Interchange Fees Explained: Rates, Costs & Savings

In 2021, U.S. businesses spent around $137.8 billion on card processing fees, with interchange fees making up a substantial 70% to 90% of that total. Interchange fees are complex and often non-transparent.

Over time, these hidden expenses can falsify financial forecasts, complicate pricing strategies, and restrict operational flexibility in a competitive market. Without clear visibility and control, organizations also risk escalating costs.

The first step toward addressing the problem is understanding interchange fees' meaning, how they work, why they exist, and what can be done about them.

In this article, we’ll define interchange fees, explain how they work, and share the strategies to reduce their operational and financial impact.

What this blog covers:

- What interchange fees are and why they exist

- How interchange fees are calculated

- Key factors that influence interchange rates

- Different pricing models (flat rate, interchange-plus, etc.) and how they compare

- The financial impact of interchange fees on merchants’ margins and pricing strategy

- Strategies to optimize or reduce interchange costs

- How Osfin’s tools help detect overcharges and streamline settlement to lower interchange burdens

- Frequently asked questions and misconceptions about interchange fees

What is an Interchange Fee?

An interchange fee is a transaction charge set by card networks (like Visa or Mastercard) that the acquiring bank pays to the cardholder’s issuing bank for every credit or debit card transaction. This cost is ultimately passed on to merchants through their card processing fees.

Card interchange fees make up the largest share of card processing fees, as they compensate issuing banks for fraud risk, payment infrastructure, and rewards programs. Rates vary depending on factors such as card type, transaction channel, merchant category, and transaction volume.

