Bank Reconciliation Problems: Causes and How to Solve Them

Financial reconciliation might sound straightforward, yet it's often a major operational headache.

The root cause behind reconciliation problems at banks?

Millions of daily transactions flow between internal systems such as the CBS and payment switches, as well as external networks and correspondent banks. Each system records data differently and often settles transactions at a different times.

Manually matching these scattered records is slow, error-prone, and risky. These breaks aren't just accounting noise; they represent potential financial exposure, which can lead to hefty penalties, like the $136 million Citibank paid.

Let’s explore some of the core bank reconciliation errors, their origins in complex systems, and understand how modern automation solutions can improve control, accuracy, and efficiency.

What this blog covers:

- The most common bank reconciliation problems and why they occur

- Key issues: timing differences, data silos, high transaction volumes, and duplicate or missing entries

- The impact of reconciliation problems on finance operations, risk, and compliance

- Best practices to diagnose, manage & resolve reconciliation exceptions

- How automation tools like Osfin address and prevent reconciliation breakdowns

What are Bank Reconciliation Problems?

Fundamentally, bank reconciliation is about making sure two sets of books agree.

For a bank, this means comparing internal records the Core Banking System (CBS)’s general ledger with an external data source. It could be a statement from another bank where it holds funds (a nostro account), data from the payment processing switch, or even details backing up an internal suspense account.

Reconciliation issues appear when these records inevitably diverge. These mismatches, known as "exceptions" or "breaks," aren't just accounting typos; they can signal genuine errors, dealings stuck in transit (due to timing differences), missing entries, or even fraud.

It's the often painstaking process of hunting down millions of potential disparities. The steps include interpreting siloed system data, file-swapping to identify mismatches, and executing fixes.

