Internal Auditing: Definition, Process, and Examples

In an ever evolving financial and technical environment, institutions cannot just rely on accuracy. They also need risk resilience, regulatory compliance, and operational efficiency, which is where internal auditing plays a critical role.

Guided by the Institute of Internal Auditors (IIA), internal auditing is a process through which financial institutions achieve required objectives by evaluating the effectiveness of operations, risk management, internal controls, and institutional processes.

These audits are conducted by the internal staff or specialized professionals to provide unbiased information with the intention of improving business performance and ensuring regulatory compliance.

What Is Internal Auditing?

Internal auditing is an independent and methodical review of an organisation that is specifically performed to evaluate and improve the internal processes, operations, and controls of that organisation.

As internal auditing is intended to create a systematic approach to enhance the complete governance and risk management of an institution, it extends far beyond basic compliance checks, control documentation exercises, or spreadsheet-based walkthroughs. It is also tied to:

- Financial data reliability

- Operational efficiency and scope for scalability

- Reporting precision and accuracy

Internal auditing not only highlights what went wrong, but also how financial systems can prevent the recurrence of any errors.

Why Internal Auditing Matters in Enterprise Environments

In regulated industries like banking and fintech, internal auditing is instrumental to maintain regulatory compliance and strengthen risk management.

Institutions overseen by authorities such as the Reserve Bank of India and Securities and Exchange Commission must demonstrate operational transparency, control reliability, and accounting accuracy. Internal auditing supports this in enterprise environments through the following:

1. Regulatory scrutiny in banking, insurance, and fintech:

Regulatory scrutiny has intensified universally, as it focuses on compliance checks, data privacy, and prevention of control failures. Authorities are shifting to in-depth auditing from routine inspections for enhanced capital and liquidity management.

2. Financial statement assurance dependency:

Financial statement assurance provides an independent, third-party validation of an institution's financial statement to improve reliability. This is heavily dependent on internal auditing due to the underlying management control and effectiveness.

3. SOX and internal control obligations:

Sarbanes-Oxley Act (SOS) mandates strict internal control obligations that include management certification of banks, and annual assessments of internal control effectiveness for ensuring accuracy, preventing fraud, and protecting citizens and investors.

4. Board-level reporting of control failures:

Control failures must be reported with precision to the designated authorities, highlighting deficiencies, material weaknesses, and crisis management plans to enable risk oversight. Internal audits should also focus on root cause analytics to prevent recurrence.

5. Cybersecurity and payment risk oversight:

Effective cybersecurity and payment risk oversight is crucial to enterprise environments and requires multi-layered frameworks for the prevention of fraud and data breaches. This helps financial institutions shift from reactive to proactive strategies.

6. Scaling operational complexity:

Scaling internal auditing for operational complexity requires complementing a checklist-based approach with a risk-based approach that uses tools like automation, data analytics, and trained individuals to support business growth.

Internal Audit Process: Step-by-Step

Internal auditing works best when it follows a clear and structured process rather than a one-time inspection. At its core, the audit journey is about understanding how things actually function inside an organization, and whether they’re working the way they’re supposed to.

Most internal audit teams structure their work around a series of practical steps, guided by professional standards such as those from the IIA. They include:

Establishing the Audit Plan

The process begins with deciding what to audit and why. Auditors typically look at risk areas, recent business changes, previous issues, and regulatory compliance to identify where attention is most needed.

The aim is to focus on what could cause the biggest problems in case they go wrong. Many organizations link this planning stage to broader risk frameworks like COSO to ensure audits stay relevant to real-world business risks.

Scoping and Defining Objectives

Once an audit area is selected, the next step is getting specific. What exactly is being reviewed? What questions are we trying to answer? This is where auditors outline the boundaries of the review to ensure clear conclusions.

Fieldwork and Control Testing

This is the most active part of the audit. Auditors engage with teams, review documents, analyze data, and test whether controls are functioning as intended. For example, they might check whether approvals are happening properly or if system access is restricted where it should be. The goal is to understand whether routine operations are reliable.

Reporting and Communication

After gathering insights, auditors bring everything together into a report. But a good audit report isn’t just technical, it’s practical. It explains what was found, why it matters, and what can be improved.

Clear communication helps management make informed decisions rather than simply ticking compliance boxes.

Follow-Up and Continuous Monitoring

Finally, the real value of an audit lies in what happens next. Follow-ups ensure that agreed improvements are actually implemented. Increasingly, organizations are also adopting ongoing monitoring to oversee risks between audit cycles.

In the end, this structured approach turns internal auditing into a continuous learning tool, not just a periodic check.

