AI in Fintech: Use Cases, Benefits & How It Works

Just a few years ago, banking meant tedious branch visits and confusing paper forms. Getting your loan approved required weeks of manual review. Fraud investigators found breaches days after they occurred. Stock trades required phone calls to brokers. Customer service operated 9-to-5 with endless hold times. And sending money internationally often meant waiting days and paying extremely high fees.

The point is that financial services were slow, expensive, and accessible only during specific hours.

Now consider this: Loans get approved in minutes. Suspicious transactions trigger alerts instantly. Millions of trades execute per second. Virtual assistants answer questions at midnight. Money crosses borders in real-time. And personalized financial advice adapts to your spending patterns automatically.

This dramatic shift, where intelligence meets finance, is possible because of a powerful combination of AI in fintech. Read on to explore what AI in fintech means and more.

What is AI in Fintech

AI in fintech as is evident is using artificial intelligence technologies to simplify financial services, help with better decision-making, and offer experiences more appropriately-suited to your needs and goals.

AI has the ability to analyze large amounts of datasets at unprecedented speed and identify patterns that humans generally ignore. And with the help of the analysis, it helps financial institutions by predicting future outcomes with remarkable accuracy. This directly helps reduce customer churn rate, plug revenue leakages, prevent regulatory penalties, and make faster, more confident decisions across the business.

This level of efficiency is possible through:

- Machine learning algorithms that improve through experience. Here, they help by detecting fraud and assessing credit risk by learning from millions of transactions.

- Natural language processing (NLP) helps chatbots and virtual assistants understand what problems customers are facing and respond in a more natural and human-like way.

- Predictive analytics helps businesses anticipate the latest trends in the market, the way customers behave, and potential risks, so decisions can be made proactively instead of reactively.

How AI Works in Fintech

Core AI Technologies

The base of AI in fintech is formed by Machine learning models. Their ability to recognize patterns that humans might miss is what’s useful here. ML algorithms keep learning from millions of transactions, improving their ability to detect discrepancies or fraud, assess credit risk, and predict customer behavior.

Consider this statistic: Traditional anti-money laundering systems generate up to 95% false positives. But with machine learning, you can dramatically reduce such false alarms by understanding actual contexts and historical patterns.

The next AI tech is Natural language processing (NLP): The capability of machines to understand human language as it is. The best use case of this is seen in customer service, where chatbots, and virtual assistants make customers feel as if they are conversing with humans. This is actually something that approximately 72% of financial institutions are trying for customer support.

Another major feature is predictive analytics. That’s how AI models can forecast future trends by analyzing historical data and current patterns.

Some fintech firms applying it in treasury and risk operations are already seeing results: 2x faster response times to market shifts and a 15-20% reduction in losses tied to exposure.

These models predict everything from loan defaults to market fluctuations, so that you can make decisions even before problems occur.

Lastly, AI is bringing smarter automation in the reconciliation domain as well. For a very long time, financial institutions had to rely on manual, extremely time-intensive processes to reconcile enormous volumes of transactions across multiple systems and data sources. But with AI, the matching and discrepancy flagging can all be automated.

What’s more, AI can actively learn from feedback related to historical mismatches to improve accuracy over time, and easily reduce the overdependence on humans.

However, AI's effectiveness also depends on data quality and volume.

Data as the Foundation

Financial institutions train AI using transaction histories, customer interactions, market movements, and behavioral patterns. The richer the data diet, the sharper the intelligence, and the more accurately AI can identify trends for you, predict outcomes, and personalize services for your customers. This foundation is built on three vital elements:

1. Real-time data processing

Real-time processing separates modern AI from traditional analytics. AI examines transactions, customer behavior, and market activity as they occur, so you can take instant actions.

2. High-quality data

The quality of data matters a lot. Accurate, complete, and unbiased data is something you can’t compromise on. If your AI is trained on incomplete records, outdated information, or biased historical patterns, it will always produce flawed recommendations, no matter how sophisticated your algorithms are.

3. Strong data governance

Without governance frameworks, your data foundation is built on quicksand. Needless to say, as a financial institution, you can't afford inconsistencies that corrupt model outputs, outdated records that generate false signals, or inaccurate information that erodes client trust.

But it doesn’t end there. Governance solves only half the equation. The other half? Extracting maximum intelligence from customer data while honoring the privacy those same customers expect.

{{banner1}}

Key Use Cases of AI in Fintech

Some of the examples of financial processes that AI helps simplify include:

1. AI-Powered Reconciliation

AI is modifying the way reconciliation is processed. Earlier, most teams used to do it manually: matching entries, checking spreadsheets, and then spending half the time figuring out why the numbers weren’t lining up. Needless to say, it was slow, repetitive, and mistakes were hard to avoid.

