The Different Types of Reconciliation Used in Accounting?

Introduction

Financial institutions often encounter considerable losses losses due to reconciliation errors. For bank and credit union executives like you, these errors aren't just revenue leakage—they represent compliance risks and operational inefficiencies that impact your bottom line.

As your organization scales, reconciliation becomes challenging due to the growing volume and complexity of financial transactions. Instead of using spreadsheets, banks now need sophisticated systems to manage the volume of financial transactions they handle. The complexity is further magnified due to changing customer expectations and the rapid evolution of omnichannel payment technologies.

For institutions planning digital transformation initiatives, understanding the different kinds of reconciliation processes will help them implement the right automation tools.

This article explores reconciliation from an accounting perspective, explains how it works, breaks down the different types of reconciliations, and explains why its importance continues to grow. We'll also introduce how Osfin can simplify and accelerate the entire reconciliation process.

What is reconciliation in accounting?

Reconciliation in accounting is the process of comparing financial records across various systems to make sure everything is correct. Think of it as financial fact-checking—making sure what your internal systems show matches with what external sources report.

For your bank or credit union, reconciliation ensures that the transactions recorded in your core banking system match with those from payment processors, and correspondent bank statements.

Consider what happens when a customer deposits a $50,000 check through your bank’s mobile app on a late Friday evening. Your deposit system might credit their account immediately, but the actual funds may settle only by Monday morning. Without proper reconciliation, this timing difference creates a discrepancy between your customer-facing systems and your cash position.

Good reconciliation practices identify these routine timing differences and differentiate them from actual errors or fraud. This verification method is vital for ensuring accurate financial statements, passing regulatory scrutiny, and making sound business decisions based on reliable data.

How Does Reconciliation Work?

Here's how reconciliation works in a typical financial organization:

Collection of Financial Documents: The reconciliation process begins with the collection of various financial documents, like internal company ledgers, subledgers , bank statements, and vendor invoices.

Manual or Automated Matching: Depending on the volume and complexity of transactions, matching can be done through spreadsheets manually, or automation tools like Osfin can be set to match based on the date, amount, and reference ID.

Identification of Unmatched Entries: The system flags off unmatched entries, which can include pending settlements, timing differences, keystroke mistakes, or unauthorized activity.

Variances and Their Resolution: Each discrepancy is verified. Some require straightforward fixes, like internal booking of bank fees—others will require more extensive investigation.

Adjustment to Journal Entries: Identified discrepancies require matching corresponding entries to the accounting system.

Document your findings and adjustments made to support necessary audit trails.

Consider this example of a standard bank account reconciliation:

Financial institutions must ensure that they have clear reconciliation schedules based on risk and volume. High-value, high-risk accounts typically require daily reconciliation, while lower-risk accounts might be reconciled weekly or monthly.

In today's world, there are several AI-based tools to assist in automating the above reconciliation steps. These tools help to minimize human errors and make the process faster and more efficient.

What are the various types of reconciliation?

Bank Reconciliation

Bank reconciliation for financial institutions involves verifying cash positions across correspondent banks, Federal Reserve accounts, and clearing networks. This process ensures your institution's recorded cash balances match external banking relationships and regulatory requirements.

- Confirms accurate cash positions for liquidity management and regulatory compliance

- Identifies timing differences in wire transfers, ACH settlements, and check clearing

- Prevents overdrafts in correspondent accounts that could damage banking relationships

Loan Portfolio Reconciliation

Loan reconciliation matches individual loan records in your core banking system against the general ledger and regulatory reports. This process ensures accurate loan balances, interest calculations, and proper classification.

- Verifies accurate loan balances for financial reporting and regulatory calls

- Ensures proper interest accrual and payment application

- Maintains accurate allowance for loan losses calculations

Card Services Reconciliation

Card reconciliation matches debit and credit card transaction processing with settlement accounts and customer postings. This complex process handles high-volume, small-dollar transactions across multiple systems.

- Reconciles card processor settlements with general ledger entries

- Ensures accurate customer account postings for card transactions

- Tracks interchange income and processing fees

Customer/Accounts Receivable Reconciliation

Customer reconciliation matches payments received against services delivered and fees charged to the customers to ensure complete revenue recognition. This verification ensures you're collecting all the revenue you've earned from the customers.

