthorized transactions, as per Nacha rules. Reversals must follow strict timelines and conditions.

3. What is the cut-off for Same Day ACH?

Same Day ACH cutoff time is 4:45 PM ET. The payment files must be submitted by 4:45 PM ET, and processing ends by 6:00 PM EST on business days.

4. How to send Same Day ACH?

The sender initiates the ACH Same Day payments through their bank, which then performs real-time checks, sends the data to the ACH operator, and ensures the money reaches the recipient the same day.

5. What is the maximum Same Day ACH limit per day?

The current maximum Same Day ACH limit is $1 million, making it suitable for large payments.