AI can match records from multiple systems even when they don’t line up perfectly. Once that is done, it standardizes the data, which avoids a lot of confusion during comparison.

Over time, these tools also start picking up common patterns. So, if the same kind of matches keep happening, the system can automatically suggest matching rules based on that logic instead of the team having to build everything manually.

Exception handling becomes easier too. Instead of reviewing every line item, teams can directly focus on the entries that genuinely need attention.

And if something is still pending, it stays on the radar until it’s resolved.

2. Detecting Frauds & Ensuring Security

The traditional way to detect fraud was quite rigid. Transactions got flagged when they crossed certain amounts or were made from specific locations. This approach failed because criminals quickly learned these patterns and worked around them.

But AI understands normal behavior for each customer and spots deviations instantly. How does that happen? Well, these systems analyze thousands of behavioral signals in one go, like spending patterns, device fingerprints, transaction timing, and merchant types. Then, they build dynamic profiles that evolve as your habits change.

The crux of the matter is that the technology adapts as fraud tactics change. For instance, nowadays, it’s becoming common for criminals to use deepfakes for identity theft. Or AI-generated phishing messages that mimic legitimate communications perfectly.

But financial institutions are equally capable of countering this with just as sophisticated defenses that detect fake identities, analyze voice patterns during authentication calls, and identify subtle anomalies in digital signatures that humans would miss.

3. Credit Scoring & Loan Decisions

Traditional credit scores locked millions out of borrowing, such as students without credit cards, immigrants new to the country, and gig workers with irregular income streams. They had repayment capacity but no credit history to prove it.

AI evaluates alternative data sources that reveal financial responsibility beyond conventional metrics. Consistent loan repayments, rental history, educational background, employment patterns, and even mobile phone usage can now be used to assess creditworthiness.

4. Automated Trading & Investment Tools

AI-adopted trading systems make decisions in milliseconds. This is possible as they can digest varied amounts of insights like market data, corporate earnings, social media sentiment, economic indicators, and global news simultaneously.

Retail investors now have access to strategies that were once reserved for institutional traders only. Platforms offer algorithmic trading tools that automatically buy assets, set stop losses, or execute dollar-cost averaging without constant monitoring.

5. Customer Service & Chatbots

AI chatbots answer your customers’ queries in an instant, understand questions in human-speak, and access complete account history in real-time.

AI understands context, detects frustration in messages, and forwards complex issues to human agents. Ask about suspicious charges, and it explains recent transactions. Need to dispute a fee? It initiates the process immediately.

In short, banking at midnight becomes as convenient as banking at noon.

6. Personalized Financial Planning

Traditional financial advisors required minimum account balances to access professional wealth management. There’s no such thing with Robo-advisors.

They just ask about your goals, risk tolerance, and timeline, and then automatically build diversified portfolios accurately adapted to your situation. What’s more, they rebalance when markets shift your asset allocation, harvest tax losses to reduce your liability, and adjust strategies as you age, all without any human intervention needed.

Future Trends in AI for Fintech

The AI in the fintech market is expected to grow to $190.33 billion by 2030. This data clearly shows how the rapid velocity with which this technology is being adopted across financial institutions. Let’s see how AI will change in the financial landscape in the coming years:

Agentic AI & Autonomous Finance

The next generation of financial AI won't wait for instructions; it will act independently within defined parameters. Unlike current systems that recommend actions, agentic AI executes complete workflows autonomously.

Such intelligent agents learn from outcomes and adapt strategies continuously. They coordinate across multiple systems and make decisions in real-time.

Real-Time Payments & ReconciliationDecisioning

Instant payment systems are rising. There’s nothing new about it. But AI integration with these systems can transform this speed into intelligence.

Usually, when transactions are processed instantly, there's no time for manual fraud review or traditional credit checks. But with AI, evaluation of transaction legitimacy, credit risk assessment, and transfer approvals can all happen simultaneously, and that too within milliseconds.

Real-time payments also mean reconciliation can’t be delayed. Since transactions are settled instantly across different payment rails, AI helps match incoming and outgoing records as they happen. Instead of waiting until the end of the day to find mismatches, discrepancies can be spotted immediately.

This gives finance teams a clearer, up-to-date view of transactions, with little to no gap between when a payment is made and when it gets reconciled.

AI for Financial Inclusion

Multilingual AI breaks down language barriers that used to exclude non-English speakers from advanced financial services. Voice-first interfaces powered by NLP allow users in rural areas without banking experience to interact with financial systems using their native languages and dialects.

AI also assesses creditworthiness using digital footprints. Mobile usage patterns, utility payment consistency, social commerce activity, and even geolocation data reveal financial responsibility for populations invisible to conventional credit bureaus. In emerging markets where smartphone ownership exceeds bank account penetration, these alternative assessment methods unlock access for hundreds of millions previously excluded from formal financial systems.

