Payment Gateways Explained: Secure Payments for Any Business

Over the past decade, digital payments have transformed the way money moves around the world. From small retailers accepting online orders to global corporations managing cross-border transactions, businesses are looking for fast, secure, and reliable ways to get paid.

Banks, fintechs, and financial institutions have stepped up to provide solutions that simplify payments while making them safer and more transparent. At the center of this ecosystem is the payment gateway, a technology that connects customers, merchants, and banks during every online transaction.

Payment gateways have had a major impact on e-commerce, subscription services, travel, and even recurring billing in sectors like insurance and utilities. They reduce friction for customers while giving businesses confidence that payments will be processed smoothly.

This article explores what a payment gateway is, how it operates, the types available, the benefits and challenges, and how reconciliation tools like Osfin add value to this digital payments space.

What this blog covers:

- What a payment gateway is and how it works

- Different types and deployment models

- Benefits and challenges of using a gateway

- How Osfin integrates with gateways for reconciliation

- Tips for choosing the right gateway

- Best practices for selecting and implementing payment gateway solution

- Frequently asked questions and practical insights

What is a Payment Gateway?

A payment gateway is a digital payment solution that securely connects customers, merchants, acquiring banks, and payment processors to enable smooth and safe online transactions. Its primary role is to authorize, encrypt, and transmit payment data so that every transaction is carried out safely and efficiently.

Payment gateways are built and maintained by different providers. Some are offered by traditional banks as part of their online banking services, while others are developed by fintech companies specializing in payments technology. Well-known global names like Stripe, PayPal, and Razorpay are examples, but many banks also run their own gateway systems.

How Does a Payment Gateway Work?

