Payment Processor vs Payment Gateway: Choosing the Right Solution

From card swipe to UPI, mobile wallets, BNPL, QR codes, and even cryptocurrency, customers now have more than 200 digital payment choices at their disposal. For them, it's just a tap or a click. But for financial institutions and banks, it adds another layer of integration, compliance, and security to tackle.

It's the payment gateway and payment processor behind the scenes that facilitate these transactions. Knowing how these two function together is essential for delivering compliant, seamless, and secure digital payment experiences.

In this blog, we’ll explore what is a payment gateway vs payment processor, their respective roles, and why both are indispensable for modern banking.

What this blog covers:

- What a payment processor is and how it works

- What a payment gateway is and its role in transactions

- Key differences between a processor and a gateway

- How gateways and processors work together in payment flows

- Examples and use cases for each

- How Osfin supports reconciliation across payment processors & payment gateways

What Is a Payment Gateway?

A payment gateway is a technology service used to securely pass payment information from the customer to the acquiring bank (the merchant's bank) and to report back to the customer or merchant whether the transaction has been approved or declined.

Think of it as the virtual equivalent of a Point-of-Sale (POS) terminal in a physical store, with added security.

How It Works (Step by Step)

1. Customer makes payment

- On an online website or application, the customer selects a product and proceeds to checkout.

- They enter payment information (card number, UPI ID, wallet log in, etc.).

2. Encryption and security verification

- The payment gateway encrypts this sensitive information so that it isn’t stolen while being transferred.

- Technologies such as SSL (Secure Socket Layer) and PCI DSS compliance are employed.

3. Data is routed to the processor.

- The gateway sends the information to a payment processor or the acquiring bank directly.

- The processor then communicates with the card network (Visa, Mastercard, etc.) and then the customer's issuing bank.

4. Bank authorization

The issuing bank verifies:

- Are the card credentials valid?

- Is there sufficient balance or credit?

- Any fraud warnings?

Depending on this, the bank approves or rejects the transaction.

5. Response back to the merchant

- The payment gateway gets the reply from the bank and passes it back to the website/app.

- The merchant verifies the order if approved.

6. Settlement

The funds are sent to the merchant's account (after deducting processing charges) and are deducted from the customer's bank account upon approval.

Key Features of a Payment Gateway

Here are some of the significant features of a payment gateway:

- Safeguards card and bank information against fraud.

- Multiple payment modes including cards, UPI, wallets, net banking, BNPL (buy now pay later).

- Fraud detection mechanism that prevents suspicious transactions.

- Smooth user experience facilitating rapid payments without fuss.

- Global accessibility, supporting various currencies and international transactions.

{{banner3}}

What Is a Payment Processor?

A payment processor is the mechanism that actually transfers money from the customer's bank (the issuing bank) to the merchant's bank (the acquiring bank). The processor takes responsibility for forwarding the transaction through the correct banking networks (Visa/Mastercard), verifying that funds are available, and confirming whether the payment is accepted or rejected.

How It Works (Step by Step)

1. Customer makes a payment.

After the payment gateway captures details, the payment processor steps in.

2. Authorization request

The processor sends payment details via the card networks (Visa, Mastercard) to the issuing bank (the customer's bank).

3. Bank checks funds

The issuing bank verifies if:

- Card details are authentic

- There are available funds

- There is no fraud detected

4. Approval or decline

The issuing bank sends an approval/decline message back through the processor.

5. Transaction settlement

Upon approval, the processor guarantees that the money is debited from the customer's account and credited (after deducting charges) to the merchant's account.

Key Features of a Payment Processor

The payment processor makes sure transactions are completed smoothly with these important features:

- Handles authorization, checking if the bank approves/declines properly.

- Transfers funds from customer to merchant banks.

- If the card network accepts it, it works with card networks like Visa, Mastercard, etc.

- Makes sure merchants receive settlement after deductions.

- Supports refunds and chargebacks in case customers dispute payments.

