Core Banking System Explained: Benefits & Trends

When you ask the customers of today what they expect from banks, the answer is simple: a greater degree of control and self-service.

The pandemic, undoubtedly, played a part in this shift, setting in motion an industry-wide domino effect.

Banks are responding by refitting their core banking foundations to deliver quicker, cleaner, and more intuitive experiences that build satisfaction and loyalty.

On the technology side, big tech firms are developing automation and advanced data processing for core banking systems. Fintechs, on the other hand, are asking the hard questions: what is a core banking system, and more importantly, what can it be?

If you are evaluating a move, this guide walks you through core banking, meaning, and how it works, while also outlining the advantages and drawbacks so you can make a clear and confident decision. Read on.

What this blog covers:

- What core banking is and how it drives banking operations

- How modern core banking systems differ from legacy platforms

- Core modules and processes every core banking system should support

- Key features like APIs, integration hubs, security, and scalability

- Benefits of adopting a modern core banking solution

- Challenges and risks when migrating or modernizing cores

- How Osfin integrates with and augments core banking systems

- Real-world use cases and trends shaping the future of core banking

- Frequently asked questions and practical insights

Core Banking Definition and Meaning

Core banking is the centralized back-end platform that processes daily banking transactions, maintains customer and account records, and updates the bank’s general ledger across all channels and branches. Its umbrella of functions encompasses deposits, withdrawals, payments, account servicing, and lending.

The CORE in banking stands for Centralized Online Real-time Environment, which means that the customer can experience the bank as a single entity.

How Does a Core Banking System Work?

At its core, a core banking system is a network of back-end servers that run everyday banking functions, from posting debits and credits and calculating interest to updating statements and processing withdrawals.

When a customer uses an ATM or makes a withdrawal at a branch, the front-end app fires a request to a centralized data center.

The platform then authenticates the user, checks limits and balances, executes the transaction, and writes results to the ledger so every channel sees the same truth.

That data center is a stack: database services, application servers for business rules, a web layer for secure APIs, and a perimeter of firewalls to keep out malware and misuse.

Modern core banking systems are built on an API and a microservices framework that allow for seamless integration of external applications and services.

- The system’s central database ensures that all account information, customer data, and transaction records are managed and stored in real-time, providing up-to-date data across all banking channels.

- Each functional module, such as cards, payments, or customer onboarding, interacts with the database through standardized APIs, making sure data flow is consistent.

- Using an integration hub further facilitates communication between external service providers and core systems, enabling features such as currency exchange, fraud detection, payments, and regulatory compliance.

- This architecture supports flexibility and scalability, enhancing performance and security for reliable and efficient banking operations.

