Step-by-Step Guide to Closing Entries in Accounting

Monthly. Quarterly. Annually.

At the end of every financial period, accountants need to perform dozens of actions to ensure an organization's financial books are accurate and reflect its actual performance. One such activity is making closing entries.

Closing journal entries help wrap up the accounting period by shifting balances from temporary accounts, like revenues and expenses, into permanent ones.

Why?

To ensure the books are reset and ready for the next period.

In this article, we'll explore what is a closing entry in accounting, how to do a closing entry, when to make them, examples, and more.

What this blog covers:

- What closing entries are and their role in the accounting cycle

- The four main steps of preparing closing entries

- Examples of journal entries for revenues, expenses, income summary, and dividends

- Impact of closing entries on financial statements and retained earnings

- Common errors to avoid when recording closing entries

- Best practices for accuracy and efficiency in the closing process

- How automation can simplify and streamline closing entries

What are Closing Entries in Accounting?

Here's a simple closing entries definition to understand what they mean. They are special journal entries that move money out of temporary accounts, like revenue and expenses, and into permanent accounts, like capital or retained earnings.

This is done because temporary accounts only reflect the activity for one period. Once that period ends, these accounts need to be reset to zero so they can start fresh in the next cycle. Permanent accounts, on the other hand, carry balances forward and show how the business is doing over time.

Temporary accounts typically include:

- Revenue accounts: All the income earned during the period

- Expense accounts: All the costs paid during the period

- Drawings or dividends: Amount withdrawn by the owner or paid to shareholders

- Income Summary account: A temporary account used to manage profit or loss before moving it into retained earnings or capital

Purpose of Closing Entries

Accounting closing entries serve various purposes:

- Resetting temporary accounts: Accounts like revenue, expenses, and dividends are designed to capture activity for a single period. Closing entries bring their balances back to zero, ensuring the next period starts fresh.

- Updating retained earnings: General journal closing entries transfer the net income/loss for the period, along with any dividends or owner withdrawals, into retained earnings or capital account. This ensures the equity section of the balance sheet is always up-to-date.

- Supporting accurate financial reporting: Closing entries clear temporary accounts and update permanent ones. This ensures financial statements reflect the company's actual performance at the end of the period.

When are Closing Entries Made?

Closing entries in accounting are made at the end of the period after all adjusting entries are completed and financial statements have been prepared. This is because temporary accounts still retain their balances until the reports are finished. Once the statements are ready, their balances can be transferred into permanent accounts without affecting the numbers.

The timing of when closing entries are made matters for two main reasons:

- Making a closing entry at the end of the accounting period ensures the income statement and balance sheet reflect the company's real performance for that period.

- Resetting temporary accounts ensures the books are ready to capture fresh activity in the new period without carrying forward any balances.

Types of Accounts Affected by Closing Entries

Closing entries in accounting do not alter every account in the books. They only affect certain accounts that need to be reset at the end of each period. These include:

- Revenue accounts: These accounts track the money a business earns during the period from selling products, providing services, or earning interest. At the end of the period, all revenue balances are closed so they don't carry over into the next cycle.

- Expense accounts: These accounts show the expenses incurred for running the business and generating revenue. For example, rent, salaries, depreciation, etc. Just like the revenue account, the expense account is also temporary, which means its balance is reset through closing entries, too.

- Dividends or withdrawals: For large corporations, this represents profits distributed to shareholders as dividends. Whereas, in partnerships or sole proprietorships, it is the amount owners take out for personal use. These accounts are also closed to make sure they don't carry forward into the new period.

- Income Summary account: This account is only used for the closing process. Revenues and expenses are first transferred here to calculate the net income or net loss. Once that is done, the balance of the Income Summary is moved into retained earnings or the capital account.

Now that you know the different accounts involved, let's look at how to do closing entries in accounting.

{{banner3.1}}

Step-by-Step Process for Preparing Closing Entries

If you're wondering how to prepare closing entries, worry not, because it isn't a complicated process. All you need to do is understand the steps involved in clearing the books. Here's how to record closing entries:

Step 1: Close Revenue Accounts

The first step in preparing a closing entry is to move all balances from revenue accounts into the Income Summary account. This includes sales revenue, service revenue, and any other income earned during the period. This step helps you reset the revenue accounts back to zero and record the total revenues in a single place.

Step 2: Close Expense Accounts

Next, move the balances of all expense accounts into the Income Summary account as well. These include items like rent, utilities, salaries, etc. Once you've transferred the balance, the Income Summary will reflect both the total revenues and the total expenses for the period.

Step 3: Close the Income Summary Account

At this stage, the Income Summary will show you if the business earned a net profit or incurred a net loss. You need to move this balance to the retained earnings account or the capital account. Closing the Income Summary ensures that revenues and expenses don't remain on the books, and the results flow into equity.

Step 4: Close Dividends or Withdrawals

The last step in preparing a closing entry is to transfer the dividends or withdrawals into retained earnings or capital. This shows how much of the profit was distributed and reduces the retained earnings balance accordingly.

Once you've completed these four steps, all temporary accounts will be reset to zero, leaving you with clean books for the next accounting cycle.

