What is Recoupment in Banking? A Critical Look at Offsets and Recoveries

In FY23, Indian banks recovered just 15% of their non-performing assets (NPAs) through all recovery mechanisms, highlighting the urgency for more effective recoupment strategies.

These are challenges frequently faced by banking and finance professionals. Debt recovery, offsets, and recoveries, when manually tracked, can become a significant challenge, especially when supplemented by regulatory pressures.

In today’s financial scenario, recoupment is the route to getting back lost finances. It is a disciplined framework for sustaining cash flow and ensuring compliance. Understanding what recoupment is can help you implement more efficient offset and recovery strategies.

This article will discuss what recoupment is in finance and banking, its importance and impacts, types and implications. Additionally, we will examine how automation through Osfin can streamline tracking and execution for recoupment.

What this blog covers:

- What recoupment in banking means and how it works in financial operations

- Common scenarios: over-payments, refunds, contract breaches and how banks recover funds

- Key risks and control points for recoupment processes

- Best practices for managing recoupment in banking operations

- How automation and software (like Osfin) help streamline recoupment workflows

Understanding Recoupment in Financial Operations

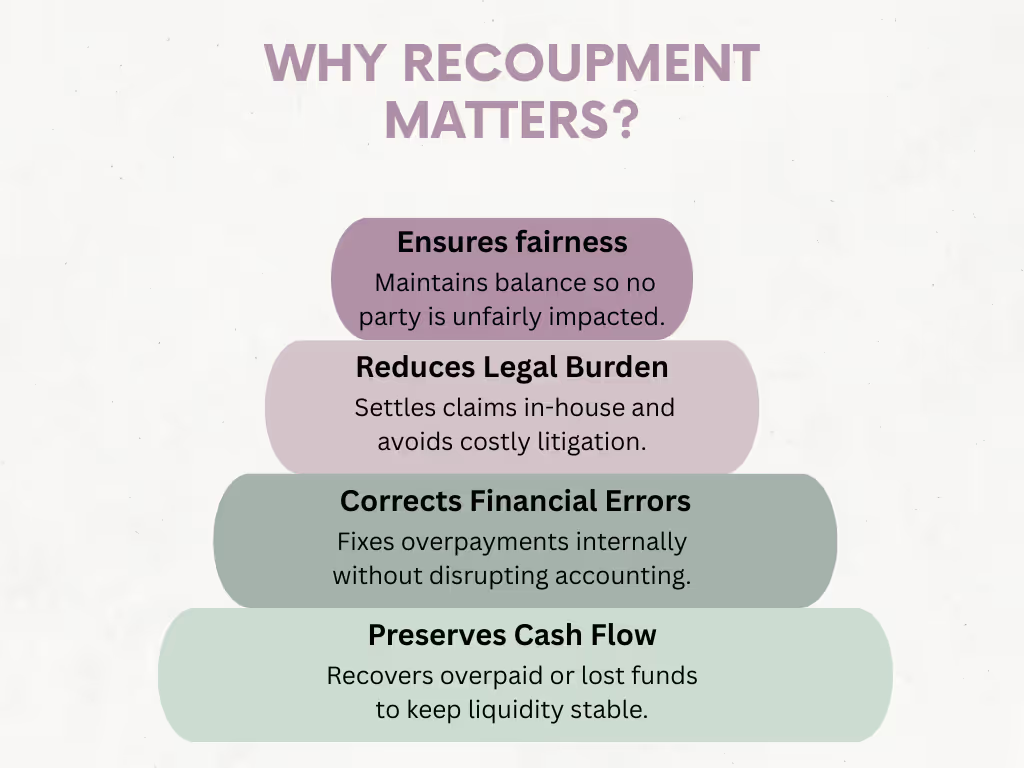

In this section, we’ll explore how recoupments have become a significant part of modern day financial operations. Here are some key points on how they contribute to FinOps:

- Preserves Cash Flow: First, recoupment assists businesses and banks in recovering money. This correction mechanism for transaction errors is critical to maintaining liquidity, hence cash flow.

- Corrects Financial Errors: Businesses can eliminate overpayments internally. This means error correction without disruptions to the accounting flow and audit complications. For scaling financial operations, this can save immense amounts of time.

- Reduces Legal Burden: Next, recoupment provides a direct route to settle overpayment claims, minimizing costly and prolonged litigation processes. We’ll discuss this further later in the article.

- Ensures Fairness: Recoupment ensures a financial balance between the parties. Any error or overpayment does not unfairly disadvantage one or both, which makes it an important legal safeguard.

These advantages underpin the necessity of recoupment strategies and execution in multiple financial arenas. For businesses and banks, correct reconciliations, and overall regulatory compliance, are all affected by recoupment. We’ll look at these closely in the next section.