- It tracks missed fee collections from wealth management and commercial services.

- It ensures accurate recording of loan payments and interest income.

- It supports compliant collections processes and customer account histories.

Osfin's invoice reconciliation module helps banks and credit unions track and verify all customer payments against services provided to them.

Investment Account Reconciliation

Investment reconciliation verifies that your institution's investment portfolio records match custodial statements and market values. This process ensures accurate valuation of often significant portions of your balance sheet.

- Verifies ownership and existence of all securities.

- Ensures accurate recording of interest, dividends, and market value changes.

- Confirms compliance with investment policies and risk limits.

Osfin's advanced reconciliation platform handles even the most complex multi-step reconciliation processes. These tools help in reducing manual effort while improving accuracy.

For more information about Osfin's complete reconciliation solutions, visit www.osfin.ai.

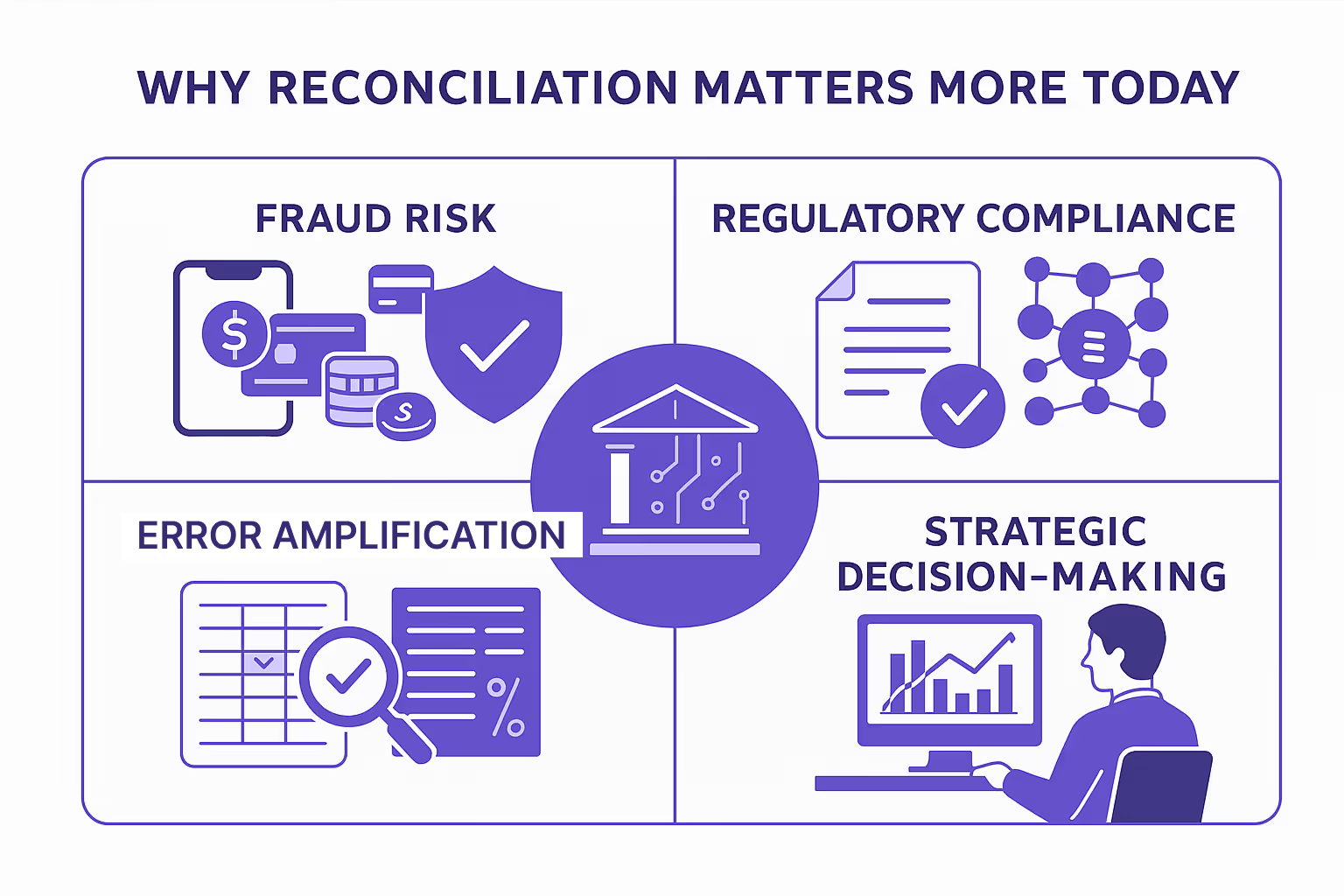

Why Reconciliation Matters More Than Ever

Reconciliation has gained critical importance in a world where transaction methods are becoming increasingly automated and technology changes are rapid.

