Payment Reconciliation Risks and How Automation Helps

Payment reconciliation is the backbone of financial operations in any business.

Yet it’s one of the trickiest processes to truly understand. The steps look simple on paper, but the moment you get into real payments from different sources, different timings, different formats it stops feeling simple. The details blur. The numbers don’t always line up. And it’s hard to know what’s supposed to happen next.

That’s why you need this guide. This article explains payment reconciliation. What it is. How it works. How to make it faster.

So let’s get started:

What this blog covers:

- What payment reconciliation is and why it matters for financial accuracy

- How to match payments with records like invoices, bank statements, and internal ledgers

- Common challenges in manual payment reconciliation (timing mismatches, data silos, errors)

- Best practices to streamline and automate payment reconciliation and control exceptions

- How Osfin’s platform supports automated payment reconciliation software for faster, more accurate outcomes

- Frequently Asked Questions on Payment Reconciliation

What is payment reconciliation?

Payment reconciliation is comparing internal payment records with the external sources, bank statements, and gateway reports to ensure they match and confirm that each transaction is accurate. This helps companies spot any discrepancies and fix issues to keep all the accounts, books, and reports consistent and reliable across the business.

Why payment reconciliation matters for businesses

Every business runs on the simple idea that money in and money out should match. Payment reconciliation is how you confirm that the story is true. It keeps your financial data grounded in reality, so every decision, report, and forecast is built on numbers you can trust.

Here’s a deeper look into it:

1. Your books become accurate

Reconciliation keeps your records clean and accurate. It’s the checkpoint that makes sure your ledgers reflect what actually settled in your bank or payment systems. When this step works, your statements line up, your close runs smoother, and your financial data stops drifting over time.

2. Cash flow becomes clear

Businesses move fast. Reconciliation is what keeps the pace. It shows what payments have come in, what’s still in transit, and what needs to be reviewed. That kind of clarity keeps every decision sharp and on time.

3. Controls get enforced better

Reconciliation creates natural controls. It catches discrepancies early, gives auditors a clear trail to follow, and shows regulators your house is in order.

4. Forges stronger vendor relationships

When payments are recorded correctly, refunds align, invoices match, and payables stay on schedule. That accuracy builds trust and reduces disputes, delays, and surprises.

5. Helps you forecast with clarity

You can’t forecast from fuzzy input. Reconciliation gives finance teams dependable numbers to model revenue, burn, runway, and working capital. The cleaner the reconciliation, the sharper the insights.

{{banner3.1}}

Types of Payment Reconciliation

The way you handle payment reconciliation depends on how your business receives money. The tools you use, the channels customers pay through, and the volume of transactions all influence the process. A retail business that sells in-store will reconcile payments differently from an ecommerce brand using multiple online gateways.

Let's look at some common types of reconciliation that businesses manage regularly.

1. Bank Reconciliation

This is the most widely used type. You compare your internal financial records with your bank statements to check that every debit or credit reflects the actual transaction.

If your books say you received $12,000, but the bank statement shows $11,500, there's a gap to investigate. Maybe it's a bank fee, a delayed transfer, or an error in data entry.

2. Payment Gateway Reconciliation

If you accept online payments through platforms like PayPal, Square, or other third-party gateways, you need to confirm that the money processed through these gateways matches your sales data. Payment gateway reconciliation helps you track deductions like transaction fees, refunds, and chargebacks.

For example, if you sold products worth $6,000 last month through your gateway but only $5,750 hit your account, reconciliation helps you identify where the $250 went.

3. E-commerce Payment Reconciliation

When you sell through marketplaces like Amazon or eBay, you deal with multiple payout cycles, deductions, promotions, and returns. Ecommerce payment reconciliation involves matching your internal sales reports with what the platform pays out.

Suppose you made 500 sales on Amazon in a week, reconciliation helps you confirm the number of shipped, returned, and paid orders line up with what Amazon credited to your account.

