Dispute & Chargeback Management with Automation

Introduction

Disputes and chargebacks have evolved from an operational problem to a strategic challenge. In 2023, the global cost of chargebacks reached $117 billion, impacting every participant in the payments ecosystem. Banks, e-commerce platforms, and payment processors all face mounting pressure to manage these costs while meeting escalating customer expectations for rapid resolution.

The traditional approach to dispute management cannot scale with today's transaction volumes. Manual processes that require 45 days for resolution clash directly with customer demands for same-day resolution. This disconnect drives customer defection to competitors who promise faster, more transparent dispute handling. For payment processors managing millions of transactions daily, and e-commerce companies protecting razor-thin margins, inefficient dispute management directly impacts bottom-line performance.

Leading organizations are transforming dispute management through intelligent automation. These solutions consolidate data from multiple sources, apply consistent decision logic, and maintain comprehensive audit trails. Early adopters report 75% faster resolution times and 60% reduction in operational costs, while simultaneously improving compliance posture and customer satisfaction metrics.

This guide examines how automation addresses the dispute challenge across financial services and e-commerce. We'll explore implementation strategies, analyze ROI metrics, and provide actionable insights for executives evaluating automation solutions for their organizations.

What this blog covers:

- What dispute and chargeback management is and why it’s crucial for merchants & financial institutions

- The lifecycle of a chargeback: dispute initiation, evidence submission, resolution

- Common causes of chargebacks and disputes (fraud, delivery issues, billing errors)

- Best practices for preventing and managing chargebacks effectively

- How automated dispute management software enhances efficiency, reduces losses

- How Osfin supports end-to-end chargeback and dispute workflows

What Are Disputes and Chargebacks in Banking and Payments?

Disputes occur when cardholders question transactions appearing on their statements, triggering a formal review process with their issuing bank. Common triggers include unauthorized transactions, billing errors, duplicate charges, or quality issues with goods and services. For example, a customer sees a $500 charge for electronics they never received—they file a dispute with their bank, which investigates by gathering transaction evidence from the merchant. If the merchant cannot prove delivery, the bank converts the dispute into a chargeback, forcibly reversing the transaction. This chargeback process follows strict network rules and timelines, involving the cardholder's bank (issuer), merchant's bank (acquirer), and card networks like Visa or Mastercard. Beyond the reversed transaction amount, each chargeback generates $20-100 in processing fees, operational costs, and potential network penalties for excessive chargeback ratios.

Why Manual Handling Slows Down Dispute Resolution?

Manual dispute handling creates expensive delays across the payment ecosystem. Investigation teams must access 5-7 different systems for each dispute—core banking for account data, payment gateways for transaction details, fraud systems for risk scores, and network portals for compliance rules. This system-hopping wastes valuable time and increases resolution costs for banks, e-commerce platforms, and payment processors alike.

The numbers tell the story. Agents spend 70% of their time gathering data instead of resolving disputes. A simple $200 chargeback requires 45 minutes of manual data collection across platforms. When agents copy information between systems, error rates hit 15%, forcing costly rework. For e-commerce companies handling thousands of disputes monthly, these inefficiencies translate to significant operational overhead and delayed fund recovery.

Also, manual procedures are not highly scalable. So, with the growth of transaction volume, the number of disputes also increases. Businesses cannot operate freely without automated processes, and they run the risk of employee turnover and burnout. These bottlenecks can eventually delay response times and reduce the effectiveness of the company’s efforts to resolve disputes.

Manual handling can also limit the company’s visibility into performance metrics. If the company does not have integrated systems, it will struggle significantly to identify recurring issues and analyze reasons for these disputes.

What is Dispute & Chargeback Automation?

Dispute and chargeback automation replaces manual processes with intelligent technology that connects all your systems. Instead of agents checking multiple platforms, automation pulls data from banking systems, payment gateways, and networks into one unified view. The platform uses AI and business rules to classify disputes, gather evidence, and make decisions automatically.