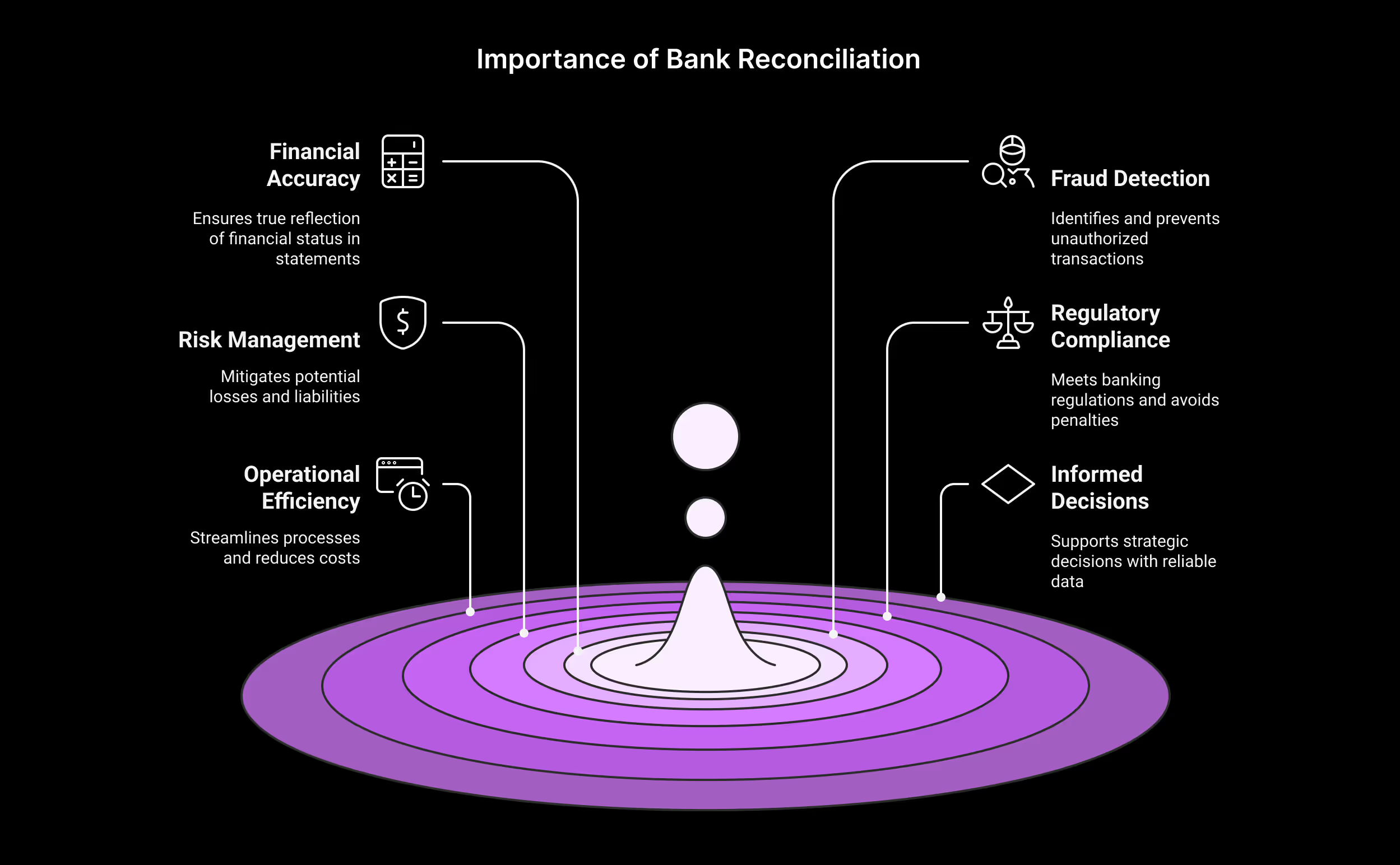

Why is Bank Reconciliation Important?

Reconciliation goes far beyond rudimentary bookkeeping. It’s fundamental to a bank's functional integrity and risk posture and is multi-faceted:

1. Financial Accuracy and Integrity

Accurate reconciliation guarantees that the bank's statements the Balance Sheet and P&Ls reflect the true situation. Uncaught errors can distort profits, misstate asset values, and lead to flawed reporting, affecting investor trust and management decisions. Ensuring complex trades don't inadvertently skew the overall balance sheet picture.

2. Fraud Detection and Prevention

Often, the first hint of unauthorized transactions or internal fraud comes from a reconciliation break. A discrepancy might signal diverted funds or exploited errors. Timely reconciliation acts as a critical internal checkpoint.

3. Risk Management

Every unreconciled item carries uncertainty a potential loss or an unrecorded liability. Leaving these unresolved creates operational risk and financial exposure. Think of it like unquantified counterparty risk; delays in spotting breaks can amplify the eventual financial hit.

4. Regulatory Compliance

Banking regulators demand accurate financial reporting and robust internal controls. Reconciliation processes are heavily scrutinized during audits. Failures can lead to hefty fines and reputational damage; regulators need assurance that the bank has firm control over its assets and liabilities.

5. Operational Efficiency

While flawed reconciliation creates inefficiency, getting it right improves it. Automated processes cut manual work, lower costs, and let skilled units focus on analysis, not routine matching.

6. Informed Decision Making

Solid strategic decisions require reliable data. Whether managing liquidity, setting lending capacity, or determining pricing, management depends on the accurate, up-to-date financial picture that only properly reconciled accounts can provide.

Common Bank Reconciliation Problem Examples

The sheer volume and complexity faced by most mid-to-top-level banks create fertile ground for discrepancies. Here are the most common reconciliation problems they face:

1. Timing Differences

This is a classic issue. Transactions simply hit the books at different times in different systems. Think processing lags, clearing house cycles, or varying daily cut-off times between the bank's internal systems and external parties.

Example: Your bank's Core Banking System (CBS) might process incoming wires until 4 PM. But the correspondent bank (your nostro account provider) processes until 5 PM. Wires hitting the nostro account between 4 PM and 5 PM appear on their statement today, but only land in your CBS tomorrow.

This creates a temporary mismatch a timing difference, not an error. Similarly, settlement files from Visa or Mastercard might arrive hours after your payment switch logged the transaction. It's an inherent feature of an interconnected financial system.