4. Vendor Payment Reconciliation

This applies when you're paying your suppliers or service providers. You check that the amount you agreed upon matches the invoice and the actual payment made. It also helps confirm there are no duplicate or missed payments. This is especially useful when you work with multiple vendors on recurring contracts.

5. POS Reconciliation

If you run a brick-and-mortar store and use a Point-of-Sale system, you need to reconcile the daily POS report with the cash and digital payments received. It's a quick way to identify billing errors or theft. For example, if your POS report says $2,000 in sales and you only received $1,850, it raises a red flag.

6. Subscription Billing Reconciliation

Businesses offering monthly or annual subscriptions reconcile recurring billing data against received payments. This ensures that all active users have paid and that inactive users haven't been charged.

Benefits of payment reconciliation

A strong reconciliation process gives your business steadier ground. Because it aligns the small details that shape the big picture. Here’s how it actually helps.

- Cleaner, simplified accounting: Reconciliation matches every transaction back to its source, keeping ledgers synced so your team isn’t rebuilding the story later.

- Cash-flow clarity: By confirming what really settled, reconciliation gives you a true view of your cash position instead of a rough estimate.

- Frictionless closes: When mismatches are resolved along the way, month-end isn’t a scramble, but it’s a final check on work that’s already clean.

- Fewer errors: Regular matching exposes duplicates, missing entries, and timing gaps early, keeping small issues from compounding.

Stronger audit trails. Each matched transaction creates a traceable path, making audits simpler because every number already has proof attached.

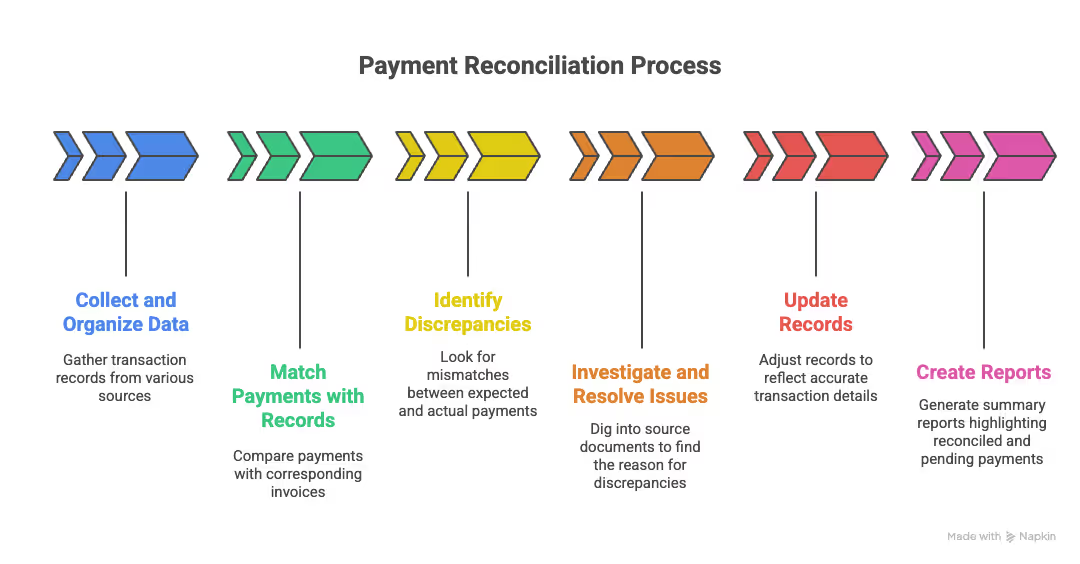

A Step-by-Step Look at Payment Reconciliation

The payment reconciliation process can vary depending on whether you're reconciling bank transfers, online payments, or vendor invoices. Still, most businesses follow a common workflow to track, verify, and update financial records.

Here's a step-by-step look at how it usually works.

1. Collect and organize payment data

Start by gathering all transaction records in one place. This could include invoices, sales reports, gateway settlements, and bank statements.

Let's say you use PayPal for website payments, Amazon for marketplace sales, and ACH transfers for settlements. Each platform shares reports differently. You'll need to download and sort them by date or order ID before starting.