{{banner3.1}}

Key Differences: Payment Processor vs Payment Gateway

While both are part of the same ecosystem, the difference between payment processor and gateway lies in their respective roles.

Here are the key payment gateway vs processor differences:

Benefits of Payment Gateways and Processors

While merchants view gateways and processors as tools for sales, banks and financial institutions consider them critical infrastructure for secure, scalable, and compliant payment ecosystems.

Both payment gateway vs payment processor brings their own advantages:

Advantages of Payment Gateways

1. Increased Customer Confidence:

Encryption, tokenization, and fraud detection secure sensitive card and bank information, enhancing customer confidence in payment products.

2. Increased Payment Acceptance:

Gateways enable banks to accept various payment instruments, including credit/debit cards, ACH, Buy Now, Pay Later (BNPL), and digital wallets, making the bank a one-stop shop for payments.

3. Global Reach:

Multi-currency and cross-border capabilities open up more possibilities with international merchant services.

4. Value-Added Insights:

Transaction data from gateways can be used to derive analytics, customer behavior insights, and customized product design.

5. Operational Efficiency:

Plug-and-play integrations with e-commerce platforms minimize onboarding friction for bank-acquired merchants.

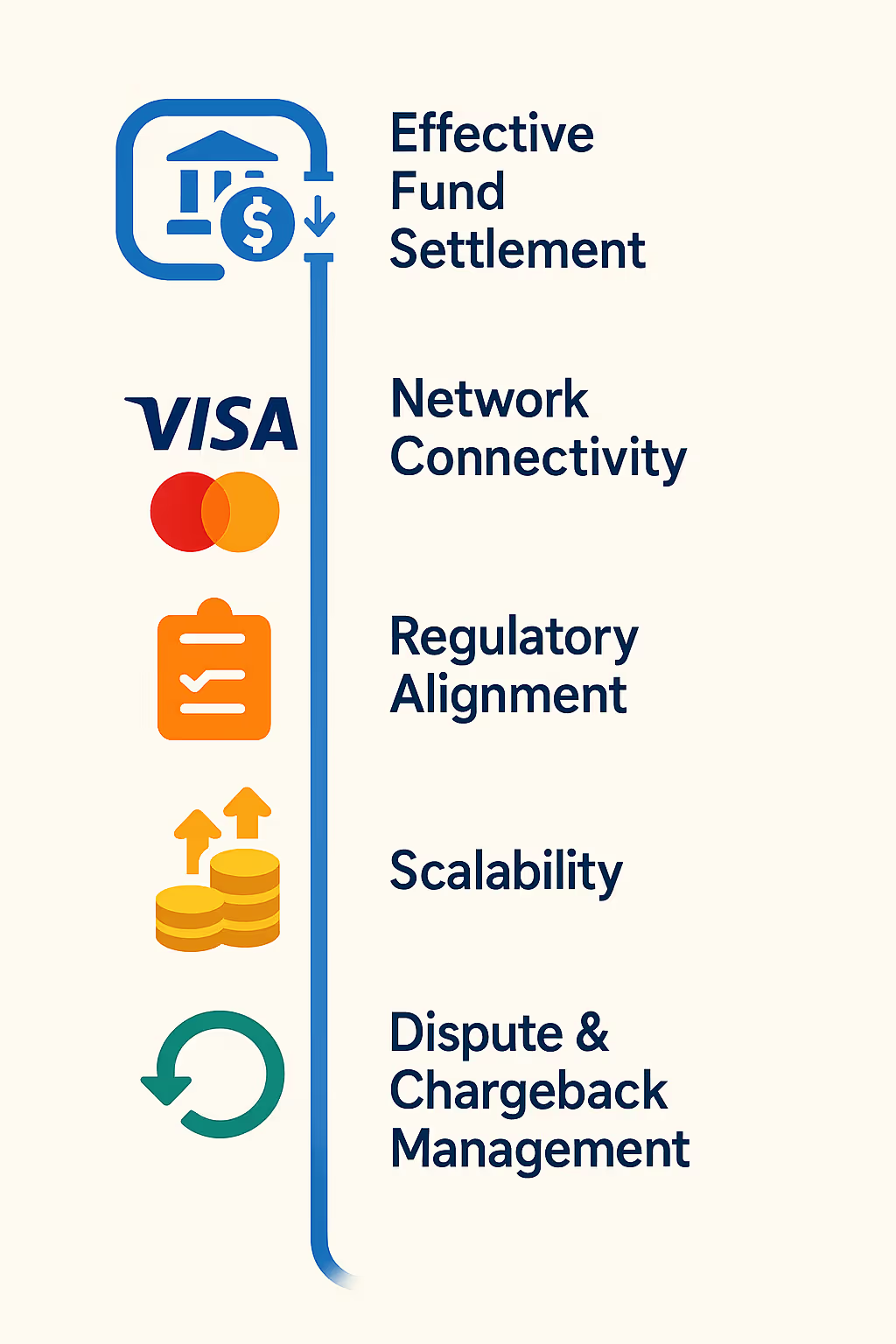

Advantages of Payment Processors

1. Effective Fund Settlement:

Prompt fund transfers between the receiver and sender banks promote liquidity and enhance trust.

2. Network Connectivity:

Direct connections with Visa, Mastercard, American Express, and Discover enhance authorization speed and reliability.

3. Regulatory Alignment:

Alignment with PCI DSS, NACHA (for ACH), and FFIEC reduces regulatory and operational risks.

4. Scalability Under High Volume:

Processors handle hundreds of millions of transactions, enabling banks to maintain uninterrupted service to merchants during busy seasons.

5. Dispute and Chargeback Management:

Workflow structures for refunds, reversals, and chargebacks increase customer satisfaction and allow banks to meet U.S. regulatory reporting requirements.

This balance makes payment processing vs payment gateway a complementary system rather than an either/or choice.

Why Businesses Need Both

Some businesses rely on just a payment processor or a payment gateway. The truth is: we need both.

Here’s why:

1. Gateways provide the entry point