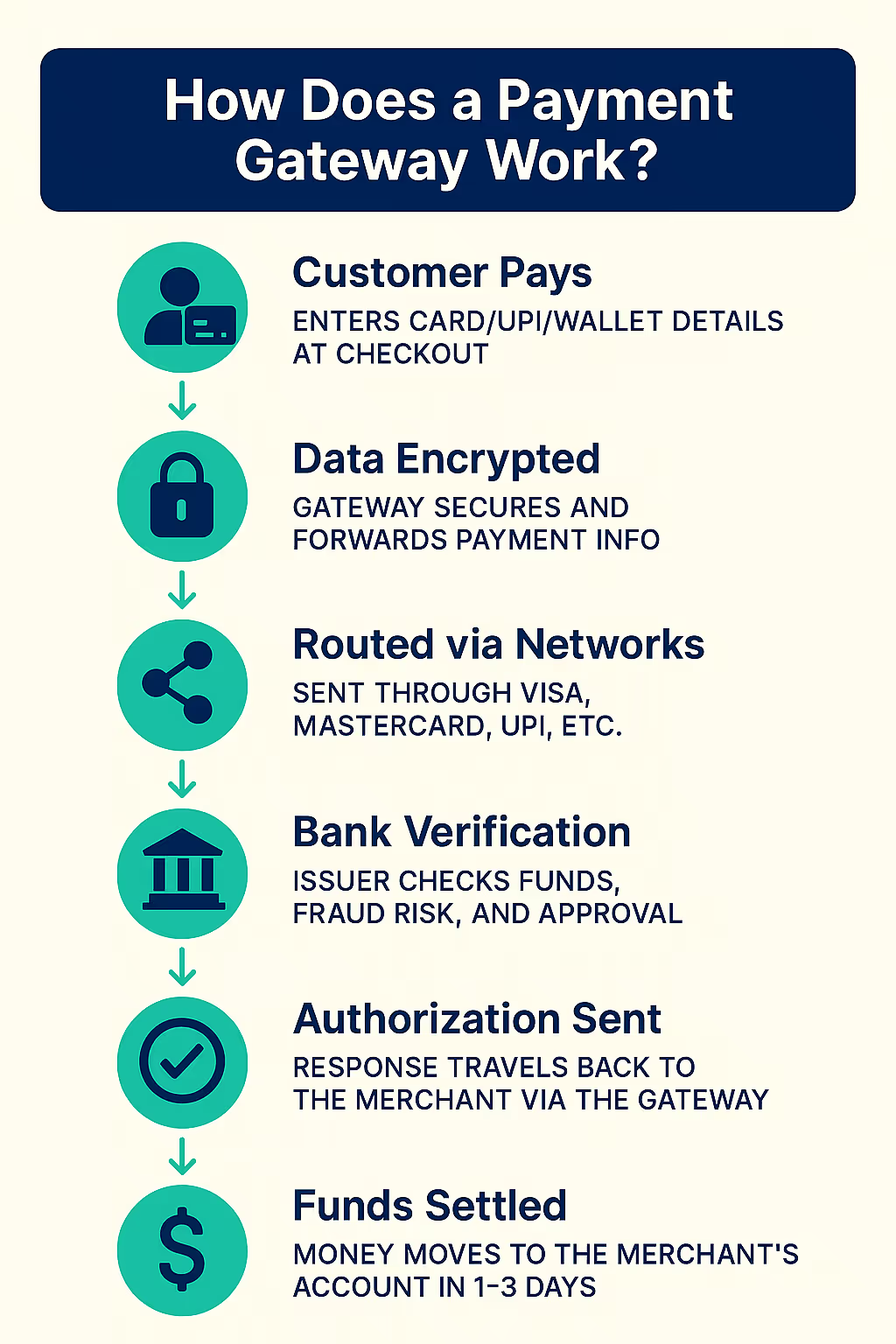

A payment gateway process may look instant from the outside, but there are several steps happening in the background every time a customer makes a payment. Here's how payment gateways work:

Step 1: Customer Initiates the Payment

The process starts when a customer enters their card, UPI, or wallet details at checkout. The gateway immediately encrypts this sensitive data so it cannot be intercepted or misused.

Step 2: Gateway Sends the Request

Once encrypted, the payment details are sent to the acquiring bank or payment processor. This is the bank or partner that works with the merchant to process digital transactions.

Step 3: Routing Through Networks

The request is then routed through relevant networks such as Visa, Mastercard, or UPI. These networks act as traffic controllers, directing the request to the correct issuing bank.

Step 4: Issuer Bank Verification

The customer's bank (the issuer) checks whether the account has enough funds and if the transaction looks genuine. Fraud checks, PIN validation, and security protocols like OTPs happen at this stage.

Step 5: Authorization Response

Based on the checks, the issuer either approves or declines the transaction. This decision travels back through the network and the acquiring bank, and finally reaches the gateway, which relays the result to the merchant's site.

Step 6: Settlement of Funds

If approved, the actual transfer of money begins. The issuer sends the amount to the acquiring bank, which eventually credits the merchant's account. Settlement usually takes one to three working days, depending on the provider.

Example of a Payment Gateway in Action

Let's understand how a payment gateway works. Say a customer is buying a pair of shoes from an online store. Here's how this transaction plays out step by step:

- At checkout, the customer selects card payment and enters their details.

- Instantly, the payment gateway encrypts this information and sends it to the acquiring bank.

- The request is passed through the card network to the issuing bank, which checks the account balance and security details.

- Within seconds, the issuer approves the payment. The response flows back through the network and gateway to the online store.

- The customer receives a confirmation message on the website, while the merchant receives assurance that the payment is authorized.

- Behind the scenes, the funds are moved to the merchant's bank account within the settlement cycle, usually one to three days later.

Types of Payment Gateways

There are various types of payment gateways based on how they integrate with the merchant's platform or app. Here are the main types of gateways and how they function.

1. Hosted Payment Gateways

With this type of gateway, customers are redirected to a third-party page to complete their payments. It's simple to integrate and highly secure, but it takes users away from the merchant's site for checkout.

2. Self-Hosted Payment Gateways

Here, payment details are collected directly on the merchant's website and then securely sent to the gateway. It gives businesses more control over branding, but also demands stronger compliance measures.

3. API-Hosted Gateways

These allow payment integration via APIs, creating a seamless checkout without redirection. Merchants benefit from full customization, though it requires technical expertise and stricter data security handling.

4. Local Bank Gateways

Offered by banks, these gateways are quite simple but often have limited flexibility in features or scalability compared to fintech-driven solutions.