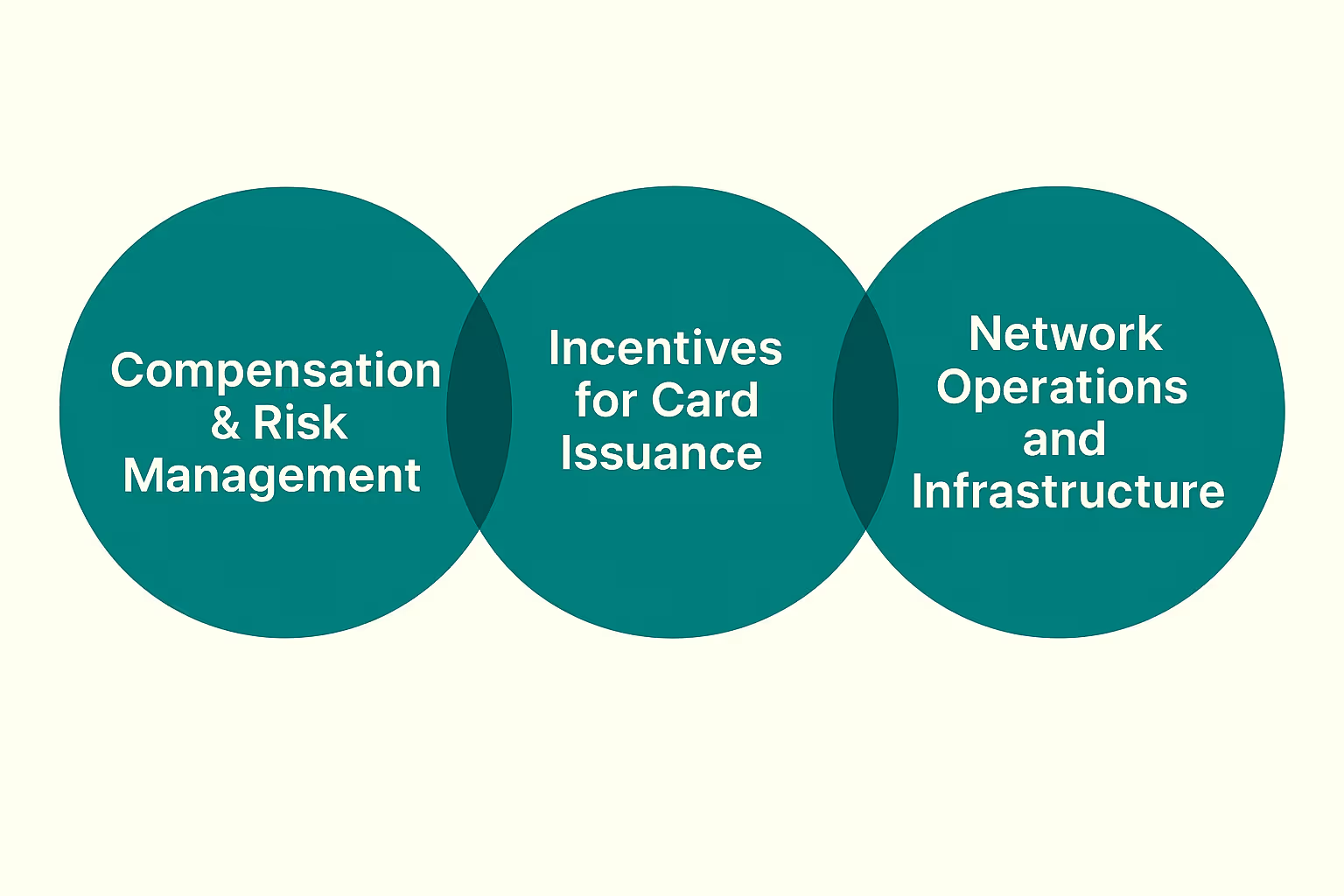

Why do Interchange Fees Exist?

The interchange fees exist for a variety of reasons, some of which are:

1. Compensation & Risk Management

Interchange fees reward issuing banks for providing cards, managing accounts, and limiting fraud and credit risks. These costs include account maintenance and payment security, enabling issuing banks to deliver cardholder services while mitigating risk.

2. Incentives for Card Issuance

Higher merchant interchange fees encourage banks to issue and promote payment cards in the market, increasing total card adoption and overall transaction volumes. This would benefit banks, card networks, and merchants by solving customer payment pain points while enabling the growth of electronic payment infrastructure across various industries.

3. Network Operations & Infrastructure

Bank interchange fees fund internal card network operations like fraud prevention, dispute resolution, and technology infrastructure. These revenues help provide stable and fast payment systems with a great user experience to merchants.

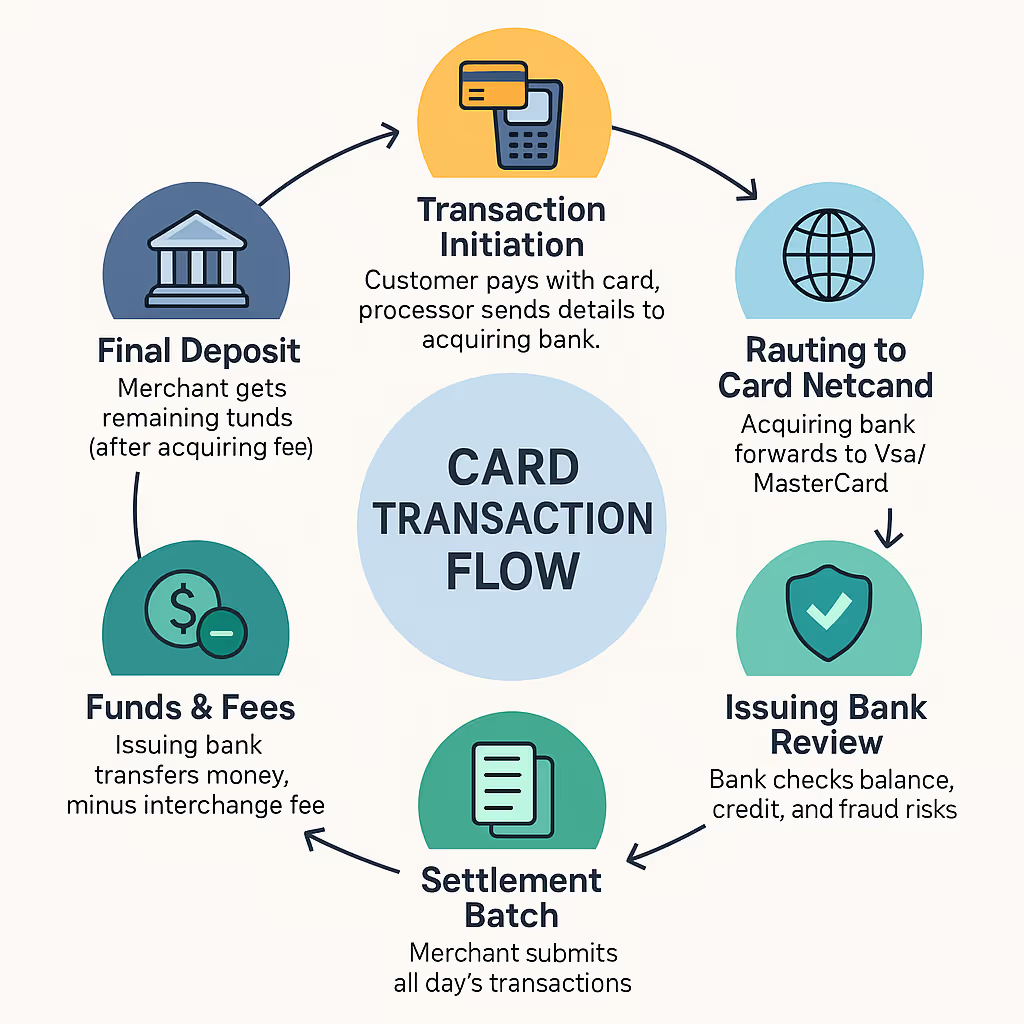

How Do Interchange Fees Work?