{{banner1}}

Types of Internal Audit

As internal audits go far beyond traditional compliance checks and follow-ups, there are defined types of audits based on key factors like operations, finance, and technicality. Each of them is explained below:

Financial internal audit

Financial internal audits focus on reviewing the accuracy and integrity of the financial statements of an institution. It evaluates the accounting methods, policies, and financial controls to ensure that they are aligned with frameworks recommended by the Institute of Internal Auditors (IIA).

Additionally, decision-makers also require reliable and trustworthy financial data to safeguard their organisation.

Operational internal audit

Operational audits evaluate the efficiency of day-to-day business activities of an organisation, which not only highlights errors but also areas for improvement. Its main purpose is to enhance the effectiveness of business operations by identifying bottlenecks and resource wastage, while building a greater risk tolerance for the business.

Compliance audit

Compliance audits are meant to ensure adherence to external laws such as those influenced by the COSO (Committee of Sponsoring Organizations), internal policies, and company requirements. These are crucial in industries that are guided by standard frameworks.

IT and cybersecurity audit

IT and cybersecurity audits examine the data privacy controls, IT infrastructure, and other software controls of an organisation to ensure that they are resilient against any potential cyber threats.

They often borrow guidelines from ISACA (Information Systems Audit and Control Association) to align with universal standards.

Process audit

Process audits are conducted to understand if your company's processes are functioning as intended. They identify control gaps and inefficiencies in operational processes so that they can be improved with corrective action.

Fraud audit

Fraud audit is intended to investigate and prevent financial manipulation, which could take the form of asset misappropriation, financial statement discrepancies, or even corruption. Unlike regular audits, fraud audits focus on identifying unusual activities in an organisation to uncover fraud.

Common Internal Audit Risks & Failures

Well-planned audit systems can also fall apart if primary foundations are not in place. These are some gaps in audit systems that should be addressed to strengthen internal audits:

1. Lack of independence: Internal audits should not be influenced by any other external sources, including the organisation's own management. If there is no independence with respect to audit systems, credibility and objectivity could be compromised.

2. Inadequate audit documentation: Since documentation serves as the main evidence in audit systems, its inadequacy may lead to poor action plans. Without structured records, statements cannot be validated.