For routine disputes, the system handles everything—from initial review to final resolution—without human touch. Complex cases get routed to specialists with all data pre-assembled. The technology maintains real-time network connections, ensures compliance deadlines, and generates required documentation automatically. This creates a scalable solution that processes growing volumes without adding staff, while reducing errors and speeding resolution from weeks to hours.

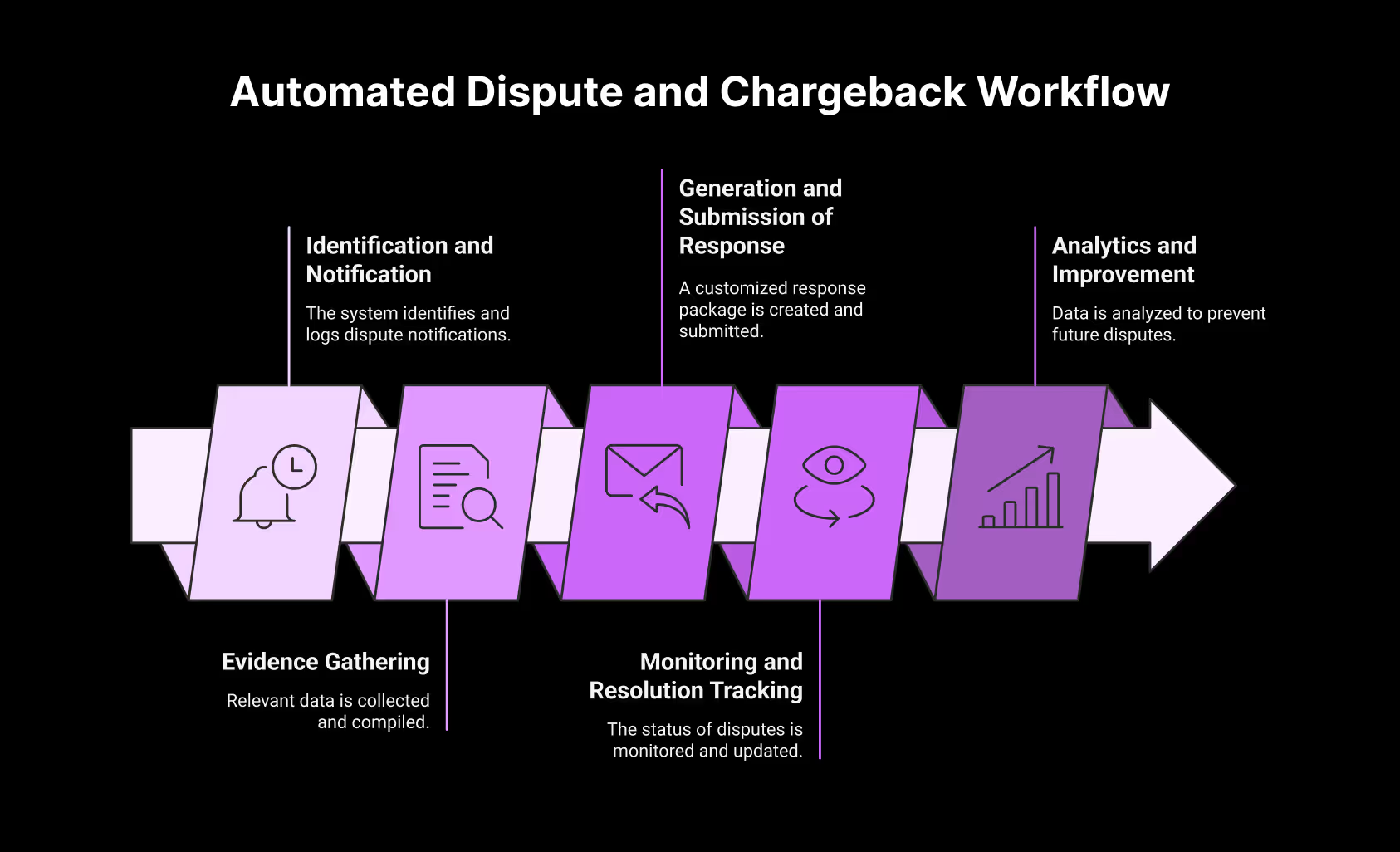

Automated Workflow: From Identification to Resolution

Automated workflow for the disputes and chargebacks management can streamline the entire lifecycle. It starts with initial identification and ends with the final resolution. It can replace manual tasks with several rules-based as well as highly intelligent systems.

The entire workflow includes steps like

Step 1: Instant Dispute Capture Customer files dispute through any channel—mobile app, online banking, or call center. The system automatically creates a case, assigns tracking number, and sends confirmation within seconds. No manual data entry required.

Step 2: Intelligent Data Aggregation

The platform simultaneously pulls data from all relevant sources: core banking, payment processors, merchant information systems, and receipt images from electronic journals. Complete case file assembled in under 60 seconds.

Step 3: AI-Powered Classification In Advanced AI-driven financial operations systems like Osfin, machine learning models analyze dispute characteristics—amount, merchant type, customer history, transaction pattern. The system categorizes dispute type, determines applicable rules, and predicts likely outcomes. High-risk cases flagged for priority handling.

Step 4: Automated Validation System validates claims against network rules and checks for duplicate disputes. It also verifies timeline compliance, and confirms documentation completeness. For clear-cut cases like proven fraud, immediate steps are initiated.

Step 5: Smart Resolution Routing Simple disputes (non-receipt, duplicate charges) process straight through with automated decisioning. Complex cases route to specialists with pre-assembled data and recommended actions. The system maintains SLAs and escalates when needed.

Step 6: Execution and Communication Approved resolutions execute automatically—credits post to accounts, chargebacks initiate through networks, merchants receive notifications. Customers get real-time updates via preferred channels. Complete audit trail captured for compliance.