2. Data Silos and Format Inconsistencies

A significant operational headache. Transaction data lives in many separate places: the CBS, payment switches (for cards/ATMs), treasury platforms, various network files (SWIFT, local ACH, card networks). Crucially, these systems often use different data formats, unique identifiers, and capture varying levels of detail.

Example: A credit card transaction gets logged instantly in the switch (with its ID). Days later, it appears in a large network settlement file (with a different reference number, maybe bundled with fees). Finally, the net amount is posted to the customer's account in the CBS (perhaps lacking granular merchant data).

Manually linking these three disparate entries switch log, network file line item, CBS posting using potentially different keys across systems is a recipe for errors and slow investigations. It happens because these systems often grew organically or were bolted together over time.

3. High Volume of Transactions

Large banks handle millions, sometimes tens of millions, of items daily. Manual comparison, even on a sample basis, becomes practically impossible and statistically unreliable.

Example: Reconciling daily ATM cash withdrawals means matching switch records against cash replenishment data and CBS postings for potentially hundreds of thousands of transactions across thousands of machines.

Even a minuscule error rate translates into thousands of exceptions needing manual review.

4. Manual Data Entry Errors

The human element is always unavoidable. Mistakes happen during manual input: transposing numbers ($152 vs. $125), keying wrong account details, incorrect amounts, or miscategorizing entries.

Example: An operations clerk manually processing a small international payment types the beneficiary account number incorrectly. The error likely surfaces only during reconciliation when the internal payment record doesn't match the nostro bank's debit confirmation, triggering an investigation.

These often occur under deadline pressure or where automation hasn't fully replaced manual steps.

5. Unrecorded Bank Fees and Charges

Small amounts add up. Banks incur various fees, from correspondent banks (Nostro account charges), card networks, and clearing systems. These debits often hit external statements directly but aren't always automatically captured and posted internally in the bank's general ledger.

Example: A monthly maintenance fee or per-transaction charge appears on the Nostro statement. Reconciliation teams must often manually identify this charge and create the corresponding internal accounting entry. This is due to a lack of automated feeds or processes for these specific charge types.

6. Missing or Duplicated Transactions

A transaction might be recorded in one system (e.g., the switch) but completely missed in another (e.g., failed file load into the CBS), or, conversely, accidentally posted twice due to a system glitch.

Example: A network settlement file fails to load properly. All its transactions become exceptions when compared to CBS records. Or, a technical hiccup causes a payment instruction to double-post internally, creating a duplicate that reconciliation must flag for reversal.

These point to system interface issues, transmission failures, or processing bugs.

7. Complex Reconciliation Scenarios: Nostro/Vostro, Inter-branch

Certain reconciliations are inherently more complex.

Matching Nostro (our accounts with other banks) and Vostro (other banks' accounts with us) involves navigating multiple currencies, tricky value-dating rules, and intricate SWIFT message matching.

Even inter-branch reconciliation within the same bank can be difficult if branches use partially independent systems.

Example: Successfully matching a SWIFT MT103 payment instruction against the corresponding MT910 debit confirmation from the nostro bank requires aligning value dates, amounts, currency, and charges. This calls for specific logic to address potential FX differences or investigation fees embedded in the messages.