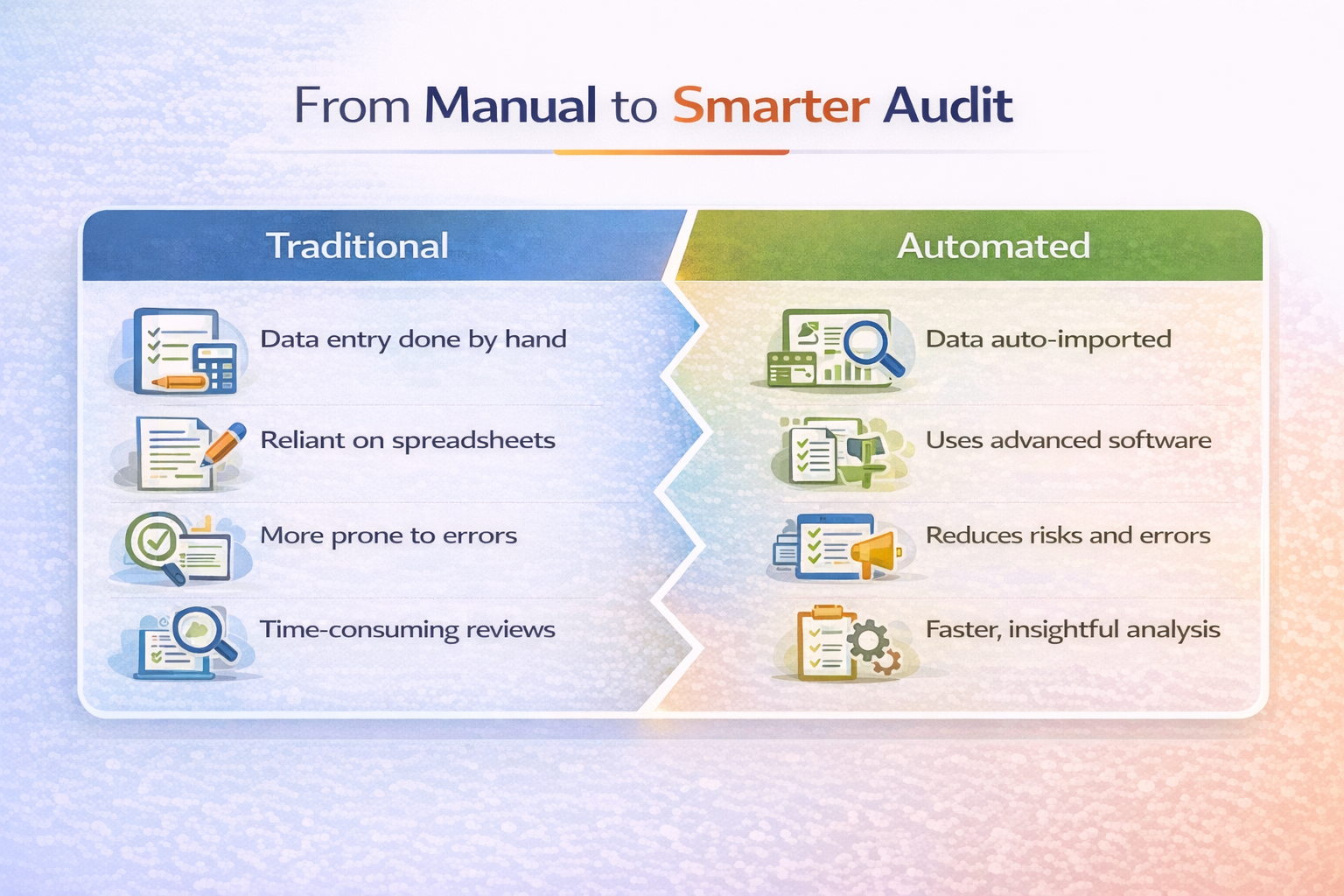

3. Overreliance on spreadsheets: This can create a huge gap in traceability as high dependence on spreadsheets, especially manual ones, is prone to errors and weak data governance. This over-reliance can mask serious issues until they escalate into major issues.

4. Poor reconciliation coverage: Poor reconciliation coverage could be a source of discrepancies between records and systems like IT, finance, and operations. Weak and manual reconciliation practices often result in errors that might go unnoticed at first but pose serious threats.

5. Delayed reporting: Timelines are crucial, especially in dynamic environments, which include finance and banking. Delays in reporting impact the relevance of audit insights, which allow issues to persist for a longer duration.

6. Inconsistent testing methodologies: If the testing methods are not consistent, there will be no benchmark for the required standards. Consistency is instrumental in ensuring that the necessary guidelines are followed.

7. Limited system visibility: This happens when auditors do not have access to complete data and documentation, which reduces audit depth and decreases the probability of flagging errors.

{{banner3.1}}

Improving Internal Audit Before Automation

Before introducing automation in internal audit systems, organisations must improve some foundational aspects of their routine activities because technology is not a replacement for methodologies, but an amplification of them.

Strengthening Governance Structure

Strengthening the governance structure is the first step towards creating a successful audit system as it helps organisations evolve into scalable and compliant enterprises from fragmented and unreliable frameworks.

Institutions such as IIA highlight universal guidelines that can be adopted for structural independence to reduce bias in assessments and increase the credibility of the organisation. Clear reporting timelines and escalation procedures ensure that the audit findings can be translated into measurable action.

Standardizing Audit Methodology

Standardizing audit methodology is also equally important because without consistent methods, internal audits will lose their relevance as they become fragmented across different divisions.

Aligning with specific industry requirements helps in establishing reliability and appropriate comparability in audit evaluations.

Control Documentation Standards

It is essential to strengthen the control documentation standards for achieving continuity and accountability. Strong documentation leads to better auditing, which enables better institutional learning and regulatory validation.

Flowcharts, narratives, and risk control matrices that can define conclusions for every assessment ensure a clear trail of findings, enhancing overall compliance.

Role of Technology & Automation in Internal Auditing

Once the basic foundations for internal auditing are set in place, technology becomes a catalyst for institutional growth by improving the speed, depth, and overall accuracy of auditing. Here are some instrumental features that highlight the role of automation:

Automated Data Aggregation

In conventional auditing methods, auditors collected data manually from different departments, which often led to unorganised data and disparate findings.

Automation integrates all these sources into a unified view, completely eliminating the need for manual handling and improving accuracy to a great extent.

These systems automatically gather data from spreadsheets and banking systems to form consolidated reports, which help in enhancing compliance with industry standards. This also leads to early identification of potential risk and manipulation, making the financial institution audit-ready throughout the year.

Continuous Transaction Monitoring

Automation is the real-time analysis of financial activities that helps you shift from periodic reviews to ongoing monitoring, which helps in detecting deviations early and taking the required corrective action before issues escalate.

This proactive model is best suited for modern financial organisations as it only relies on previous static rules, but uses strategic tools to reduce false positives by providing constant surveillance.

Structured Issue Tracking

Structured issue tracking involves a systematic and organised process of resolving tasks with ownership mapping, remediation timelines, and tracking data for timely action.