An interchange fee is charged with every credit or debit card transaction. Understanding the step-by-step flow shows how funds, fees, and authorizations move across banks, networks, and processors. Let’s take a look at the process.

Step 1: Transaction Initiation

This is when a cardholder buys something with a credit or debit card. Upon completion of shopping, the merchant’s payment gateway or processor sends transaction details to the acquiring bank, initiating the process.

Step 2: Routing to Card Network

The acquiring bank forwards the request for the transaction through the relevant card network (Visa, Mastercard), which in turn redirects it to the issuing bank of the cardholder for validation.

Step 3: Issuing Bank Review

The issuing bank validates the cardholder's available balance or credit limit and conducts fraud detection checks before accepting or rejecting the transaction.

Step 4: Authorization Transmission

The issuing bank sends authorization back through the card network to the acquiring bank, which communicates with the merchant and usually does so within seconds.

Step 5: Settlement Batch Submission

Upon the close of business day, the merchant delivers authorized transactions in a batch to their acquiring bank for settlement through one of the card networks.

Step 6: Fund Transfer and Fee Deduction

The card network sends the transaction to the issuing bank, debits the bank’s account, and then transfers the funds, after deducting the interchange fee, to the acquiring bank.

Step 7: Final Merchant Deposit

The acquiring bank deposits the remaining amount in the merchant's account minus their acquiring fee, thus completing the payment cycle.

{{banner3.1}}

Interchange Fee Rates & Factors

The rate of interchange fees depends on the geographical location, card types, and transaction method.

That fee is typically about 2% of the transaction value in the US. Debit card fees, capped by the Durbin Amendment at $0.21+ 0.05% per transaction, cost merchants less than credit cards.

Across the European Union, card interchange fees are limited to 0.3% of the value of a credit card transaction and at most 0.2% for direct debit card transactions. Every April and October, Visa and Mastercard review and modify their rates in response to current trends.

However, there are several factors affecting the interchange fee rates, some of which are:

- Card Type: Debit cards with PINs are cheaper; rewards credit cards charge more to pay for benefits.

- Business Size and Industry: Bigger businesses can often negotiate more competitive rates, and value-based pricing is standard in some industries, e.g., higher fees for supermarkets than fuel retailers.

- Transaction Type: Card-present transactions (POS) cost less than card-not-present transactions (CNP), such as MOTO orders, or phone sales.

- Card Brand Policies: Every card network, including Visa, Mastercard, American Express, and Discover, has its own operating regulations. At the same time, Amex and Discover operate differently.

- Regulatory Caps: The Durbin Amendments in the U.S. or EU Interchange Caps influence maximum allowable rates.

How to Calculate Interchange Fees?

Interchange fees involve many economic variables that the card networks determine themselves. Although rates look flat rate + percentage, several factors affect the actual cost to process a single transaction.

Key factors in calculating interchange fees are:

1. Card Type

The interchange credit card fees are higher than those of debit cards. Even the rewards, the premiums, and the business card are costly, with fees funding the perks and loyalty programs made available by issuing banks.

2. Transaction Method

Card-present transactions (swipe, chip, or tap) can be processed quickly through the checkout and have lower rates due to less risk of fraud. Card-not-present transactions like phone & MOTO have higher costs due to more security risks.

3. Merchant Category Code (MCC)

The merchant's MCC reflects the industry's risk and average ticket size. When an industry has higher average transactions, it will have a higher interchange rate, since the risk involved is higher than others.

Impact of Interchange Fees on Stakeholders

Effective interchange rates can make the difference in influencing profitability with transaction costs and provide insights into how to offer competitive pricing.

These costs, which build up very quickly for businesses with high-volume card transactions, are foundational to virtually every aspect of a company, from customer pricing to payment acceptance policies.

Here are some aspects in which interchange fees can impact business:

1. Operating Costs

Each time a card is used for a transaction, it incurs an interchange fee, reducing margins (especially in high-volume, low-margin businesses). That makes managing costs and adding fee reduction strategies crucial.