Modern Core Banking Vs Legacy Systems: A Comparison

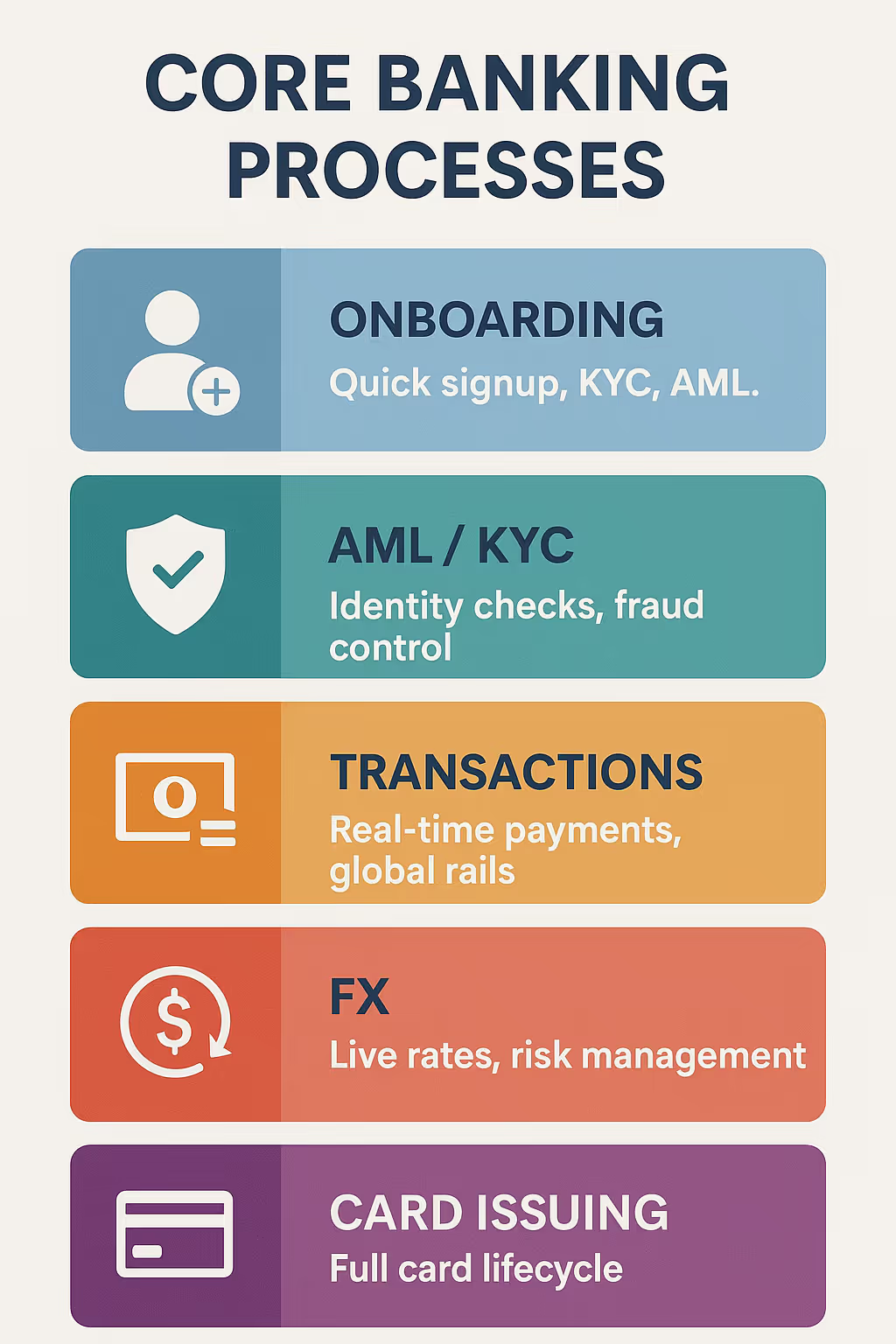

What are the Key Core Banking Processes?

Here are some of the essential processes that are associated with core banking, and which every core banking platform must have:

1. Customer Onboarding:

This module guides a prospect from their initial contact to a live account. As you can guess, the system collects the basics, verifies documents, and runs the checks banks need for KYC and AML. Most of it is automated, so fewer forms, fewer mistakes, and a much faster start. Ultimately, having a frictionless onboarding module ensures customers have a smooth start, which sets the tone for a longer, happier relationship.

2. AML/KYC:

To ensure that the banks can thoroughly verify the identity of their customers, KYC was introduced. At the outset, these rules help banks authorise users, monitor activity, and assess risk to deter fraud or money laundering efforts.

More modern systems not only ensure foolproof due diligence, but also make the process itself more convenient for the clients. For instance, while traditional banks might need a customer to bring physical identification documents, a modern core banking software would only require online submission of paperwork.

3. Transaction processing:

Real-time transaction processing is a hallmark feature of modern core banking. It ensures that all financial activity conducted within the system, like transfers and deposits, is processed and updated instantly.

In addition, it’s also responsible for how wide the payment acceptance is for banks. It determines if it supports all types of mobile and card payments, or if it allows for seamless cross-border payments made under SEPA, SWIFT, CHAPS, ACH, and BACS.

Banks can answer these questions in the affirmative by connecting to payment-as-a-service or embedded finance providers. This type of fast payment system not only builds customer satisfaction but also facilitates the accurate management of banking records.

4. Currency exchange:

Today's customers expect fast, hassle-free cross-border payments and fair exchange rates. A well-built currency exchange module makes that possible. It allows the core to be plugged into FX/liquidity providers to stream real-time prices, request competitive quotes, apply tiered spreads, and lock rates for a short window.

Ultimately, integrations like these enhance the financial institution’s ability to manage currency risk, offer better pricing, and improve overall service quality.

5. Card issuing:

From card issuance and activation to expiration and renewal, the card issuing module manages the entire lifecycle of a card. To offer these services, a bank must hold Principal Membership with schemes such as Visa or Mastercard.