2. Match payments with records

Once you've compiled the data, compare each payment with its corresponding invoice or order. You're checking for the right amount, correct date, and matching reference number.

For example, an invoice of $2,500 issued on April 5th should match a payment of $2,500 received in your bank account, also dated April 5th, with the same transaction ID.

3. Identify discrepancies

At this stage, you look for any mismatch between what you expected to receive and what actually came in. This includes missing payments, incorrect amounts, duplicate entries, or transactions marked as paid but not settled. Identifying these gaps early prevents reporting errors from piling up at the end of the month.

Let's say your internal records show a customer invoice of $3,000 as paid, but your bank shows two separate credits, $1,800 and $1,200, both referencing the same invoice number. This could indicate a split payment, a manual error, or a system glitch that needs deeper review.

4. Investigate and resolve issues

Once you spot a discrepancy, dig into the source documents or payment logs to find the reason. This may involve checking transaction IDs, verifying settlement reports from the gateway, or reaching out to the customer for clarification. The goal here is to determine if it's a legitimate partial payment, a gateway deduction, or a duplicate entry that needs adjusting.

In the example above, further investigation shows that the customer paid $1,800 through ACH but faced a failed attempt during the first transaction. They retried the payment for the remaining $1,200 using a credit card, causing the system to log both under the same invoice without flagging it as a split payment.

5. Update records

Once the issue is understood, adjust your records accordingly to reflect the accurate transaction details. This step helps maintain clean, audit-ready books and prevents the same invoice from being flagged again. Be sure to document the reason for the update, especially if it involves a correction or manual intervention.

In this case, you update the invoice status to "fully paid," mark it as a split payment with two reference IDs, and add a note explaining the failed ACH attempt and the second payment method.

6. Create reports

End the process by generating a summary report that highlights reconciled and pending payments. These reports support monthly closing, audits, and financial reviews.

How Does Payment Reconciliation Work?

The payment reconciliation process can vary depending on whether you're reconciling bank transfers, online payments, or vendor invoices. Still, most businesses follow a common workflow to track, verify, and update financial records.

Here's a step-by-step look at how it usually works.

1. Collect and organize payment data

Start by gathering all transaction records in one place. This could include invoices, sales reports, gateway settlements, and bank statements.

Let's say you use PayPal for website payments, Amazon for marketplace sales, and ACH transfers for settlements. Each platform shares reports differently. You'll need to download and sort them by date or order ID before starting.

2. Match payments with records

Once you've compiled the data, compare each payment with its corresponding invoice or order. You're checking for the right amount, correct date, and matching reference number.

For example, an invoice of $2,500 issued on April 5th should match a payment of $2,500 received in your bank account, also dated April 5th, with the same transaction ID.

3. Identify discrepancies

At this stage, you look for any mismatch between what you expected to receive and what actually came in. This includes missing payments, incorrect amounts, duplicate entries, or transactions marked as paid but not settled. Identifying these gaps early prevents reporting errors from piling up at the end of the month.

Let's say your internal records show a customer invoice of $3,000 as paid, but your bank shows two separate credits, $1,800 and $1,200, both referencing the same invoice number. This could indicate a split payment, a manual error, or a system glitch that needs deeper review.

4. Investigate and resolve issues

Once you spot a discrepancy, dig into the source documents or payment logs to find the reason. This may involve checking transaction IDs, verifying settlement reports from the gateway, or reaching out to the customer for clarification. The goal here is to determine if it's a legitimate partial payment, a gateway deduction, or a duplicate entry that needs adjusting.

In the example above, further investigation shows that the customer paid $1,800 through ACH but faced a failed attempt during the first transaction. They retried the payment for the remaining $1,200 using a credit card, causing the system to log both under the same invoice without flagging it as a split payment.

5. Update records

Once the issue is understood, adjust your records accordingly to reflect the accurate transaction details. This step helps maintain clean, audit-ready books and prevents the same invoice from being flagged again. Be sure to document the reason for the update, especially if it involves a correction or manual intervention.