How Recoupment Impacts Reconciliation & Compliance

What does recoupment mean for reconciliations and compliance? Recoupment may impact them through inherent record adjusting and error correction techniques. Here are some ways how:

1. Error Corrections:

Recoupment is often used to correct mistakes like overpayments or underpayments. These can show up during audits or internal reviews. By resolving these issues quickly, it helps maintain the accuracy and reliability of financial records.

2. Recovered Costs Adjustment:

When recoupments are successful, they require changes in income statements and balance sheets. This ensures that the company’s financials reflect real, adjusted numbers, whether that’s recovered revenue or corrected losses.

3. Altered Payment Schedules:

Recoupment may result in altered payment schedules, like rent reductions in the future or issuing refunds, thereby affecting financial schedules and reconciliations.

4. Compliance and Audit Support:

A strong recoupment process helps build a clear audit trail. It shows when and why money was recovered. The benefits are multifold: an extensive recoupment workflow supports compliance, makes auditing straightforward, and reduces the risk of fines or regulatory pushback.

5. Legal and Reputational Risks:

Frequent recoupments, especially when caused by unresolved billing issues, can put you or your organization at the risk of legal challenges. Over time, they can also harm an organizational reputation. This can raise concerns among customers, partners, and regulators alike.

When Does Recoupment Happen?

When loan borrowers default, recoupment enables banks to recover the outstanding amount through legal channels or by seizing assets. Here are common scenarios where such recoupment typically occurs:

- When the Loan Turns into an NPA: If the borrower defaults on a payment for more than 90 days, the loan is categorized as a Non-Performing Asset (NPA). Banks can initiate recoupment at this stage by retrieving collateral under the agreed-upon recovery frameworks.

- When Mutual Debts Exist Simultaneously: Recoupment happens when mutual debts exist simultaneously, when both the bank and the customer owe each other. The bank counterbalances its liability by deducting the amount that a customer owes, typically for overdrafts, settlements, or insolvency proceedings.

- When Legal or Asset-Based Recovery is Needed: Banks enforce recoupment by going to court or liquidating the assets when voluntary repayment fails. Such an escalation happens after the usual recovery steps have been exhausted.

Recoupment vs Refund vs Reversal: What’s the Difference?

Refunds, recoupments, and reversals are often confused. Let’s examine the differences in this table:

{{banner1}}

Types of Recoupment

Recoupment can be in different forms based on the type of transaction and the grounds on which the money is restored. Here, we will define recoupment types:

1. Transactional Recoupment

This type occurs due to disputed transactions, chargebacks, and payment reversals. Transactional recoupment is initiated due to customer claims and complaints, seeking a refund of the amounts paid to merchants and recipients.

2. Credit and Loan Recoupment

This type of recoupment includes loan overpayments, defaults, overdrafts, fee adjustments, and collateral liquidation. Its purpose is to recover funds from borrowers through direct offsets, seizure of assets, or adjustments to accounts when repayment terms are violated.

3. Institutional and Regulatory Recoupment

This recoupment includes misuse of government subsidies, grants, financial aid, or other compliance-based recoveries. It aims to return funds to regulatory bodies or institutions when audits reveal anomalies or violations of terms and conditions.

4. Operational or Settlement Recoupment

This type of recoupment includes errors in inter-bank settlements, clearing house reconciliations, and duplicate payments. It aims to resolve intra-party or intra-bank financial discrepancies through structured recovery procedures identified during checks or audits.

Implications and Challenges of Recoupment

With the foundations of recoupment in place, it’s important to understand how it can impact financial and banking operations, and in turn, reconciliation. The implications are twofold, which we will look at here.

Financial Implications

1. Improves Liquidity:

Recoupment strengthens the bank's liquidity. The overpaid money enhances efficiency: it streamlines operations using collection procedures such as lawsuits or debt collection. Note that this makes rapid reconciliation a necessity, given the frequent cash flow adjustments.

2. May Cause Customer Hardship:

On the flip side, it reduces available funds for customers. Unmatched entries become visible in reconciliation reports, potentially leading to financial problems or even a poor relationship with banks.

Legal Implications

1. Risk of Disputes:

Customers can challenge recoupments, potentially leading to legal implications and reputational effects on a bank.

2. Limited to Same Transaction:

Another legal challenge is how recoupment is often limited to claims involving the same transaction. A good reconciliation system should be able to track how recoupment is affecting the numbers within the same transaction lineage.

3. Survives Bankruptcy:

Banks can pursue recoupment even in the midst of or after the declaration of bankruptcy.

The implications of recoupment directly tie to operational challenges. This is especially true in the case of financial institutions dealing with mounting volumes of data. Here are some of the key challenges you should know:

4. Cash Flow Strain and Reconciliation Delays:

High transaction volumes make it harder to recoup funds quickly. Cash flow can reduce, and reconciliation cycles can extend by days or weeks. This is particularly true when either payment recovery is delayed or when the business ends up overdrawing its accounts.