Alternatively, they can also act as an agent for an IBAN sponsor or official card issuer. In this arrangement, the core banking platform directly integrates with the issuer to ensure a convenient card lifecycle for the customer.

Features of Core Banking Software

Modern core banking features focus on internal capabilities that deliver efficiency and stability, enabling complex banking processes to run reliably, securely, and at scale.

Here are the key features:

1. Centralised database:

A single source of truth for all customer data, accounts, balances, transactions, identity documents, tariff groups, and more. Given that it’s a core component of the system, it’s protected inside and out with encryption, access controls, audit logs, and retention policies to meet legal and security requirements.

2. API and integration hub:

To connect the external modules, banks need a middleware that connects products, partners, and channels through API-first support. Modern core banking platforms today ship with ready integrations to multiple payment schemes, payment types, FX/liquidity providers, AML/KYC, and fraud detection services.

It ensures you make the most of all the modules you add to your core banking. At the end of the day, this means providing secure partner onboarding, versioning, monitoring, and retries to keep services reliable at scale.

3. Security and compliance systems and services:

Protecting sensitive customer data and adhering to regulatory standards are non-negotiable mandates for banks today.

Therefore, banks must employ robust cybersecurity measures, including cutting-edge methods like continuous monitoring and advanced encryption protocols, to make sure that not only are all boxes checked, but they are so in the most reliable manner.

This includes adherence to GDPR, AML/KYC requirements, and other industry-specific standards. Fortunately, modern core banking systems have automated compliance tools for real-time monitoring, reporting, and auditing. At the end of the day, these modules help you set up real-time alerts, reporting, and audit trails to reduce risk and simplify regulatory reviews.

4. White-label platforms:

Today, web and app are the primary customer touchpoints when it comes to banking. Of course, having your own branding over your systems works. With white-label web and mobile apps, banks can ship fast with their own branding, without having to waste effort and time developing their own software from scratch.

Out of the box, they include account views, payments and transfers, card controls, and in-app support. Institutions can also tailor their services to match the experience to the right audience. How? With the built-in integration hub that allows you to connect your core banking systems to third-party banking APIs, which improve usability and speed-to-market.

5. Core banking engine:

It’s the necessary real-time engine for accounts and payments, built on open APIs. This engine allows modules to be added and configured as per need, which includes onboarding, payments, account management, card issuing, and the whole nine yards.

Moreover, these modules can be used independently or as a part of a unified platform with multicurrency support and instant ledger updation.

Benefits of Core Banking Solution

Now that you know about the principles and capabilities of modern core banking platforms, here’s a list of all the benefits they unlock:

1. Higher productivity

With all your data available in a centralized format, you can cut the back-and-forth between branches, making transactions move faster regardless of the customer's location.

This straight-through processing and shared data reduce the need for manual handoffs and duplicate entry. The result? Now, the front, middle, and back office teams get to work off the same source of truth, which shortens turnaround times and improves customer experience.

2. Stronger security

The more secure your systems are, the more trust you garner, and the less the possibility of any mishap. To that end, modern core banking platforms add layers of encryption across the stack so that there are no leaks. Additionally, role-based access controls, audit trails, and AI-based anomaly detection help prevent internal and external threats.

Protection on the client-side is equally important, if not more so. Adding a zero-trust layer along with biometric and MFA reduces the chances of any compromises from the customer's end.

Together, these safeguards support broader regulatory compliance without slowing down the user.

3. Anytime, anywhere banking

In a world that’s growing increasingly digital, availability matters. A resilient core keeps services online around the clock, with mobile, web, ATM, and API channels drawing from the same reliable engine. Cloud-ready architectures, active-active failover, and disciplined SRE practices help banks meet uptime targets while giving customers support whenever they need it.

4. Lower operating costs

Automation, powered by the AI-driven components of modern core banking systems, allows banks to reduce manual work. This, in turn, shrinks the room for error and offers capabilities that allow teams to do more with less.

Moreover, consolidating legacy systems onto a single platform cuts maintenance overhead and vendor sprawl. You also get to standardize processes across the board, which reduces training time and exception handling, freeing budgets for meaningful processes like innovation and product development, rather than upkeep.