2. Pricing Decisions

A business can increase prices, set minimum card payment amounts, or take the loss, leading to various implications for competition and meeting customer expectations.

3. Cash Flow

Due to fees being taken off before deposits hit business accounts, businesses need to forecast cash flow accurately and adjust working capital.

4. Business Model Adjustments

Many businesses can minimize fee exposure by encouraging cash or debit card use, implementing surcharges (where legal), and working with processors more wisely.

{{banner1.1}}

Interchange Fees Vs Other Payment Fees

Interchange fees are a small portion of the total cost of accepting card payments; other payment processing costs include several others. Understanding both is essential for effective cost management.

- Interchange Fees: Acquiring bank (the merchant's bank) pays the issuing bank (the cardholder's bank) for each transaction. Networks like Visa or Mastercard set this fee.

- Other Payment Fees: Services such as security and transaction routing come at a cost that payment processors/gateways charge.

Interchange charges are set by networks; other fees will often depend on services and volume.

Examples: Credit card charges interchange fees at 2.00%, debit cards at 0.30% (Kotak Mahindra Bank); gateway fees, chargebacks, and assessment fees may vary.

Trends Shaping Interchange Fees In 2025

In 2025, regulatory trends, a faster pace of technology adoption, and shifting consumer payment preferences are working to shape interchange fees. This presents finance and operations leaders with new cost-saving opportunities and operational challenges.

Regulatory Pressure: Restrictions are increasing with governments fine-tuning mandates like the Fed’s debit cap adjustment, pushing processors and merchants to adopt new payment vectors and work on cost savings.

Real Time and Digital Wallets: Instant, mobile, cashless payments drive cost savings and security, disrupting payments technology based on the traditional card type and fee structure.

BNPL Expansion: Buy Now, Pay Later reconfigures transaction economics, introducing alternative fee structures and potential regulatory pitfalls.

Fraud Prevention & Tokenization: Enhanced security measures, such as fingerprint authentication & tokenization, allow a high chance of reducing interchange categories and their fees.

How Osfin Automates Interchange Fees Optimization

Interchange fees remain a significant, often hidden, cost driver for businesses. The complexity makes it difficult for finance teams to know if they’re overpaying or being charged incorrectly. This is where reconciliation becomes critical. Without it, you can’t:

- Verify accuracy of fees charged by acquiring banks and card networks.

- Spot discrepancies where they may be overcharged or misclassified into higher-fee categories.

- Gain transparency into true payment processing costs across multiple channels.

- Optimize expenses by identifying patterns and switching to lower-cost payment routes.

Osfin automates this reconciliation process.

Osfin is a high-speed, intelligent reconciliation platform for enterprises dealing with high-volume transactions. It keeps analyzing the transactions, automatically flags overcharges, performs automatic exception handling, and effortlessly fits in with normal payment processes through its intuitive real-time dashboard.

Here’s how it achieves this:

- Data Ingestion: Ingests data from multiple sources through its file-format agnostic platform. No matter the file type or size, Osfin can easily integrate it using its 170+ pre-built connectors and normalize the data. It can also apply custom deviation tolerances during ingestion to filter out any poor-quality data before reconciliation begins.

- Logic-Driven Reconciliation: Reconciles 30 million records in just 15 minutes and has the ability to handle many-to-one or one-to-many transactions.

- Automated Exception Handling: Scans payment records to identify incorrect or inflated interchange rates. If there are any discrepancies, they instantly get routed to the appropriate team member for correction.

- Compliance Reporting: Generates detailed reports and keeps workflows audit-ready with full traceability and transaction history. Real-time dashboards also provide savings insights, fee category breakdowns, and optimization opportunities.

- Data Protection: Secures sensitive data with 256-bit encryption, role-based access, and two-factor authentication.

- Global Standards: Meets leading regulatory requirements, including SOC 2, PCI DSS, ISO 27001, and GDPR.

{{banner3}}

FAQs on Interchange Fees

1. What is interchange in credit card processing?

Interchange fees, explained in simple terms, would be the charges paid by the merchant’s bank to the cardholder’s bank for processing a transaction, and are decided by card networks like Visa or Mastercard.

2. Who sets interchange fees for credit cards?

Credit card interchange fees are set by card networks such as Visa, Mastercard, or RuPay, depending on the type of cards, payment method, merchant category, and transaction amount.

3. Can interchange fees be negotiated?

Not usually, because card networks typically set interchange fees. However, most of the costs associated with payment processing can be negotiated with providers.

4. How do interchange fees impact merchants?

For many merchants, interchange fees are an essential component of total payment processing costs since they ultimately impact merchant profitability and pricing of goods and services.