RTP vs ACH: Choosing the Right Payment Method

Real-time payments by the Clearing House have transformed the United States’ financial landscape by offering unmatched speed and availability. RTP by TCH handled over 76 million transactions worth $42 billion during Q1 2024 and 107 million transactions worth $481 billion by Q2 2025. This extensive adoption highlights the role of RTPs as an enabler of instant, secure and transparent transactions across the US.

Whereas, the ACH network serves as the backbone US electronic payments. Despite its regional focus, ACH is evolving by handling an increasing volume of transactions as businesses and consumers switch from traditional methods of money transfer toward electronic payments. This expansion of ACH real time payments and innovations like Same Day ACH further support this shift.

This article shares a detailed comparison of RTP vs ACH and explores their individual features, use cases, reconciliation differences and how Osfin supports their integration and reporting between these payment methods.

What this blog covers:

- What RTP (Real-Time Payments) is and how it works

- What ACH (Automated Clearing House) is and how it works

- Key differences between RTP and ACH: speed, availability, reversibility, cost, etc.

- Use cases where RTP is preferred vs where ACH is ideal

- Challenges and limitations of RTP and ACH rails

- How Osfin supports reconciliation across both RTP and ACH

- Best practices for choosing or combining payment rails

- Frequently asked questions on RTP vs ACH

What Is ACH?