5. Data Volume and Accuracy Issues:

Inaccurate data entry or the lack of audit trails can lead to mistaken recoupment. Consequences may include legal disputes or even failure to recover the funds outlined in the recoupment. This risk is particularly high when no automated systems or real-time monitoring are in place.

Remember, clean data is prerequisite for effective reconciliation workflows.

6. Compliance and Fraud Risk:

Non-regulated recoupment practices, particularly when conducted on a large scale, can increase the risk of non-compliance with financial or legal standards.

They also create a greater exposure to fraud, and raise the chance of legal action from either customers or regulatory authorities. With the right reconciliation automation tools, not only can you ensure compliance, but also keep real-time visibility of active recoupments.

{{banner1.1}}

Best Practices for Managing Recoupment Situations

Multiple moving parts in the recoupment process can lead to complications, fast. To steer clear of them, the recoupment must be well-managed. Here are three best practices to keep in mind:

1. Implement Automated Reconciliation Tools:

Manual reconciliation often delays recoupment tracking, increases the risk of missed discrepancies, and makes recovery efforts inefficient and error-prone.

With the right automated reconciliation tool, tracking transactions, identifying discrepancies, and initiating recoupment activities can be handled in a single platform.

2. Maintain Open Communication:

It’s best if customers are notified clearly and in writing when a recoupment is created. Such documents, which differ in format, provide information about the basis, the total amount, and the legal grounds for initiating recoupment.

With streamlined communication measures in place, you can minimize conflicts and build customer relations. Simultaneously, complying with regulatory requirements is simplified.

3. Establish Internal Controls and Audit Trails:

Lastly, ensure that every transaction is logged with audit trails. These can be traced during internal auditing, and assist in legal defence in the rare case of escalations. Of course, this lengthy audit tracking process can be made simpler with an automated recoupment and reconciliation tool.

{{banner3.1}}

Automating Recoupment Tracking with Osfin

Tracking recoupment in large-scale financial systems requires the rapid, accurate, and complete tracking of large volumes of information. That is where Osfin comes in.

Osfin.ai is a state-of-the-art financial operations platform designed to automate the reconciliation process, particularly for recoupment. Osfin powers recoupment across cards, loans, and disbursements with over 30 million verifications in 15 minutes. Its suite of features includes much more, such as:

1. Seamless Integration & Format Flexibility

- Supports diverse formats including MT940, ISO 20022, CSV, JSON, XML

170+ ready connectors to ERPs, banking platforms, processors, and APIs

2. Comprehensive Transaction Reconciliation

- An automated engine matches transactions across ledgers, bank statements, ERPs, and clearing files

- Automatically reconciles gateway data, including fees, taxes, and settlements

3. Comprehensive Exception and Mismatch Handling

- Automatic mismatch flagging with escalation features

- Detects duplicates and outliers, with real-time exception tagging and smart team routing.

4.No-Code Workflows & Real-Time Dashboards

- No-code options for building custom rules, tolerances, and logic in your workflow

- Dashboards that track match status, exposure, and exception queues live

5. Enterprise-Grade Security & Compliance

- Security measures including role-based access, end-to-end encryption, and two-factor authentication

- Audit-ready process with full traceability

- Compliant with SOC 2, PCI DSS, ISO 27001, GDPR

6. Fast Setup & Expert Support

- Quick deployment, with minimal IT effort

- Backed and supported by reconciliation and finance operations specialists

Whether it's disputed transactions, regulatory holdbacks, or instant recoupment triggers, Osfin empowers you and your teams to handle all circumstances comfortably.

{{banner3}}

FAQ’s

1.What is recoupment in banking?

In banking, recoupment means the process of recovering money that was previously paid out, typically due to an error, overpayment, or missed mandatory payments. The bank follows through on recoupments by withholding or offsetting future payments.

2.When can a bank initiate recoupment?

A bank can initiate recoupment in several cases, including instances of overpayment, transaction processing errors, or the existence of funds that are contractually owed. This occurs within the scope of the original transaction or agreement. The bank must have a valid reason, supported by records or policy, to initiate recoupment.

3.Is recoupment the same as a refund?

No, recoupment is not the same as a refund. A refund occurs when the recipient voluntarily returns money, typically after a return or cancellation. Recoupment, however, is when the payer, often a bank, actively recovers money. This can be done by adjusting future payouts or claims.

4.Can customers dispute a recoupment?

Yes, customers can dispute a recoupment. If it is suspected to be incorrect, unfair, or not covered by terms of the agreement, customers can file complaints, and if needed, escalate the issue to regulatory bodies. They may question the reason for or the amount discussed in the recoupment.

5.What is the effect of recoupment on credit scores?

Recoupment can affect credit scores if it leads to missed payments, defaults, or collection actions. In other words, if it affects the customer's account operations, it may lower the customer’s credit score.