How does automation reduce turnaround time (TAT) and improve accuracy?

Automation can easily reduce TAT, or turnaround time, greatly. It can improve accuracy in dispute and chargeback management in several ways. Such as streamlining data handling and processing, eliminating manual bottlenecks, ensuring adherence to regulatory timelines, etc.

For instance, a company that uses AI-powered systems can enjoy a reduction in operational time spent on case reviews of around 50%.

Here’s how automation can reduce TAT and improve accuracy:

- Faster Turnaround Time

Integrated systems can fetch relevant transaction data, customer communications, supporting documentation, etc., from several reliable sources. Such capabilities can reduce the time required to both compile and review evidence greatly. Also, automated systems can generate and submit responses in time. They can thus ensure that businesses adhere to the stringent deadlines set by card networks. Thus, automation completes all significant tasks within a few minutes.

- Improved Accuracy

Manual processing may offer scope for human errors. Those may include misinterpretation of reason codes, choosing the wrong documents, biases, missing deadlines, etc. Any of these errors can result in rejected responses, along with financial losses.

With automation, companies can successfully minimize these risks by offering workflows that can ensure several conditions, such as including correct documents, meeting all conditions, timely submissions, etc.

Moreover, automation tools can use machine learning to find anomalies or potential issues. These AI-powered tools can improve the quality of dispute responses further.

Impact on Operations and Customer Support Teams

The automation of dispute and chargeback solutions can have a positive impact on both operations and customer support teams. Here’s how it can help:

For Operations Teams

Automation can simplify time-sensitive and complex procedures related to dispute and chargeback management for credit cards. Tasks like retrieving data, preparing documents, and case tracking are usually handled by the system. These automation tools can eventually minimize the need for human intervention.

Such a tool can accelerate the entire resolution procedure, leaving operations teams time for more complex and time-sensitive cases. Operational teams can also benefit from automated alerts, real-time dashboards, etc. These features can enhance the process of making decisions and monitoring performance.