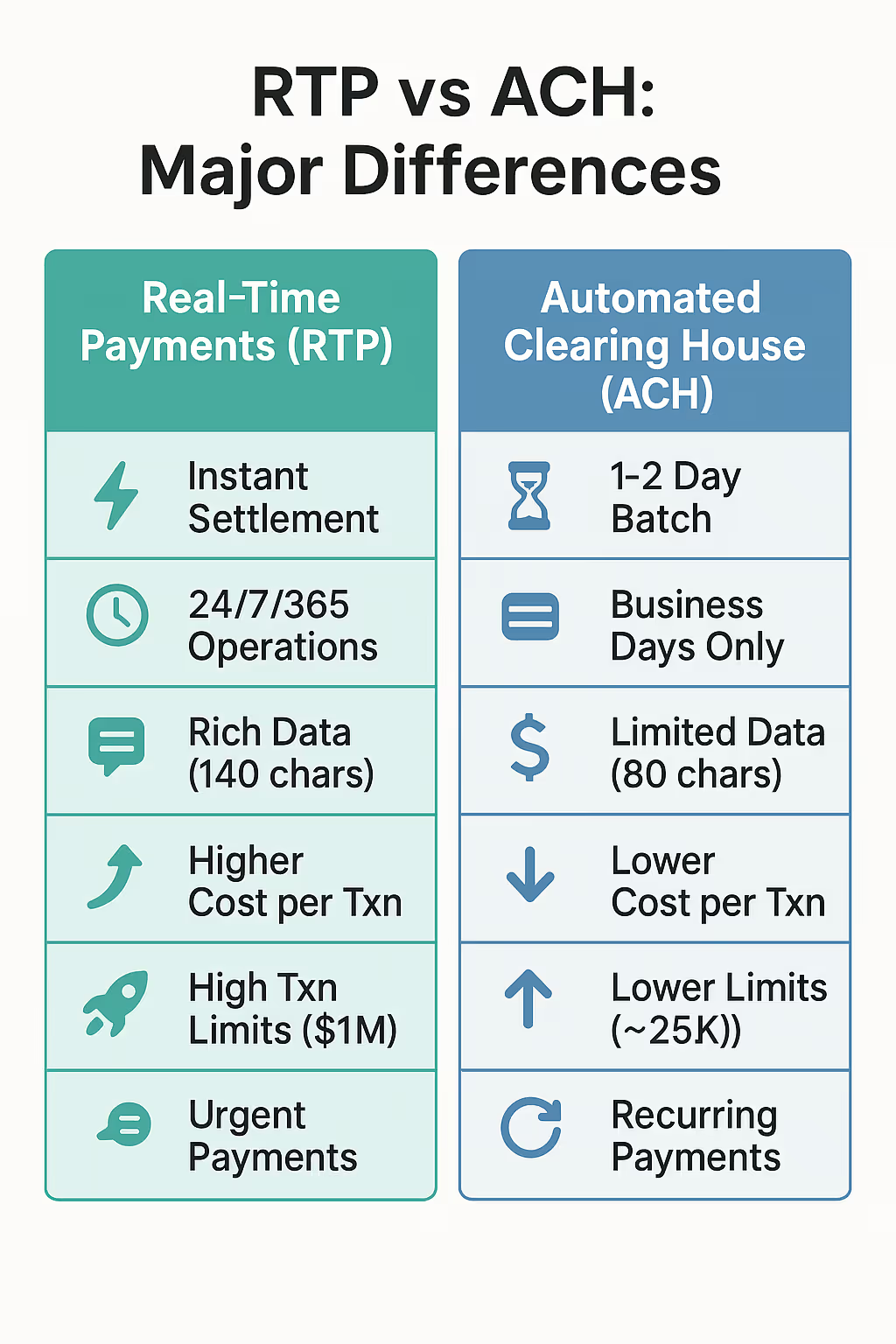

Despite the rise of instant transfers, the Automated Clearing House (ACH) remains the primary electronic payment method in the United States. As stated by NACHA, ACH payments moved over $22 trillion in Q1 2025 alone. ACH processes high volumes of recurring transactions such as payrolls, vendor invoices and government benefits with proven security and low per-payment costs. Traditionally, settlement occurs in one to two business days, but innovations such as same Day ACH and ACH real time payments are bridging that gap.

In the RTP vs ACH discussion, ACH offers cost efficiency and reliability while RTP prioritizes immediacy. Understanding what is ACH real time and the operational meaning behind faster ACH settlement is essential for finance teams designing cash flow strategies and reconciliation workflows that Osfin can fully automate.

What Are Real-Time Payments (RTP)?

Real-Time Payments (RTP) by the Clearing House enables nationwide instant fund transfers with settlement in seconds, operating 24/7/365. There are no cut‑off times, no batch delays and funds become available immediately which improves liquidity and cash flow visibility.

TCH RTP networks are built to process credit push payments in real-time while carrying rich payment information to ensure compliance with standards like ISO 20022. These systems process transactions in real time and often carry richer payment data than ACH to simplify and shorten the time taken by finance teams for reconciliation and reporting.

In the RTP vs ACH context, RTP delivers unmatched speed and transparency while ACH real time payments and Same Day ACH are better for legacy rails.

RTP vs ACH: Feature-by-Feature Comparison Table

The RTP vs ACH debate centers on speed, cost, availability, data richness, use cases and other factors such as those listed below.

When to Use RTP vs ACH

The table below talks about practical scenarios where organizations must evaluate RTP vs ACH based on their transaction urgency, cost considerations and operational impact among other important factors.

RTP vs Same Day ACH: Are They the Same?

Below are some similarities that matter to US finance leaders when it comes to comparing The Clearing House RTP vs Same Day ACH. Both of these were introduced to accelerate fund availability, enhance operational visibility and support more time‑sensitive payments.

1. Both are Faster than Standard ACH

Whether through continuous processing (RTP) or same‑day batch windows (Same Day ACH) both methods can clear funds faster than the standard ACH network. This speed helps in avoiding cash flow delays and improves working capital agility.

2. Compliance‑Grade Security and Governance

Both operate on regulated US banking networks with strict compliance frameworks including authentication protocols, fraud controls and data protection aligned to NACHA and payment‑network standards.

3. Support for Common Enterprise Use Cases

Each rail can facilitate payroll, vendor settlements, insurance payouts and consumer disbursements where faster settlement delivers measurable business benefits. Both integrate into core payment flows without requiring an entirely new ecosystem.

4. Integration with Financial Systems for Automation

Banks, ERPs and reconciliation platforms support both methods thus, transaction and settlement data is directly entered into finance systems for automated matching, reporting and audit trails.

5. Improvement in Liquidity Planning

By reducing the time taken for the transfer, both payment methods give treasury teams more timely and accurate data for forecasting and same‑day cash position management.