A payment gateway acts like the digital security at the front door of a store. It's where the consumer inputs payment information and is assured their data will be protected with encryption and tokenization. Without a gateway, organizations would have no compliant method of capturing and storing sensitive card or ACH data on the web.

2. Processors make the transaction happen

After the data is collected securely, the payment processor comes in. It sends messages to card networks such as Visa, Mastercard, American Express, and Discover, along with the issuing bank, to check for funds. It sends money to the receiving bank so merchants receive payment. If there were no processor, even the most secure checkout would not work because no money would transfer.

3. Together, they prevent fraud and errors

If you use the processor alone, customer information would be at risk, which is a serious threat under ABA and PCI DSS regulations. If a gateway alone is used, the payments would be stuck in "pending" limbo without movement. Together, gateways and processors ensure secure authorization, U.S. regulatory compliance, and consistent execution.

Here are some payment gateway vs payment processor examples to show why both are required for a transaction to be successful.

Example 1: When a customer purchases shoes from an online store, the payment gateway securely collects card information, while the processor communicates with Visa and the issuing bank to facilitate the transfer of funds.

Example 2: When a person pays using PayPal or Apple Pay, the gateway facilitates secure input and encryption of the payment information, while the processor sends the transaction over the correct banking networks and settles the funds into the merchant account.

Without gateways, we cannot securely capture customer data. Without processors, the money never transfers. The processor vs gateway relationship is interdependent.

{{banner1.1}}

Challenges in Managing Payment Processors and Gateways

While gateways and processors facilitate smooth transactions and customer ease, they also present operational, compliance, and strategic issues that need to be carefully monitored. They include:

1. Regulatory Compliance and Security

Having multiple payment gateway and payment processor complicates the monitoring of compliance and geographic standards like PCI DSS, NACHA (for ACH), FFIEC cybersecurity guidelines, and ABA best practices. One gap in encryption, tokenization, or authentication can incur penalties and loss of trust.