For Customer Support Teams

Dispute automation can help customer support teams by freeing them from time-consuming backend procedures. With the help of integrated systems, agents can view transaction details, access case statuses, and even offer updates rapidly. These AI-powered tools can eventually improve response time and allow agents to resolve client issues more efficiently.

Real-World Use Cases of Automation in Banking Disputes

According to Gartner, the adoption of AI in finance sectors has increased by 58% in 2024. So, let’s see a few real-world use cases of automation in banking disputes:

- Payment Processors

Many payment processing companies use AI within their automated workflows. Such systems can easily predict dispute outcomes, along with potentially fraudulent claims. Thus, companies can resolve issues accurately and optimize resource allocation.

- E-Commerce Platforms

Online marketplaces face thousands of disputes daily due to high transaction volumes. with automation, these companies can review chargeback claims carefully. Those include order details, confirmation of delivery, and also records of customer communication.

Moreover, automated systems can both prepare and submit responses to card issuers without any human help.

Top Tools Powering Dispute and Chargeback Automation

Several advanced tools can transform the task of dispute and chargeback management. Those include:

- Osfin

Osfin provides financial automation solutions specializing in chargeback and dispute management. The AI-powered platform streamlines reconciliation, enhances transparency, and reduces revenue leakage across payment ecosystems through real-time transaction reconciliation.

- Chargebacks911

This platform can manage disputes and chargebacks with a comprehensive approach. It includes several crucial features and solutions for all types of merchants. This platform focuses on both pre- and post-solutions for chargebacks. Hence, it can help companies by protecting against fraud.

- Kount

It is one of the most popular providers of chargeback management solutions. It can offer a holistic view of disputes and chargebacks. Hence, it helps companies to resolve disputes quite successfully.