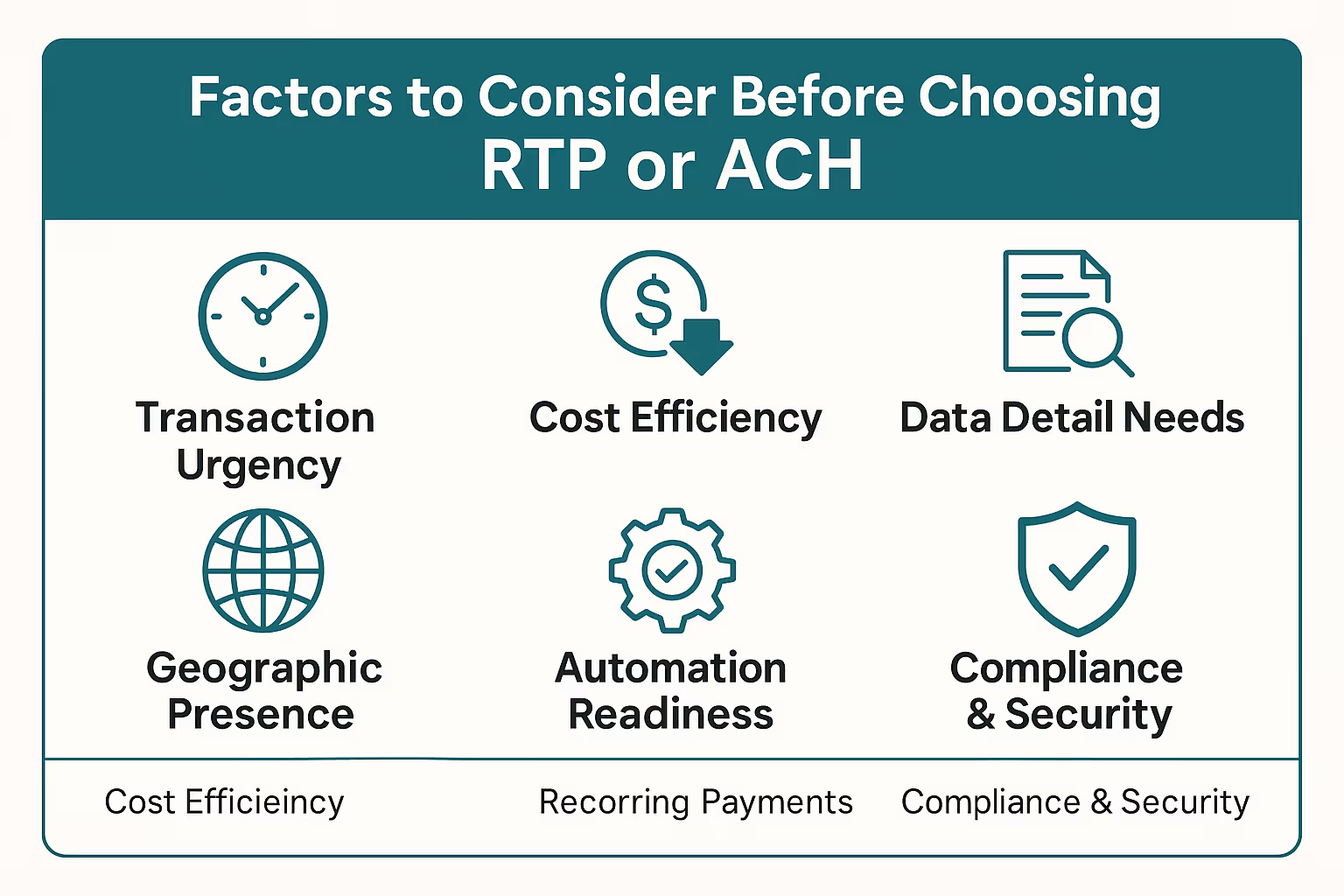

RTP or ACH: What’s Best for You?

Selecting between RTP vs ACH requires fintechs and finance leaders to evaluate multiple strategic factors such as those mentioned below so they can align payment operations with business goals.

1. Transaction Urgency and Speed Requirements

Evaluate if immediate funds availability is crucial for your business. RTP delivers instant settlement 24/7/365 which is ideal for emergency payouts, real-time payroll and just-in-time vendor payments. ACH and Same Day ACH suit those use cases where a one-day or two-day settlement is acceptable.