5. Multi-currency readiness:

Customers can now carry out cross-border payments effortlessly, without having to bow down to large manual conversions. Modern core banking systems can integrate with real-time FX rate modules and multicurrency wallets to improve the affordability and accessibility of cross-border settlements.

Banks can also collaborate with local clearinghouses and apply rules-based hedging to limit exposure.

The Role of Core Banking in the Digital Era

Core banking has transitioned from nightly batch runs to an always-on model. Customers now expect instant transactions, always-updated statements and records, and a consistent experience across channels.

That’s a high bar to meet, and one that necessitates that core banking systems turn into real-time engines that update transactions, integrate with secure APIs, and enforce risk and compliance without adding any friction.

On top of that, new payment methods, evolving data-sharing rules, and new, richer digital formats have raised those expectations further. As a result, core banking systems now must also carry data end to end, while managing fraud and liquidity around the clock.

This interoperable and granular nature of operations is being addressed by cloud-based and modular designs. Since most institutions modernize in phases (augment-first, replace selectively), this model of core banking systems suits the needs of banks perfectly.

Ultimately, the payoff is speed and clarity. A modern core banking platform significantly shortens product cycles and unlocks cleaner, better use of data.

In fact, today it has become the bank’s connective tissue, allowing teams to plug in partners quickly, orchestrate journeys from front to back, and ship steady improvements within regulatory guardrails.

How Osfin Integrates with Core Banking Systems

Most banks don’t do an all-at-once "big bang" migration. They layer specialist services alongside their legacy systems and modernize in phases. Reconciliation is one of the specialist services.

Regulators and researchers outline three practical paths: full replacement, component replacement, or wrapping/augmenting the legacy core; the last two are the lower-risk routes many institutions choose.

Osfin built for that reality. We plug into your core and adjacent systems, unify transaction data, automate matching, and publish audit-ready outputs, without forcing a complete migration.

As a financial operations automation platform, we are focused on high-speed reconciliation for banks and fintechs. Our file-format agnostic platform ingests data from diverse sources, including internal databases, payment gateways, and banks, and reconciles deposits, loans, payments, invoices, and other financial transactions.

Our integration model is connector-led. Osfin provides seamless API integrations and 170+ pre-built connections, which banking teams can use to pull transaction, settlement, and statement data into a single source of truth.

Our pipelines are format-agnostic. It can handle Excel, CSV, JSON, XML, MT940, and more with ease, no manual formatting required. This matters when your core, gateways, and clearing files all speak different file extension dialects.

Using this data, we normalize records and run high-speed matching with exception tagging, dashboards, and a no-code rule builder. In performance benchmarks, our platform processed up to 30 million records in ~15 minutes, covering ACH, SWIFT, RTP, and card network files.

Here’s how it fits your core:

- Connect: Link the core, ERPs, processors, gateways, and bank feeds via connectors/APIs.

- Normalize: Map incoming formats (e.g., MT940/CSV/JSON) to a unified dataset.

- Reconcile: Apply matching rules, auto-tag exceptions, and route to owners in real time.

- Publish: Push reconciled outputs and reports to finance systems and stakeholders.

On the compliance front, we’re fully aligned with SOC 2, ISO 27001, PCI DSS, and GDPR. We employ 256-bit SSL/TLS encryption, role-based access controls, and two-factor authentication (2FA) to ensure enterprise-grade security.

If you’re augmenting your core, we provide a fast and controlled way to centralize data, reconcile across rails and systems, and implement finance operations improvements now, while your longer core modernization journey continues.

Why not try it out for yourselves? Get in touch with us at Osfin and discover how you can elevate your reconciliation.

Frequently Asked Questions

1. How is core banking different from online or mobile banking?

Online and mobile banking are customer channels. Core banking is the processing and record-keeping engine that channels call to post transactions.

2. What is a banking core?

Core banking is the central back-end system that links all branches of a bank, allowing customers to access accounts and make transactions through a single, secure platform. It covers functions like loan management, new account opening, deposits, withdrawals, and more.

3. What is the difference between retail banking and core banking?

Core banking refers to the infrastructure and systems that underpin banking operations, while retail banking encompasses consumer-facing services such as savings accounts, loans, and mortgages.

4. What are the disadvantages of core banking?

Core banking relies excessively on technology. This means that any failure in computer systems can cause the entire bank network to break down. Also, if data is not properly protected, hackers can access sensitive customer data.