2. Fraud and Risk Management

With the rise of real-time and online payments, fraud attempts have become more advanced. Banks must ensure that security controls are balanced with transactional speed and a seamless user experience across multiple processors and gateways. If not, there are elevated chargebacks, greater risk exposure, and regulatory action from organizations such as the CFPB.

3. Integration Complexity

Operations now span multiple geographies, payment systems, and customer bases. In the absence of robust integration frameworks, there are more delays, inconsistencies, and technical debt that hinder innovation.

4. Operational Costs and Revenue Leakage

Various processors charge different fees, have unique interchange rates, and have different settlement calendars. Without centralized control, these can result in hidden expenses and revenue leakage.

5. Customer Experience and Reliability

Customers expect instant and guaranteed payments, whether they swipe a card, pay through a mobile wallet, or via ACH/real-time transfers. Any unsuccessful or delayed transaction not only frustrates the customers but also erodes trust.

6. Data Fragmentation and Reconciliation

Each payment gateway and payment processor create its own report formats, data formats, and settlement files. For financial institutions that process millions of transactions every day, payment gateway reconciliation of these records increases errors, lengthens financial close cycles, and complicates compliance reporting.

7. Vendor Dependency and Contractual Rigidities

Banks often utilize third-party vendors for their key payment infrastructure. Although this facilitates speed to market, it also causes vendor lock-ins, rigid service contracts, and excessive switching costs..

8. Cross-Border Payments and Standardization

Cross-border payment management adds an extra level of complexity with different compliance regimes, FX conversion mechanisms, and settlement cycles. The absence of a uniform international standard means it becomes challenging to provide transparent, low-cost, and efficient cross-border payment services.

How Osfin Simplifies Payment Operations

While payment processor vs gateway carries their own strengths, dealing with them individually poses challenges such as data fragmentation, incompatible reports, and compliance risks. Osfin resolves this by providing an end-to-end reconciliation and compliance-ready system:

1. Seamless Data Ingestion:

Osfin is a file-format agnostic platform that can handle any file format and import records from multiple platforms through 170+ integrations. It even applies custom tolerance rules before reconciliation starts to eliminate low-quality data, duplicates, or outliers at the intake level. This saves time by preventing problems instead of fixing them later.

2. Automated Record Matching:

Whether it's one-to-many or many-to-one matching, Osfin's logic-driven engine reconciles 30 million records in just 15 minutes with 100% accuracy. It even automatically reconciles payment gateway reports, splitting them into commissions, taxes, and fees so finance teams don't spend hours chasing numbers.

3. Smart Exception Management:

Osfin places each unmatched transaction with explicit reasons and delivers them to the appropriate team member for resolution via its integrated ticketing and exception engine. Live dashboards monitor it all in real-time, from match status to exposure and exception queues.

4. Compliance and Security:

Osfin provides compliance-ready reports and maintains fully traceable, audit-proof workflows. With 256-bit encryption, role-based access controls, and two-factor authentication, the platform is both secure and intelligent. And it ticks all the right boxes - SOC 2, PCI DSS, ISO 27001, and GDPR.

Final Thoughts

Payment processor vs payment gateway are two sides of the same coin. The gateway takes and stores customer information, while the processor processes and settles the transaction. Both are necessary for smooth, secure, and efficient payment operations.

But maintaining them as separate entities usually results in operational complexity. That's where Osfin steps in, providing businesses with a single, smart layer that simplifies reconciliation, compliance, and settlement monitoring.

FAQs on Payment Processor vs Payment Gateway

1. Is Visa a payment processor or gateway?

Visa is a payment processor. It mediates between banks, merchants, and customers to securely authorize and settle card transactions.

2. What is the difference between payment gateway and processor?

A payment gateway receives and encrypts customer payment information, whereas a processor communicates with the banks and card networks to process and settle transactions.

3. What else is called a payment gateway?

A payment gateway can also be referred to as a "merchant gateway" or "online payment gateway," as it allows businesses to receive secure payments from customers over the internet.

4. How is a payment gateway different from API?

A payment gateway is the service that facilitates transactions, whereas a payment API is the technical interface that developers use to link websites or applications to the gateway.