2. Cost Efficiency and Transaction Volume

Consider transaction fees relative to payment volume and value. ACH offers lower per-transaction costs making it more optimal for high volumes of routine payments. RTP charges a higher amount of fees but at the same time it offers speed and rich data for urgent or high-value transactions.

3. Data Richness and Reconciliation Needs

Real time ACH payments can include higher remittance data to support faster, more precise reconciliation and reporting. For finance teams focused on reducing manual intervention and errors, this transparency is an advantage.

4. Geographic Reach and Use Case Suitability

The Clearing House RTP operates across the US to enable faster credit transactions. ACH however, offers an infrastructure that is more suited for payroll, government disbursements and subscription billing.

5. Integration and Automation Capability

Evaluate how payment data integrates into ERP, treasury and reconciliation systems. Both RTP and ACH channels can integrate into automated workflows. Platforms like Osfin offer customizable and scalable automation to handle both types of payments.

6. Regulatory Compliance and Security

Both payment methods are made to comply with strict US-centric and international standards and industry-wise regulations. Ensuring your chosen system meets these criteria protects against fraud, data breaches and operational risks.

RTP vs ACH: Reconciliation and Reporting Differences

Reconciliation and reporting are crucial processes for finance teams that are responsible for managing cash flow and compliance. The table below points out the differences between real-time payments vs ACH, that affect transaction visibility and reconciliation preparedness.