In this case, you update the invoice status to "fully paid," mark it as a split payment with two reference IDs, and add a note explaining the failed ACH attempt and the second payment method.

6. Create reports

End the process by generating a summary report that highlights reconciled and pending payments. These reports support monthly closing, audits, and financial reviews.

{{banner3}}

Payment Reconciliation Examples and Case Studies

These real-world cases show how teams handle the complexity and what changes when the process becomes simpler, faster, and more accurate.

E-commerce retailer: Multi-gateway chaos to 99% automation

A leading e-commerce retailer was reconciling over a million monthly transactions across multiple payment gateways, banks, and internal systems. Fragmented data and manual matching slowed everything down.

After implementing Osfin.ai, the team achieved 99% automation, cutting manual work to near zero and giving eight people full control over massive transaction volume.

The result: reconciliation became an organized, predictable part of operations not a bottleneck.

A Tier-1 bank could cut card reconciliation time from days to hours

A major bank struggled with multi-day card reconciliation cycles driven by legacy systems and hundreds of daily exceptions. The delays pushed month-end timelines and added pressure on finance teams.

Osfin.ai reduced the entire process from days to hours and slashed manual exceptions.

The result? Month-end stopped taking over their evenings. The team got breathing room back. Less scrambling, more clarity.

Risks & Challenges of Payment Reconciliation

Even with a reliable process, payment reconciliation often brings along a set of challenges that can slow down operations or cause reporting issues. These problems usually show up as your transaction volumes grow, especially when you manage multiple payment channels or deal with tight reporting timelines.

1. Delayed or missing payments

Payments may not always arrive on time or might get lost between systems. This disrupts cash flow tracking and creates confusion in your financial reports. If you ship orders or pay vendors based on assumed receipts, even one missing payment can cause a larger downstream issue.

2. Manual data handling

Relying on spreadsheets or manual entry increases the risk of mistakes. A single typo, missed transaction, or misaligned reference number can lead to inaccurate books. Over time, this makes audits harder and forces your finance team to backtrack across weeks of data.

3. Disconnected payment sources

When you collect payments from different gateways, bank accounts, or platforms, it's hard to centralize data. Each provider sends statements in different formats and at different times. If you sell on your website, Amazon, and through direct bank transfers, reconciliation quickly becomes a time-consuming task.

4. High transaction volumes

As your business grows, so does the number of transactions. Matching each payment manually becomes unmanageable without increasing headcount. A flash sale or promotional campaign might bring in thousands of orders, all of which need to be tracked and verified.

5. Lack of transparency in deductions

Payment gateways often deduct fees, taxes, or holdbacks before settling the final amount. If these deductions aren't clearly broken down, you won't know whether you were underpaid or if the system is behaving as expected. This leads to guesswork and misreporting.

6. Duplicate or incorrect entries

Manually logging payments can sometimes result in duplicate entries or incorrect values being entered. These errors may not be caught until reconciliation, forcing your team to redo work or explain gaps during financial reviews.

7. Time-consuming audits

When reconciliation is irregular or poorly tracked, audits become difficult. Your team spends more time looking for missing data or justifying inconsistencies. This slows down monthly closures and puts pressure on your finance workflows.

How to Automate Payment Reconciliation

Manual reconciliation can only take you so far. As your payment volume grows, errors, delays, and data silos become harder to manage. That's where automated payment reconciliation steps in, giving you a faster, more scalable way to stay accurate.

What is automated payment reconciliation?

Automated payment reconciliation uses software to match transactions across your internal records, bank accounts, and payment gateways. It reduces human intervention and speeds up the entire process by pulling, organizing, and comparing data in real-time.

What parts of the process can be automated?

Most of the repetitive and error-prone steps can be automated, including:

- Importing bank statements and gateway reports

- Matching transactions with invoices or orders

- Identifying discrepancies or duplicate entries

- Applying rules to handle common deductions

- Flagging payments that need manual review

Automation handles high-volume data with consistency, making it easier to catch mismatches instantly.

