Understanding ACH Transfer Limits: Daily & Monthly Caps

When it comes to transferring money for bill payments, payroll deposits, tax refunds, or other recurring transactions, ACH transfers completely dominate the scene. With over 33.6 billion payments processed in 2024 alone, it’s clear they’ve become the backbone of modern payment systems in the US.

But behind the speed and convenience of ACH transfers lies an often-overlooked constraint: ACH transfer limits. These limits, determined by specific financial institutions, can dictate how much money can be sent or received in a single transaction, per day, or even per month, making them a critical factor for cash flow management and financial planning.

In this article, we’ll explore what ACH transfers are, ACH transaction limits, and various other nuances associated with them.

What this blog covers:

- What ACH transfer limits are and why they matter for businesses and individuals

- How daily, monthly, and per‐transaction caps are set and vary by institution

- The impact of ACH limits on cash flow, payment strategy and reconciliation

- Best practices for managing and negotiating ACH limits

What is an ACH Transfer?

ACH transfer is an electronic fund transfer (EFT) between banks and credit unions in the US. These transfers are mainly processed through a centralized financial network called Automated Clearing House (ACH), owned and governed by Nacha – an association of banks, payment processing companies, and credit unions. Read More

Typically used for payments like recurring bill payments, payroll, tax refunds, social security payments, or interest payments, ACH offers a convenient, secure, and cost-effective alternative to credit cards or check payments. For processing ACH payments, several entities are involved, including Originating Depository Financial Institution (ODFI), Receiving Depository Financial Institution (RDFI), and ACH Operator.

The processing begins when ODFI collects all the ACH transfer requests received within a given period into a batch and sends them to an ACH operator at different intervals during the day. The ACH operator sends these files to the RDFI, from which the funds will be withdrawn. The RDFI releases the funds, which travel through the ACH network to be deposited into the receiver’s account.

The standard processing usually takes 3-5 business days, but with the introduction of Same-day ACH, the processing time has been reduced to just a few hours.

What is an ACH Transfer Limit?

ACH transfer limit refers to the maximum amount of funds that can be processed through an ACH transaction, within a single transaction or over a specific period. This ACH limit is typically different for different financial institutions and may depend on the type of account, the customer's profile, and the ACH service used.

The objective behind setting these ACH payment limits is to ensure regulatory compliance, reduce risks, and prevent fraud in the payment process.

Every bank or credit union sets its individual ACH transfer limit, depending on its internal policies and risk management practices. For instance, Chase ACH transfer limit can be $10,000 per transaction, while Bank of America allows only $1,000 per transaction.

Nacha has also set some guidelines in this context. In case of Same-Day ACH, Nacha only allows ACH payments of up to $1 million per transaction.

Examples of ACH Transfer Limits by Bank

Since different financial institutions have different ACH payment limits, to get an idea about these transfer limits, let’s look at some of the real-life examples. Here are the ACH limits allowed by some of the major banks in the US:

{{banner1}}

Types of ACH Transfers

ACH transfers are broadly categorized into two types based on the method through which funds are processed. These include:

1. ACH Debits

ACH debits refer to the ACH transfers that are initiated by the payee to collect payment from the payer's bank account. These are pull payments, where funds are electronically pulled from a bank account after authorization is received from the sender. Some common examples include bill payments, subscription-based payments, B2B payments, and other similar transactions.

2. ACH Credits

ACH credit payments, on the contrary, are initiated by the payer to send funds directly into a receiving account. In this type of ACH transfer, the push mechanism is involved, where funds are sent or pushed electronically into a bank account. ACH credits are typically used for payroll deposits, tax refunds, and government benefits payments etc.

How ACH Limits Affect Finance Operations?

Since several business organizations rely heavily on ACH payments for payroll, vendor payments, bill payments, and other bulk transactions, ACH transaction limits can significantly influence cash flow, risk mitigation, financial planning, and operational efficiency. Here are the key impacts of ACH limits on finance operations:

1. Cash Flow Management

ACH limits can impact the timing and scheduling of payments. Businesses with large payment commitments may need to split payments across multiple transactions or days to stay within limits, which can complicate cash flow planning and delay settlements.

2. Operational Complexity

Finance teams may face increased administrative overhead to monitor and manage payment limits, requiring careful scheduling of payments and prioritization of transactions. Handling large payments might also require alternative methods, such as wire transfers, which can be more expensive and slower compared to ACH transfers.