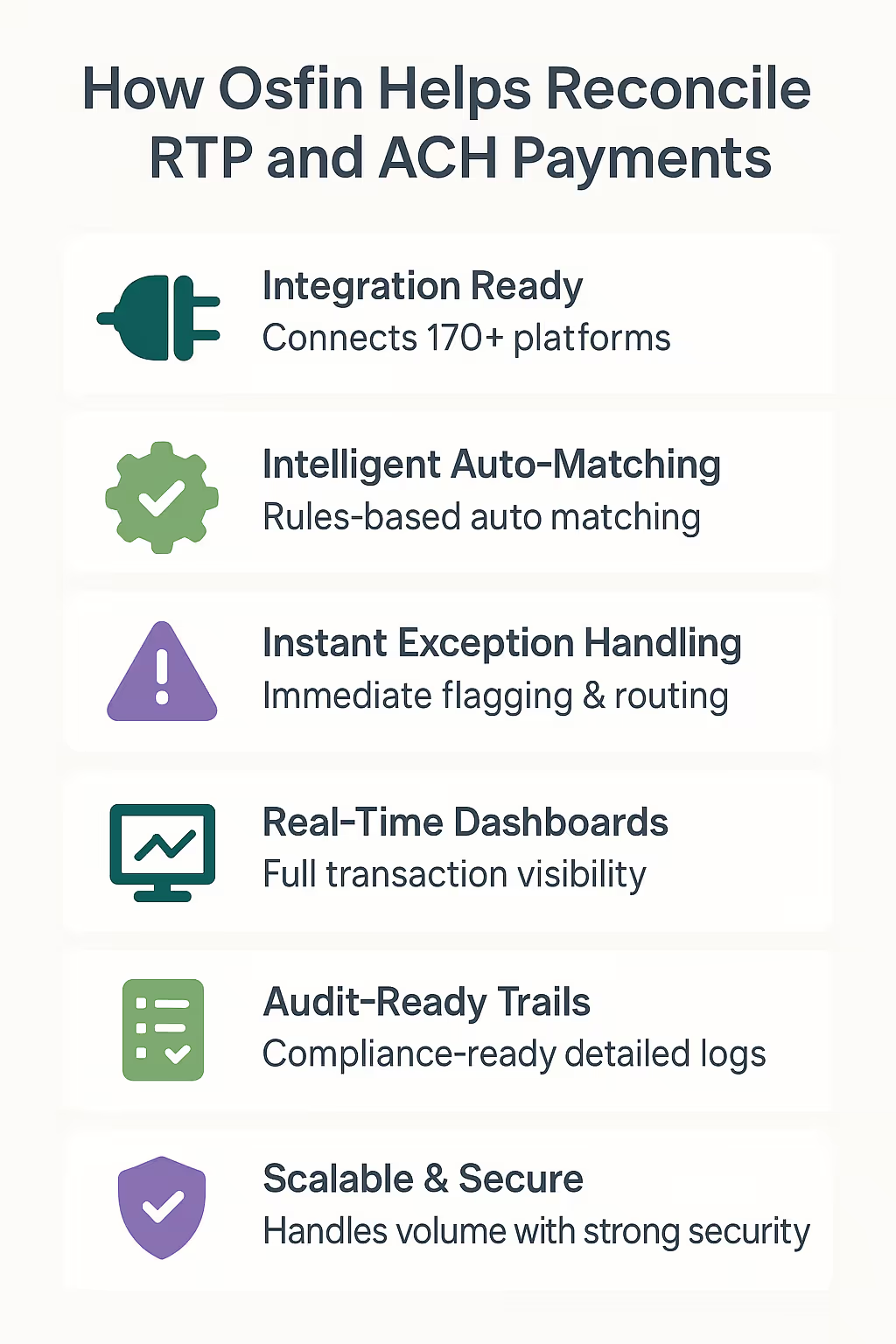

How Osfin Helps Reconcile RTP and ACH Payments

Reconciliation is one of the most important components when it comes to managing RTP vs ACH payment workflows where speed, accuracy and audit readiness are non-negotiable. Osfin transforms reconciliation by automating complex processes such as transaction matching and exception resolution across real-time and batch payments.

1. Configuration and Seamless Integration

Osfin integrates with over 170 platforms including banks, ERPs and payment service providers. The file-format agnostic platform can ingest data regardless of file formats to support business-specific models. It also automatically parses and cleans the data to prepare it for further reconciliation steps. This enables finance teams to combine ACH real time payments, real-time ACH and TCH RTP data streams under one platform without manual oversight.

2. Automated and Intelligent Reconciliation

The platform auto-reconciles 30 million transactions within 15 minutes using rules that you can configure to handle one-to-many and many-to-one scenarios. Osfin’s reconciliation also includes complex cases such as split payments and delays while maintaining 100% accuracy.

3. Exception Handling and Break Management

Osfin instantly detects exceptions and mismatched data, tags it with appropriate reasons and directs it towards appropriate teams with the ticketing and exception handling module. While doing so, Osfin also includes full contextual details such as transaction ID, payment rail, exception type and suggested resolution. This reduces the number of reworks and boosts reconciliation for both TCH RTP and ACH payments.

4. Real-Time Dashboards and Audit Trails

Finance teams can easily monitor and track reconciliation status through customizable dashboards as every transaction is fully traceable with audit-ready trails. Osfin also ensures compliance with standards like SOC 2, PCI DSS, ISO 27001 and GDPR to support regulatory and internal controls across ACH real time payments and RTP channels.

5. Built for Volume, Compliance and Security

Osfin’s platform delivers reconciliation that is scalable without having to expand the team size. It employs financial-grade security protocols and meets global compliance requirements which enables organizations to manage high-velocity payment volumes from both RTP and ACH.

Thus, Osfin automates the reconciliation processes for both instant and batch payments to ensure that finance teams can focus on cash flow strategy and decision-making without manual errors or delays. This operational clarity is essential for fintechs in the evolving RTP vs ACH payments landscape.

{{banner1}}

FAQs on RTP vs ACH

1. What security measures differentiate real-time payments (RTP) from traditional ACH transactions?

RTP employs advanced authentication, encryption and continuous settlement for instant fund transfers 24/7/365. ACH follows strict NACHA compliance with fraud prevention but relies on batch processing with different risk profiles and control timing.

2. How do reconciliation requirements vary between RTP and ACH payments?

RTP offers richer remittance data and immediate visibility to enable near-instant matching and faster error resolution. ACH primarily relies on batch data with limited details which causes delayed reconciliation. However, ACH real time payments and Same Day ACH reduce these timelines.

3. What operational challenges do finance teams face when integrating RTP alongside ACH payments?

Finance teams must handle both instant RTP and batch ACH workflows to ensure exception management and compliance. Platforms like Osfin unify these streams to reduce errors, improve audit readiness and support scalable payment operations.

4. How is Same Day ACH positioned within the broader RTP vs ACH landscape?

Same Day ACH accelerates ACH settlement via limited same-day windows that improve liquidity without RTP’s instant availability. It narrows the speed gap while sharing ACH’s infrastructure to help organizations needing faster payments without fully adopting RTP.