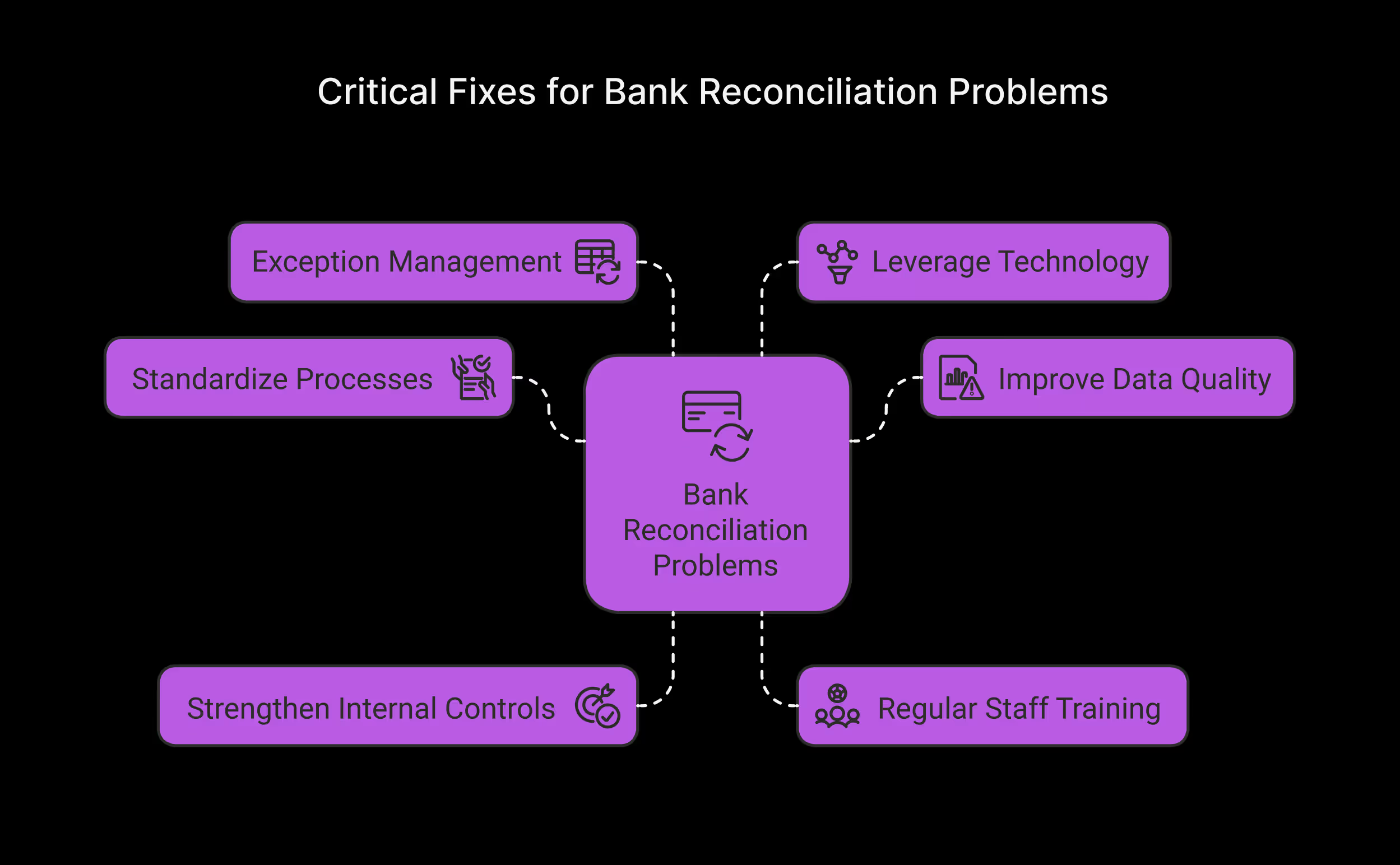

6 Critical Fixes for Bank Reconciliation Problems and Solutions

Addressing bank reconciliation problems requires a multi-pronged approach, from foundational process improvements to technological solutions. Here are the key steps (bank reconciliation problems with solutions):

1. Standardize Reconciliation Processes

Define and document clear, consistent procedures for all types of reconciliations. Specify data sources, matching criteria, timelines (daily reconciliation is crucial for high-volume areas), escalation procedures for exceptions, and roles and responsibilities. Consistency is key.

2. Improve Data Quality at the Source

The best way to reduce reconciliation breaks is to prevent errors upstream. This involves:

- Implementing validation rules in transaction processing systems.

- Enhancing data governance policies.

- Working towards standardizing data formats and identifiers across systems where possible.

3. Strengthen Internal Controls

Implement checks and balances, such as segregation of duties (ensuring the person processing transactions isn't the same person reconciling them), regular independent reviews of reconciliations, and mandatory approvals for adjusting entries.