Explainability & Trust

As AI takes on bigger financial decisions, it can’t operate like a mystery box. When a customer is denied a loan or flagged for fraud, they deserve a clear reason. This is where explainable AI comes in. It shows why a decision was made.

This level of transparency also means smart business. When you can explain how your AI works, you earn customer trust, meet regulatory expectations, and catch bias or errors early. And when customers understand why their application was rejected, and what they can improve, they’re given clarity and a way forward, instead of feeling unfairly shut out.

Regulatory Evolution

Governments around the world are stepping in to set clear rules for how AI should be used in finance.

In the European Union, the AI Act labels many financial AI systems, such as those used for credit approval, as “high risk.” Basically, the law wants banks to be completely transparent about how their AI systems work, regularly test them for biases, and make sure humans can take charge in decisions that have major impact on people’s lives.

Something similar is happening in the U.S. as well. Regulators are issuing guidelines that focus on transparency, the quality of training data, and the ability to explain AI-driven decisions.

By clearly defining what’s allowed, regulators create a fair playing field where responsible use of AI becomes a competitive advantage. Remember that financial institutions that invest early in compliant, trustworthy AI systems position themselves as reliable partners.

{{banner1.1}}

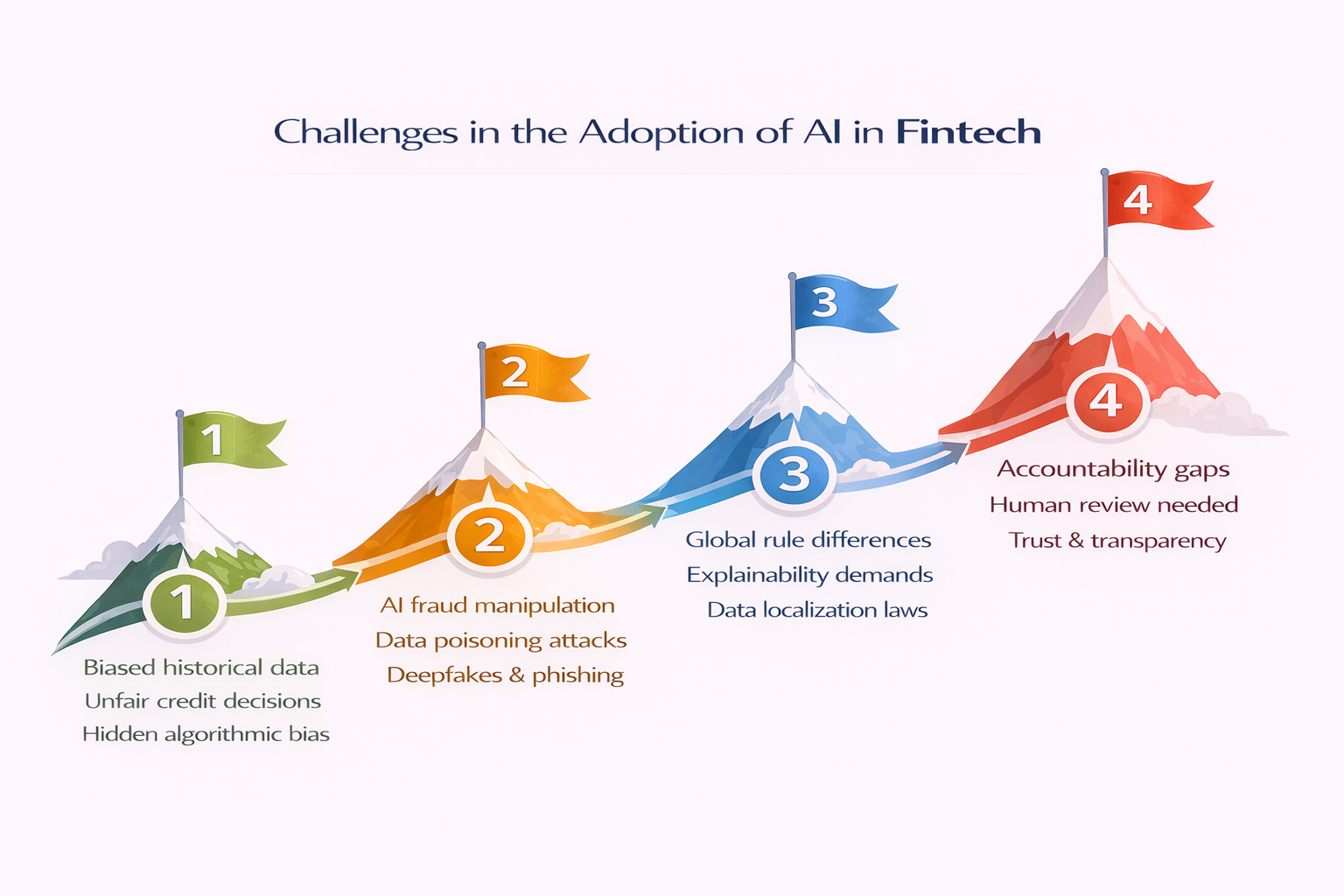

Challenges & Risks

Here are some challenges and risks that you should be aware of before adopting AI in fintech:

1. Data Bias & Fairness

AI learns by looking at history. But if historical data itself includes years of unfair treatment, your AI can end up behaving in a similar fashion.