Here are some of the reasons why reconciliation is growing in relevance:

Increased Risk of Fraud: Growth in digital transactions creates more avenues for fraud. Regular reconciliations serve as a security blanket against this.

Regulatory Challenge: firms need to provide accurate records and reconciliations to meet emerging regulatory requirements

Errors Amplify: In fast-paced transaction environments and large-scale banks, minor errors in financial systems can multiply quickly, potentially impacting financial integrity and reputation.

Enabling Decision-Making: Accurate and updated data helps management teams to make informed strategic decisions.

In simple terms, strong practices for reconciliation act as the backbone of the financial health and resilience of the company.

For example, a regional bank in the Southwest region improved its reconciliation processes after auditors flagged weaknesses during a routine examination. Their new approach not only satisfied regulators but also identified $280,000 in missed fee income and prevented duplicate vendor payments worth $45,000 annually.

As transaction volumes grow and payment methods multiply, robust reconciliation processes have become non-negotiable for financial institutions navigating today's complex environment.

How Osfin Can Help

Osfin recognizes that reconciliation is about streamlining your financial operations, not just another task. Our cutting-edge reconciliation solutions improve accuracy, reconcile payments, and unify data.

- Automated Data Fetching & Matching: We have tools that automatically retrieve and compare data from various sources.

- High Speed Processing

- Real-Time Alerts: Receive immediate alerts when a discrepancy arises, enabling you to take appropriate action.

- Prepare thorough reports that ensure transparency and traceability, making them audit-ready.

FAQs about Reconciliations

What is the recommended frequency for performing different types of reconciliation?

Financial institutions should tailor reconciliation frequency to risk level and transaction volumes. High-risk, high-volume accounts (like correspondent relationships and settlement accounts) require daily reconciliation. Investment portfolios typically need weekly verification, while vendor accounts can be reconciled monthly. Digital transformation has made daily reconciliation increasingly practical for more account types, reducing risk exposure and improving financial accuracy.

What are typical reconciliation mistakes, and how can we avoid them?

Common errors include timing differences between systems, manual entry mistakes, duplicate transaction recording, and improper account coding. Prevent these by implementing standardized cut-off times, automating manual processes, establishing unique transaction identifiers, and creating clear account coding guidelines. The most effective prevention combines solid policies, proper staff training, and system automation, along with a meaningful supervisory review of reconciliation results.

How can financial institutions transition from manual to automated reconciliation?

Start by documenting current reconciliation processes in detail and identifying pain points. Implement automation in phases, beginning with high-volume reconciliations while maintaining parallel manual processes initially. Ensure staff understand that automation changes their role from data processors to exception handlers and analysts. Develop clear procedures for resolving exceptions flagged by automated systems. Success depends on viewing the process as a business transformation project rather than just a technology implementation.

What key metrics should be tracked to measure reconciliation efficiency?

Track the time to complete each reconciliation type; monitor the percentage of accounts reconciled within target timeframes, the number of unresolved items and their aging, the exception rates by reconciliation type, and the cost per reconciled transaction. We should monitor these metrics over time to identify trends and improvement opportunities. Leading institutions establish benchmarks for each metric and regularly review performance against these standards to drive continuous improvement.

How does reconciliation differ between community institutions and larger financial organizations?

Reconciliation principles are consistent regardless of size; community banks and credit unions face resource constraints but benefit from simpler structures. Larger institutions manage greater complexity with more accounts and systems but typically have dedicated reconciliation teams. Both larger and smaller institutions face similar regulatory expectations; however, examiners may scrutinize larger institutions more intensely. Regional and community institutions can often operate more efficiently by automating high-volume reconciliation tasks.