Benefits of automation

Shifting to automation improves accuracy and saves time. It also helps your team focus on tasks that require actual judgment, like resolving payment disputes or managing exceptions.

Here's what you gain with automation:

- Reduced manual errors

- Faster month-end closures

- Centralized payment data

- Real-time visibility into discrepancies

- Better audit trails and compliance

Manual vs Automated Payment Reconciliation: What’s the Difference?

Manual reconciliation may work when your transaction volume is low or your payment sources are limited. As your business grows, though, the process becomes slower, more error-prone, and harder to manage. Automation helps solve these issues, but how exactly does it compare?

Here's a quick side-by-side view of manual vs automated payment reconciliation:

Also Read: Manual vs. Automated Bank Reconciliation: Differences?

How is automation done?

You can set up automated payment reconciliation through tools that connect to your accounting software, payment gateways, and bank accounts. These solutions pull data via APIs or file uploads and apply reconciliation logic automatically.

Platforms like Osfin.ai, for instance, offer custom workflows that fit different reconciliation types—be it gateway, ecommerce, or subscription billing. You get dashboards, alerts, and reports that help your finance team act faster, with fewer gaps to chase down manually.

Quicker, more efficient payment reconciliation with Osfin.ai

Manual payment reconciliation slows your finance team down and makes it harder to close your books on time. It also increases the risk of missed entries, duplicate records, and payment delays that can directly affect your cash flow. The longer it takes to match transactions, the harder it becomes to make timely financial decisions. Over time, these gaps limit your ability to scale confidently.

Automation is the smarter way forward, but financial operations demand more than just speed. You need a solution that's accurate, secure, and reliable, something built to handle sensitive financial data without compromise.

Osfin.ai is designed for this. This platform helps businesses automate payment reconciliation with built-in intelligence, seamless integration, and expert-driven support.

You can reconcile millions of transactions in minutes using Osfin.ai. This tool consolidates payment data from 170+ sources, including banks, issuers, and payment gateways. Businesses using Osfin.ai benefit from 99.9% auto-reconciliation powered by AI-based validation and data extraction. With real-time dashboards and customizable reporting, you get full visibility and faster issue resolution across every reconciliation cycle.

Security is built into every layer of Osfin.ai. This solution is SOC 2, ISO 27001, PCI DSS, and GDPR compliant, with 256-bit SSL encryption and regular VAPT testing. You also get access to industry-specific support from expert who understand the nuanced demands of the payments and cards ecosystem.

{{banner1}}

FAQs on Payment Reconciliation

1.What is an example of payment reconciliation?

A common example is payment gateway reconciliation, where you compare the sales recorded on your website with the settlement report from a payment gateway like Razorpay. You verify if the amount you received matches the transaction total after deducting fees or refunds.

2.Why is daily payment reconciliation important?

Reconciling payments daily allows your finance team to detect discrepancies early and avoid issues piling up over time. It also keeps your cash flow reporting up to date and helps you close books faster with fewer errors.

3.What are the 5 steps to reconcile your account?

The five steps include collecting payment data, matching transactions to records, identifying mismatches, investigating the cause, and updating your books. Following this structure ensures accurate financial reporting and better control over your payment flow.

4.How to avoid errors in payment reconciliation?

You can avoid errors by standardizing your data formats, reducing manual entry, and using automation tools to match transactions. These steps lower the risk of duplicate entries, missed payments, and incorrect reconciliations.

5.What is the role of AI in Payment Reconciliation?

AI helps automate the matching of payments across systems, flags potential issues in real-time and learns from past patterns. This improves reconciliation speed, accuracy, and allows your team to focus on higher-value financial tasks.

6. Why do businesses need payment reconciliation?

Businesses need payment reconciliation to make sure their records match the money that actually moved. It shows what came in, what went out, and what’s still pending. This clarity helps teams plan better, avoid mistakes, reduce risk, and keep a clean audit trail behind every transaction.