3. Risk Management and Compliance

ACH payment limits act as controls to prevent fraud, reduce over-exposure to financial loss, and ensure system stability for both financial institutions and users. Banks must ensure that payments remain within regulatory and internal risk thresholds to avoid declines or returns.

4. Impact on Payment Speed and Customer Experience

Restrictions on same-day ACH payments or lower daily caps can lead to delays in urgent payments or payroll, affecting recipient satisfaction. Businesses need to plan around cutoff times and limits to ensure timely payments.

5. Financial Planning and Forecasting

Understanding ACH limits helps in the optimization of working capital by aligning payment schedules with allowable transfer limits. Limits can influence decisions on payment methods and require contingency planning for larger or time-sensitive payments.

Best Practices for Managing ACH Transfer Limits

To effectively navigate the ACH transfer limits set by different financial institutions, certain proactive strategies are required that balance compliance with operational efficiency. These include:

- Know the transfer limits: Get clarity on your daily, per-transaction, and monthly ACH caps, and understand how they differ for various transaction types.

- Split large payments when necessary: If an urgent payment exceeds your available limit, plan ahead to divide it into smaller installments that fit within the allowed caps.

- Negotiate higher limits: If your transaction volumes are growing, work with your bank to increase limits in advance.

- Leverage security and fraud detection tools: Integrate fraud monitoring, dual authorization for high-value transactions, and robust cybersecurity protocols to support higher limits safely.

- Regularly review your limits: Financial institutions periodically review ACH limits based on updated risk models, account activity, and customer profiles. Demonstrate responsible account use to be eligible for increased limits, and keep your business or customer information up to date.

{{banner3}}

Pros and Cons of ACH Transfers

While ACH transfers have become critical for modern business payments in the US, powering everything from payroll to vendor disbursements, they aren’t without their trade-offs. Like any payment method, they offer distinct advantages but also come with limitations that can impact timing, costs, and flexibility.

Pros of ACH Transfers

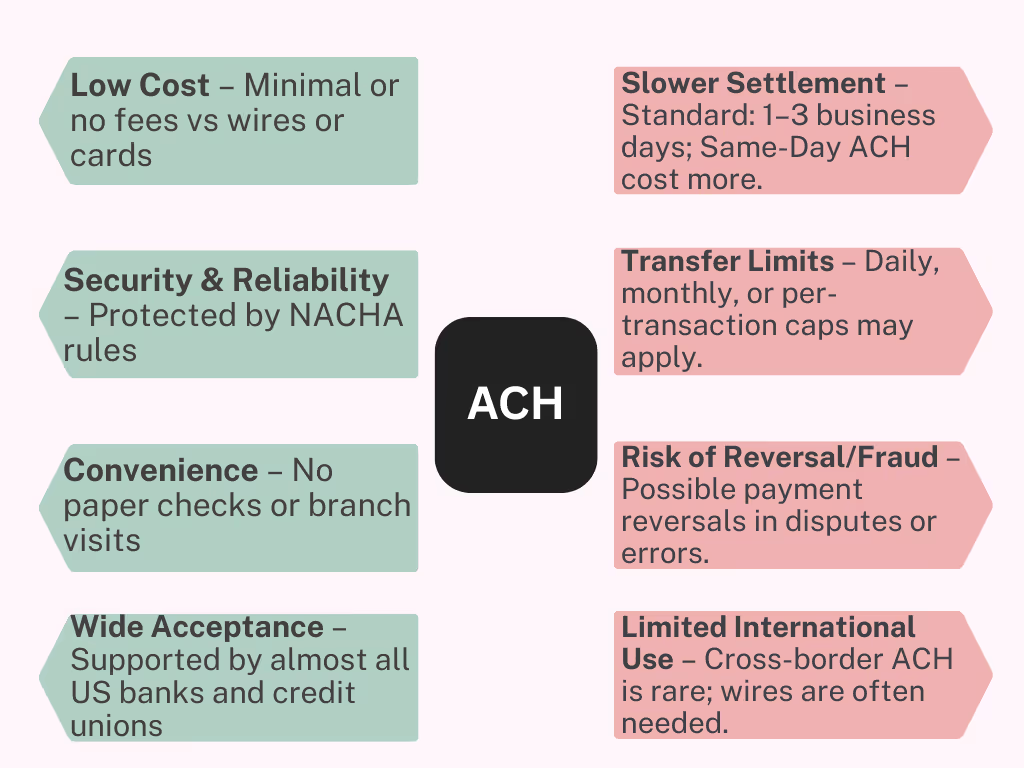

Low Cost: ACH transfers usually require minimal or no fees compared to wire transfers or credit card transactions, making them an affordable option for bulk or recurring payments.