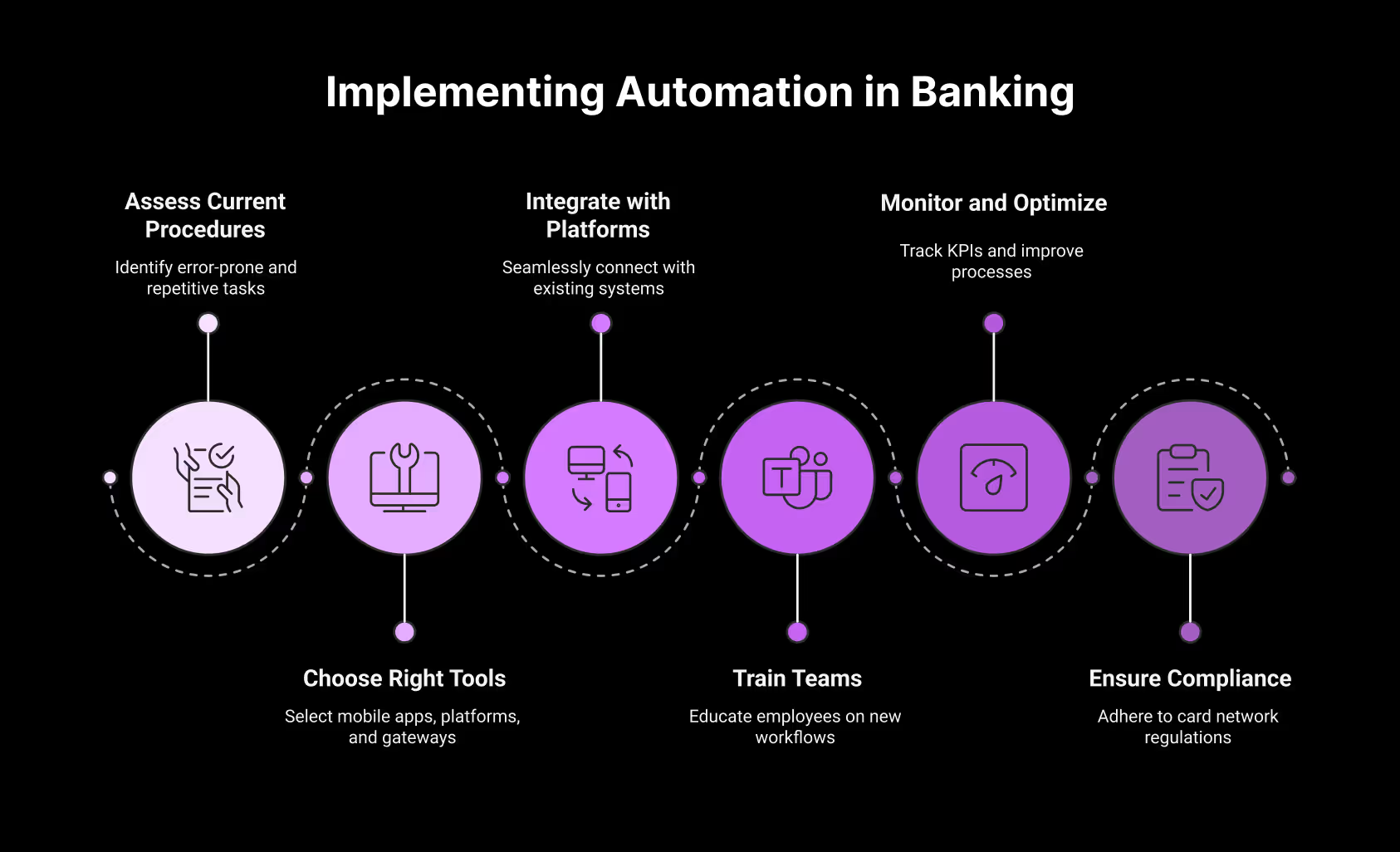

How to Adopt Automation in Your Bank or Payment System

To automate your payment system effectively, you have to start by assessing your current procedures. These audits will help you identify both error-prone and repetitive tasks. Then, you have to choose the right tools.

Those must include mobile banking apps, online banking platforms, payment gateways, etc. All these will ensure strong security measures.

The entire procedure will need some important steps, like

- Assessing your business needs: You must start by carefully evaluating your needs regarding dispute and chargeback automation workflows.

- Choosing the Right Tools and System: Next, choose the right tools and system.

- Proper integration with existing platforms: Integrate your automation tools seamlessly with your core banking system, CRM, fraud detection tools, payment gateways, etc.

- Training your teams: Train your employees on the new automated workflows and the right tools.

- Monitor and Optimize: Try to monitor and track key performance indicators. Also, use the automation platform to continuously optimize the procedures.

- Staying compliant: Ensure that your business follows all the card network regulations.

Conclusion

Disputes and chargebacks are a significant issue for many companies that accept online transactions. Therefore, companies must manage these issues effectively and utilize the appropriate tools to prevent losses. Automation in dispute and chargeback management can help businesses automate and streamline the entire chargeback procedure and eventually recover lost revenue.

FAQs

Can automation handle high-value or complex disputes?

Automation handles data gathering and initial analysis for all disputes, but high-value cases still route to senior agents for final decisions. The system pre-assembles all evidence and provides recommendations, allowing experts to focus on judgment rather than data collection.

Will automation replace our dispute management team?

No, automation enhances your team's capabilities rather than replacing them. Staff shift from repetitive data gathering to handling complex cases, improving merchant relationships, and analyzing dispute trends to prevent future issues.

How does automation ensure regulatory compliance?

Automated systems have built-in compliance workflows that track all regulatory deadlines and automatically issue provisional credits when required. Every action is logged with timestamps, creating perfect audit trails for regulatory examinations.

How long does it take to implement dispute automation?

Most banks and payment processors complete implementation in 3-6 months. This includes system integration, testing, and team training. Starting with a pilot program for specific dispute types can show results within 8-12 weeks.