Closing Entry Examples

Let's look at a general journal closing entry example to see how it actually works. Say Company AB Ltd. has the following balances at the end of the accounting period:

- Revenue: $50,000

- Expenses: $35,000

- Dividends: $5,000

Here's how to do closing entries for the company:

1. Close Revenue Accounts

The first step is to clear the revenue balance. AB Ltd. will debit Revenue for $50,000 and credit the Income Summary for the same amount. This resets the revenue account to zero.

2. Close Expense Accounts

Next, all expense balances need to be transferred. AB Ltd. debits the Income Summary for $35,000 and the various expense accounts (utilities, rent, etc.) to bring them down to zero.

3. Close the Income Summary

At this point, the Income Summary has a credit balance of $15,000 ($50,000 - $35,000). To close it, AB Ltd. debits the Income Summary for $15,000 and credits Retained Earnings for the same amount. This moves the net income into the company's equity.

4. Close Dividends

Finally, AB Ltd. needs to account for shareholder distributions. It will debit Retained Earnings for $5,000 and credit Dividends for $5,000, reducing equity by the amount paid out.

After completing these steps, all temporary accounts will be at zero, and AB Ltd.'s retained earnings will show the actual net effect for the year. This closing entries example makes it easier to understand how the process works. Let's now look at how do closing entries affect the balance sheet and other financial statements.

How do Closing Entries Affect the Financial Statements?

Closing entries may seem like a small activity behind the scenes, but they have a huge impact on the financial statements. They bridge the gap between the last accounting period and the next one, ensuring the numbers reflect the organization's performance accurately. Here's how:

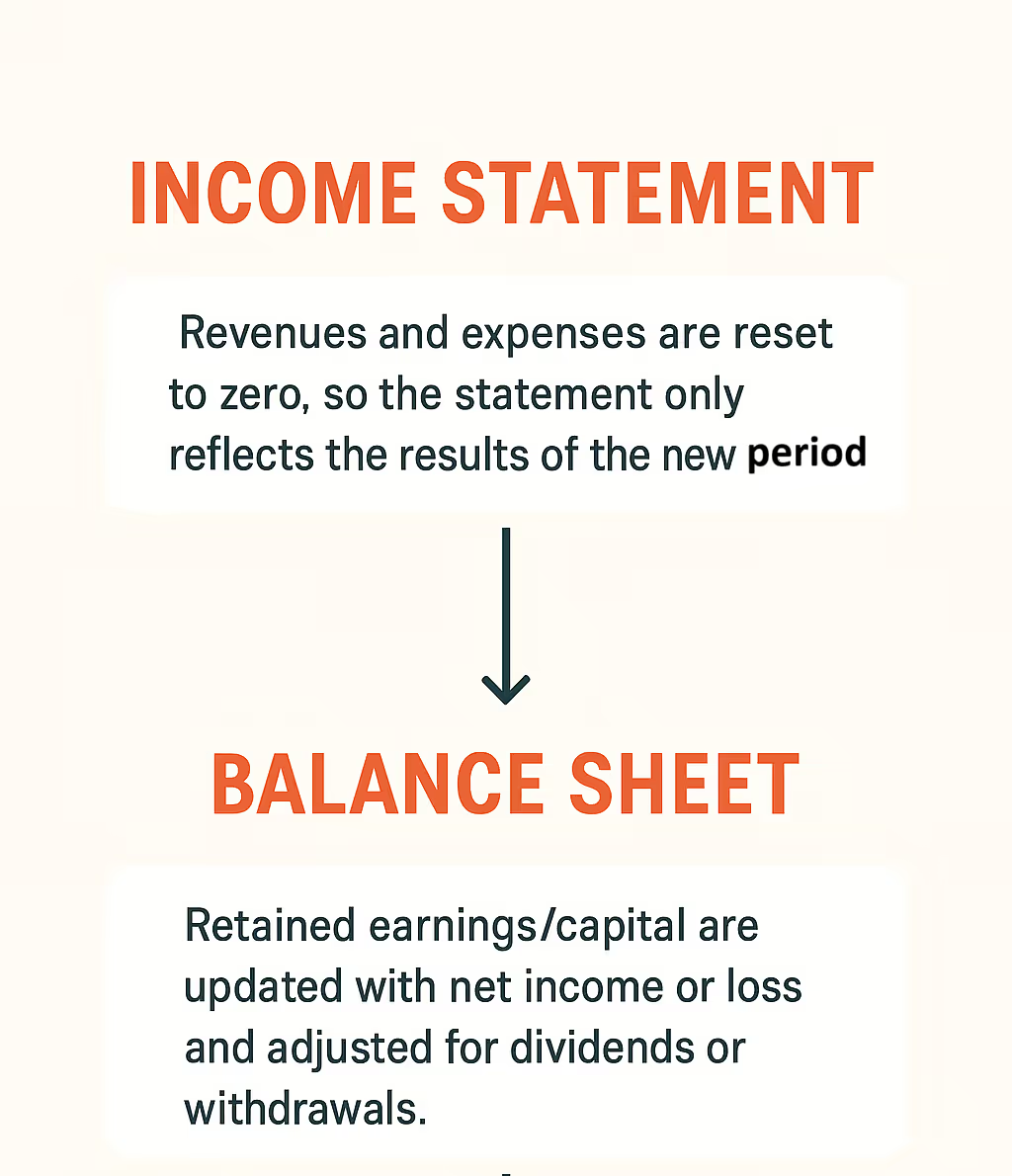

- Income statement: Once the revenues and expenses are closed, those accounts are reset to zero. This means the income statement for the next period starts fresh. It only shows the results of that specific period instead of carrying forward old balances.