Security & Reliability: ACH transactions use robust bank-to-bank systems, operating under strict NACHA rules, which reduce fraud risk and ensure regulatory compliance.

Convenience: Since the payments are processed electronically, there’s no requirement for paper checks, in-person bank visits, or manual workflows. Businesses and consumers both benefit from easy online initiation.

Wide Acceptance: Almost all US banks and credit unions support ACH, allowing broad reach for everything from payroll to insurance payments.

Cons of ACH Transfers

Slower Settlement Times: Standard ACH payments typically take 1-3 business days to settle; Same Day ACH is faster but may have availability constraints and higher fees.

Transfer Limits: Most banks impose per-transaction, monthly, or daily ACH limits that may restrict high-value payments.

Risk of Payment Reversal or Fraud: Unlike wires, ACH payments can sometimes be reversed if authorized incorrectly or in cases of disputes. Fraud risks exist if proper account validation is not used. Read More

Not Suitable for International Payments: While limited international ACH is possible, most cross-border payments require wire transfers or specialized remittance services.

Optimizing ACH Reconciliation with Osfin

ACH payments provide an efficient and secure way to transfer funds, but reconciling them, especially at scale, can be a tedious, error-prone process. Mismatched entries, return codes, and multiple bank files often create bottlenecks that slow down operations teams. Osfin’s reconciliation automation platform removes these roadblocks and streamlines ACH reconciliation from start to finish. Let’s see how.

1. Seamless Data Intake from Any Source

As a truly format-agnostic platform, Osfin connects with 170+ data sources, including banking systems, ERPs, CRMs, ACH operator, and payment gateways to bring in data. No matter the file type, whether it’s NACHA/ACH files, BAI2, ISO 20022 XML, CSV, Excel, or flat files, Osfin ensures smooth ingestion and reconciliation.

During intake, it applies configurable tolerance thresholds to weed out incomplete or inaccurate records before they ever hit reconciliation. Duplicate entries and statistical outliers are identified instantly, ensuring only clean, usable data moves forward.

2. High-Volume, Intelligent Matching

Using advanced, rules-based matching logic, Osfin effortlessly handles complex transaction relationships, whether they’re many-to-one, one-to-many, or nested. The system can reconcile up to 30 million records in just 15 minutes with 100% accuracy.

3. Proactive Exception Resolution

When a transaction doesn’t match, Osfin assigns a precise reason code and automatically routes it to the right team member for quick resolution. Live dashboards provide at-a-glance visibility into match rates, outstanding exposures, and exception queues so teams can act quickly and decisively.

4. Audit-Ready, Secure Outputs

Every reconciliation cycle ends with a detailed compliance report and a fully traceable workflow history. All data is safeguarded with enterprise-grade 256-bit encryption, role-based permissions, and multi-factor authentication. The platform adheres to stringent regulatory frameworks, including SOC 2, PCI DSS, ISO 27001, and GDPR, ensuring both operational efficiency and complete compliance peace of mind.

With Osfin’s powerful automation, intelligent matching, and airtight security, transform your ACH reconciliation from a manual, error-prone chore into a fast, precise, and fully compliant process. Book a demo now.

FAQs on ACH Transfer Limits

1. Is there a limit on ACH payments?

Yes, there is a limit on ACH transfers. Each financial institution sets its own caps on ACH transactions based on factors like account type, transfer method, and customer profile. There can be a monthly and daily ACH limit, and even on a per-transaction basis.

2. What happens if I try to exceed my ACH transfer limit?

If one tries to send more than what the ACH limit allows, the bank may block or reject the transfer. Some will alert right away, while others simply decline the transaction. It is always better to check the ACH limit before making large payments to prevent delays.

3. What is the maximum ACH transfer limit that can be transferred between banks?

The ACH maximum amount that can be transferred between banks depends on factors like the account balance, the bank’s ACH limits, and the receiving bank’s acceptance limits. While Nacha recently increased the maximum possible ACH transfer to $1,000,000, not all customers will qualify for that amount.

4. How do ACH limits affect business operations?

ACH limits can slow down important business transactions like payroll, vendor payments, and bulk transfers. Businesses might have to break payments into smaller amounts, change payment dates, or ask for higher limits to keep cash flow steady and prevent delays.

5. Is there a difference between ACH transfer limits for personal and business accounts?

Personal accounts usually have lower ACH transfer limits than business accounts, since businesses often handle larger payments. In many cases, business accounts can request higher limits based on their transaction volume and operational needs.