Some instrumental components of an automated structured system include unique identifiers, prioritisation by category, and ownership.

Automation brings transparency into this process by simplifying reviews in complex financial and technical environments and transforming audit findings into measurable improvements.

Enterprise-Grade Audit Trails

Enterprise-grade audit trails are secure and traceable logs of finances, system changes, and routine activities. These trails ensure transparency in systems, which is critical for regulatory compliance, detection of fraud, and accurate financial reviews.

Features of enterprise-grade audit trails include security, comprehensive coverage, and actionable insights, which lead to continuous financial and operational improvement.

Measuring Internal Audit Effectiveness

Measuring internal audit effectiveness is not determined by the completion and conclusions of an audit, but also by how it impacts risk management, governance, and control environments. The following factors play a huge role in assessing the audit effectiveness:

Audit Coverage Ratio

The audit coverage ratio measures the extent of an institution’s operations that are reviewed by internal and external audit.

It is designed to understand whether the internal audit system is aligned with the evolving risk management landscape. A higher ratio indicates risk-focused planning, at par with enterprise risk approaches.

Issue Resolution Timeliness

This defines how promptly the flagged issues can be resolved by the management. As automation accelerates identification, it has a direct impact on responsiveness. Automation helps in avoiding delayed resolutions, which could signal a lack of accountability.

Repeat Finding Frequency

Recurring issues from previous internal audits signal deep-rooted problems that require systemic solutions, such as shifting from annual to quarterly reviews to identify root causes for long-term growth.

Control Testing Automation Rate

As testing becomes modernized and digital, the proportion of controls tested automatically also becomes an indicator of institutional efficiency. If the automation rate is higher, it eliminates the need for manual testing and saves operational time.

Audit Committee Reporting Quality

Finally, measurable action depends upon the quality of insights that reach the management. Better quality reporting translates findings into business growth and sustainable improvement.

How Enterprise Reconciliation Platforms Like Osfin Strengthen Internal Auditing

As internal auditing shifts toward continuous improvement, reconciliation can no longer remain manual and fragmented. Osfin addresses this gap as an enterprise SaaS reconciliation automation platform built for high-volume, complex environments. It ingests data in its original format and is designed to provide cross-system control visibility, making it especially valuable for internal audit teams.

Osfin enhances reconciliation transparency, reduces manual journal adjustments, enables exception-level visibility, and maintains traceability that supports audit-ready documentation

Osfin’s capabilities are delivered through four key stages:

Importing Data (Ingestion):

Osfin is file-format agnostic, supported by 170+ integrations that import data from multiple sources regardless of format. It applies custom deviation tolerances to filter poor-quality data and detects deviations at the ingestion stage.

Reconciliation Process:

Using logic-based matching, Osfin handles one-to-many, many-to-one, and multi-way reconciliations (two- to five-way). It can reconcile up to 30 million records in 15 minutes and automatically match payment gateway reports with commission, tax, and fee breakdowns.

Exception Handling:

The platform flags unmatched transactions, assigns accurate reasons, and routes them via its ticketing engine. Live dashboards provide visibility into match status and exception queues.

Final Output:

Osfin generates compliance-ready reports with full traceability. It secures data using 256-bit encryption, maker-checker controls, role-based access, and two-factor authentication, while aligning with SOC 2, PCI DSS, ISO 27001, and GDPR.

In doing so, Osfin turns reconciliation into a transparent, audit-aligned control function.

{{banner3}}

FAQs

1. What is internal auditing?

Internal auditing is an independent activity designed to examine and improve an institution's operational efficiency. It includes a structured assessment of internal tools, processes and risk management.

2. What is the purpose of internal auditing?

The primary purpose of internal auditing is to provide an accurate and unbiased review of an organisation’s processes. They serve as an integral tool for improving financial administration and operational efficiency.

3. Who should perform an internal audit?

Internal audits should be performed by specialized professionals which are a part of the institution. They often hold certifications like certified internal auditor (CIA).

4. Who does an internal auditor report to?

The internal auditor generally reports to the board of directors through the audit committee. The chief internal auditor also reports directly to the CEO in many cases.

5. How often should internal audits be conducted?

Internal audit frequency is determined by risk, process complexity, and compliance requirements, generally ranging from quarterly for high-risk areas to annually for stable, low-risk processes.

6. What is included in an internal audit report?

An internal audit report typically includes an executive summary, audit objectives, scope, detailed findings (using the 5Cs: Criteria, Condition, Cause, Consequence, Corrective action), and agreed-upon management action plans.

7. Can automation improve internal auditing?

Yes, automation significantly improves internal audit by increasing efficiency, accuracy, and coverage while reducing costs and eliminating manual handling.