- Balance Sheet: Closing entries update the retained earnings or capital to include the net profit or loss from the closed period, along with dividends or withdrawals. This change also reflects in the equity section, ensuring the balance sheet aligns with the company's actual financial standing.

Closing entry accounting ensures the financial statements are reliable, making it easier to judge how well the business is actually doing.

Common Mistakes in Closing Entries

After understanding the meaning and looking at some closing entries examples, the process might seem straightforward. However, you must be mindful of some common mistakes to avoid slip-ups. Here are some common pitfalls to watch out for:

1. Leaving Temporary Accounts Open

One of the most important things to keep in mind is that revenue, expenses, and dividends should all be reset to zero at the end of the period. If even one of them is overlooked, it will impact the results for the next period.

2. Miscalculating the Income Summary Balance

No matter how careful you are, errors are bound to happen. And any mistake in adding up revenues or expenses can lead to the wrong net income/loss being carried forward. Therefore, it's important to review the numbers carefully before transferring balances.

3. Closing in the Wrong Sequence

Remember the step-by-step guide and example of closing entries? Well, you need to follow the process in the exact same order. Start with revenue, then expenses, followed by the Income Summary, and finally dividends or withdrawals. Mixing up the order can affect the results.

4. Not Updating Retained Earnings

The Income Summary doesn't provide a complete picture by itself. You need to close it into retained earnings or capital. If you miss this step, you'll leave equity incomplete.

5. Posting Without Review

Just because you know how to do closing entries in accounting doesn't mean you shouldn't be careful. By posting entries directly without running a final check, you risk overlooking errors that will make their way into the financial reports.

Best Practices for Closing Entries

Just knowing what is a closing entry and looking at some closing journal entries examples isn't enough. You must also follow some best practices for a seamless process with accurate results:

- Invest in accounting software: Accounting tools can simplify the entire process by automating calculations. They're also great for ensuring accuracy.

- Automate routine closings: Instead of manually entering the same adjustments month after month, set up automated journal entries to save time and lower the risk of manual errors.

- Reconcile before closing: Make sure every bank statement, invoice, and expense is accounted for. Proper financial reconciliation will ensure you don't carry forward inaccurate data.

{{banner2}}

Automating Closing Entries with Osfin

While preparing closing entries isn't a complicated process, it can become complicated if your data is inaccurate or scattered across different systems. Osfin takes away this hassle. Here's how it helps you automate closing entries:

- Importing data (ingestion): Osfin is a file format-agnostic platform with more than 170 integrations. This means it can access data from multiple sources, no matter how it is stored. While doing this, it applies custom deviation tolerances to weed out poor-quality data and detects duplicates and outliers.

- Reconciliation process: Once the data is in, Osfin uses logic-based matching to handle both one-to-many and many-to-one transactions. It can reconcile up to 30 million records in just 15 minutes and even auto-matches payment gateway reports.

- Exception handling: Osfin automatically flags unmatched transactions, assigns them the right reason, and routes them to the right team member through its built-in exception handling engine.

- Output: Osfin also delivers detailed, compliance-ready reports. Plus, it is backed by 256-bit encryption, role-based access, and two-factor authentication, while staying compliant with SOC 2, PCI DSS, ISO 27001, and GDPR.

To Sum Up

Understanding what are closing entries and their purpose is essential to maintain accurate, reliable financial records. Following the process, learning from closing entries accounting examples, and using the right tools can help you simplify month and year-end closings without any errors.

If you're looking to streamline reconciliations for closing entries, Osfin can help. It offers automated workflows, real-time visibility, and solid compliance checks, so you can manage your financial books stress-free.

Book a demo to enhance your closing process with Osfin.

FAQs on Closing Entries

1. What are the 4 closing entries?

The four closing entries are:

- Closing revenue accounts to the Income Summary.

- Closing expense accounts to the Income Summary.

- Transferring the balance of Income Summary to Retained Earnings or Capital.

- Closing dividends or drawings to Retained Earnings.

2. How to do closing entries step by step?

To prepare a closing entry, start by adding all revenue accounts and moving the total to the Income Summary. Then, do the same for expenses. Post the difference between revenue and expenses to Retained Earnings or Capital. Finally, reduce Retained Earnings by the amount of dividends or drawings.

3. What is the purpose of closing entries?

Closing entries aim to reset temporary accounts like revenues and expenses back to zero. This ensures each new accounting period starts fresh without leftover balances from the past.

4. After the closing entries, which account would still have a balance?

Only permanent accounts, such as assets, liabilities, and equity, will retain their balances after the closing entries.