4. Regular Staff Training

Ensure the reconciliation team understands the processes, common error types, the systems involved (CBS, switch, network protocols), and the importance of their work. Train them on investigation techniques and the use of any reconciliation tools.

5. Implement a Robust Exception Management Framework

Don't just identify exceptions; manage them. Define categories for different types of breaks (timing, fee, error, potential fraud), assign ownership, set resolution deadlines, and track aging.

This prevents exceptions from languishing unresolved. Use bank reconciliation statement problems analysis to identify recurring issues.

6. Leverage Technology Automation

For banks, manual reconciliation is simply not scalable or sustainable. Automation is the most effective way to tackle the volume, complexity, and data fragmentation issues head-on.

How Automation Reduces Bank Reconciliation Problems?

.avif)

Automation platforms specifically designed for bank reconciliation can dramatically transform the process:

- Automated Data Aggregation: Reconciliation softwares can automatically connect to and extract data from various sources CBS, switch logs, SWIFT messages, network files, external bank statements (via APIs or file uploads) eliminating manual data gathering and consolidation errors.

- Intelligent Matching Engines: These tools use predefined rules (configurable internally) alongside advanced Artificial Intelligence (AI)/Machine Learning (ML) algorithms. They help match vast numbers of transactions across different datasets, even with variations in formats (one-to-one, one-to-many, and many-to-many matching scenarios) or reference data.

- Automated Exception Identification and Workflow: The system automatically flags unmatched items (exceptions). More importantly, it can categorize them based on rules (e.g., identifying likely timing differences vs. potential errors) and route them electronically to the appropriate team or individual for investigation via built-in workflows. This ensures accountability and speeds up resolution.

- Enhanced Visibility and Reporting: Real-time dashboards show the status of reconciliations, the number and aging of exceptions, and key performance indicators (KPIs). This transparency allows management to monitor performance, identify bottlenecks, and spot systemic issues.

- Reduced Manual Errors: Automating data handling and matching virtually eliminates the risk of human error associated with manual input or comparison.

- Improved Speed and Efficiency: Automation speeds up reconciliations from days to just hours or even minutes. Banks can reconcile daily rather than pausing for weekly/monthly cycles, which significantly reduces risk exposure. Staff can focus on complex exceptions rather than tedious matching.

How Osfin Helps Eliminate Your Reconciliation Woes

Osfin understands the intricate reconciliation challenges faced by banks. Our platform is designed to directly address the pain points discussed scattered data, manual effort, complex matching, and slow exception resolution. We provide:

- Seamless Data Integration: Connectors to aggregate data automatically from your core banking system, payment switches, network files, and external sources.

- Advanced Matching Capabilities: Powerful, configurable rules engine combined with AI to achieve high auto-match rates across diverse datasets.

- Streamlined Exception Management: Integrated workflow tools to categorize, assign, track, and resolve exceptions efficiently.

- Real-time Visibility: Comprehensive dashboards and reporting for complete control and insight into your reconciliation landscape.

{{banner1}}

FAQs on Bank Reconciliation Problems

1. What is the single biggest bank reconciliation problem?

The biggest systemic challenge for banks is fragmented data across CBS, switch, and network files, combined with huge volumes. It makes matching and investigation incredibly complex and slow.

2. Is daily reconciliation necessary for all bank accounts?

Daily reconciliation is crucial for high-risk, high-volume accounts like nostros and suspense, and for system checks (Switch-to-CBS). Less active ones depend on risk assessment.

3. Can automation completely eliminate reconciliation exceptions?

Automation maximizes auto-matching, minimizing exceptions, but won't eliminate valid breaks like timing differences or real errors. It focuses teams on necessary investigations.

4. How is AI used in bank reconciliation automation?

AI and ML enhance matching by learning data patterns, suggesting non-exact matches, and predicting break resolutions. It helps flag anomalies that could indicate fraud or new error types.

5. What is the typical ROI for implementing reconciliation automation?

ROI stems from multiple domains. These include slashing manual effort (FTE savings), quicker error/fraud detection (loss reduction), better compliance, faster close, and redirecting staff to higher-value analysis.