For example, credit models trained on old lending decisions may pick up biases against certain neighborhoods, professions, or demographic groups. The downside being that qualified applicants may be rejected simply because the system learned from a past that was unfair.

What’s even more dangerous is the objectivity tag attached to it. When a human makes a biased decision, it can be questioned or challenged. But what if an algorithm does the same? It’s often defended as being data-driven.

Preventing this requires deliberate effort. You need to regularly check models for unfair patterns and use more diverse and representative data free of biases.

2. Security & Cyber Threats

AI systems have become attractive targets for cybercriminals. Attackers don’t always break in loudly; they often try to trick the system instead. Just a subtle change in transaction pattern, and they can make fraudulent activity look normal, even to AI-based fraud detection tools.

They can even tamper with training data. It’s not difficult to teach AI systems to wrongly approve or ignore certain actions. When the systems get breached in such a fundamental way, the damage is widespread, exposing massive datasets and putting millions of customers at risk at once.

At the same time, criminals are using AI as a weapon. With Deepfake technology, they can mimic a customer’s voice or face during identity checks. Or create AI-generated phishing messages that are almost impossible to differentiate from real bank communications.

When financial institutions strengthen their defenses, it’s worth bearing in mind that attackers have the same technology at their disposal and can evolve just as quickly. So, what’s the way forward? Constant monitoring, regular updates, and sustained investment in security.

3. Regulatory & Compliance Complexity

Financial institutions operate across countries, and each region has its own rules for how AI should be used. In Europe, regulations emphasize explainability. In the U.S., regulators focus more on testing models for bias and fairness. Many Asian markets, meanwhile, prioritize data sovereignty, requiring data to stay within national borders. Designing AI systems that meet all these requirements at once quickly becomes complex and costly.

There’s also a tradeoff at the technical level. The most accurate AI models are often the hardest to explain, yet regulators increasingly expect transparency. Even the teams building these systems can struggle to fully explain how models with millions of parameters arrive at specific decisions.

4. Ethical Use & Human Oversight

Fully autonomous AI raises difficult questions. When an algorithm makes a serious mistake, who is responsible? Should a machine be allowed to reject someone’s mortgage application without any human review? And at what point does automation stop being helpful and start feeling impersonal?

Responsible oversight depends on people who understand both finance and AI, a skill set that’s still rare. Teams need to know when to trust automated decisions and when to step in. Finding this balance of keeping humans meaningfully involved without undermining automation remains one of the biggest ethical challenges in fintech.

Conclusion

AI has no doubt reshaped the fintech’s value chain and will continue to do so. From fraud detection and credit decisions to trading algorithms and personalized advice, no function remains untouched. At the same time, increasing reliance on AI introduces new risks, responsibilities, and ethical considerations that cannot be ignored.

The future of fintech will belong to institutions that pair innovation with responsibility. Something platforms like Osfin are known for.

Osfin is an automated reconciliation platform that helps banks and financial institutions reconcile millions of transactions within minutes. This format-agnostic platform integrates data from 170+ sources regardless of format, matching 30 million records in 15 minutes with 100% accuracy, and automatically flagging exceptions with complete audit traceability.

Moreover, Osfin ensures complete security and compliance. It maintains SOC 2, PCI DSS, ISO 27001, and GDPR compliance, and keeps your data secure with 256-bit encryption, maker-checker flow, role-based access, and two-factor authentication.

{{banner3}}

FAQs

1. What is AI in fintech?

AI in fintech refers to the use of intelligent technologies to automate financial processes. AI helps financial institutions analyze data, detect fraud, and deliver faster, more personalized financial services to customers.

2. How does AI improve financial risk management?

AI improves financial risk management by analyzing large datasets in real time. This helps detect risks early, predict losses, prevent fraud, and support more accurate decision-making across financial operations.

3. What are the major use cases of AI in fintech?

AI in fintech can be used for fraud detection, automated trading and investments, fair credit scoring, personalized financial planning, and customer support.

4. What are the challenges of implementing AI in fintech?

While leveraging AI to simplify fintech, you can encounter challenges like biases, cybersecurity threats, complex regulatory changes, and ethical concerns over decision-making.

5. How will AI shape the future of financial services?

In the future, AI will be able to automate complex decisions with Agentic AI, integrate with real-time payments for better security and transparency, and promote financial inclusion.