Benefits of Payment Gateways for Businesses

Adopting the right payment gateway allows businesses to stay competitive in a fast-moving digital economy. Here's how businesses benefit from adopting payment gateways:

1. Faster Transactions Strengthen Business Operations

Speed is central to digital commerce. Payment gateways process authorizations in real time, giving both customers and businesses immediate confirmation of a transaction. This reduces waiting periods, accelerates order fulfillment, and provides businesses with more predictable cash flow for day-to-day operations.

2. Strong Security Protects Revenue and Reputation

Handling sensitive financial data demands the highest level of protection. Gateways apply encryption, fraud detection, and PCI-DSS compliance to safeguard each transaction. Businesses benefit by reducing chargebacks and fraud losses, while also building customer trust in their brand's reliability.

3. Global Reach Opens New Growth Opportunities

Expanding into new markets often comes down to accepting local payment preferences. Gateways that support multi-currency and international cards make cross-border transactions seamless. Businesses can serve global customers without facing the complexity of setting up separate payment systems in each region.

4. Seamless Checkout Builds Customer Confidence

Gateways that integrate with multiple methods, cards, UPI, net banking, or wallets, offer customers flexibility and convenience. When customers can pay quickly without errors or repeated attempts, conversion rates rise, and loyalty follows.

Payment Gateway in Banking & Finance

Banks and financial institutions act as facilitators of payment transactions or as providers of their own gateway services. Each role involves different responsibilities and brings distinct benefits.

When Banks Facilitate Payment Gateway Transactions

When a payment gateway processes a transaction, banks are heavily involved behind the scenes:

- Acquiring Banks work directly with merchants to accept digital payments. They receive payment requests from gateways and handle settlement into the merchant's account.

- Issuing Banks verify customer details, check account balances, run fraud checks, and approve or decline transactions.

- Clearing and Settlement obligations are managed through banking channels, ensuring that funds move reliably from the customer to the merchant.

- Compliance and Risk Oversight is maintained, with banks applying regulatory checks like AML, KYC, and transaction monitoring.

In short, banks provide the trust layer that keeps payment gateways operational, secure, and compliant.

When Banks Provide Their Own Payment Gateways

Some banks go beyond facilitation and develop their own payment gateway systems for merchants. Doing so brings them several advantages:

1. Direct Merchant Relationships: By offering gateways, banks deepen their engagement with businesses and secure long-term partnerships.

2. Revenue Streams: Transaction fees, settlement charges, and value-added services create an additional line of income.

3. Brand Credibility: Businesses often trust a bank-run gateway more, given the reputation and regulatory oversight banks already hold.

4. Integrated Services: Banks can bundle gateways with merchant accounts, loans, and other financial services, creating a full-service package.

Challenges & Considerations of Payment Gateway

While gateway payment processing has become the backbone of digital commerce, it comes with challenges that businesses and financial institutions cannot ignore. These challenges impact compliance, reputation, and financial accuracy.

1. Security Risks in Online Transactions

Fraud remains one of the biggest threats when it comes to online payments. Hackers target gateways with phishing, credential theft, and card-not-present fraud. To counter this, gateways must use encryption, tokenization, and fraud detection. Security standards like the PCI-DSS (Payment Card Industry Data Security Standard) apply globally, and failure to comply can result in heavy penalties.

2. Data Privacy Concerns

Gateways handle sensitive financial data that must be protected under strict privacy laws. In the EU, GDPR requires businesses to safeguard personal data, while CCPA in California enforces similar obligations. India has recently rolled out the Digital Personal Data Protection Act (DPDP, 2023). Non-compliance with these local and international regulations hefty penalties.

3. Regulatory Compliance Obligations

Beyond data privacy, gateways must align with financial regulations. In the US, FinCEN monitors suspicious activity, in Europe, PSD2 enforces strong customer authentication, and in India, RBI regulations govern transaction security and storage of payment data. Each market imposes unique obligations, making global operations complex for gateways and the businesses using them.

4. Financial Accuracy and Reconciliation

Even when transactions are secure and compliant, discrepancies can occur during settlement. Fees, taxes, and chargebacks may lead to mismatches between gateway reports and bank credits. Without timely reconciliation, businesses risk financial leakage and accounting errors. Automated reconciliation tools like Osfin.ai help detect settlement delays, duplicate entries, or missing funds, ensuring financial accuracy in gateway payment processing.

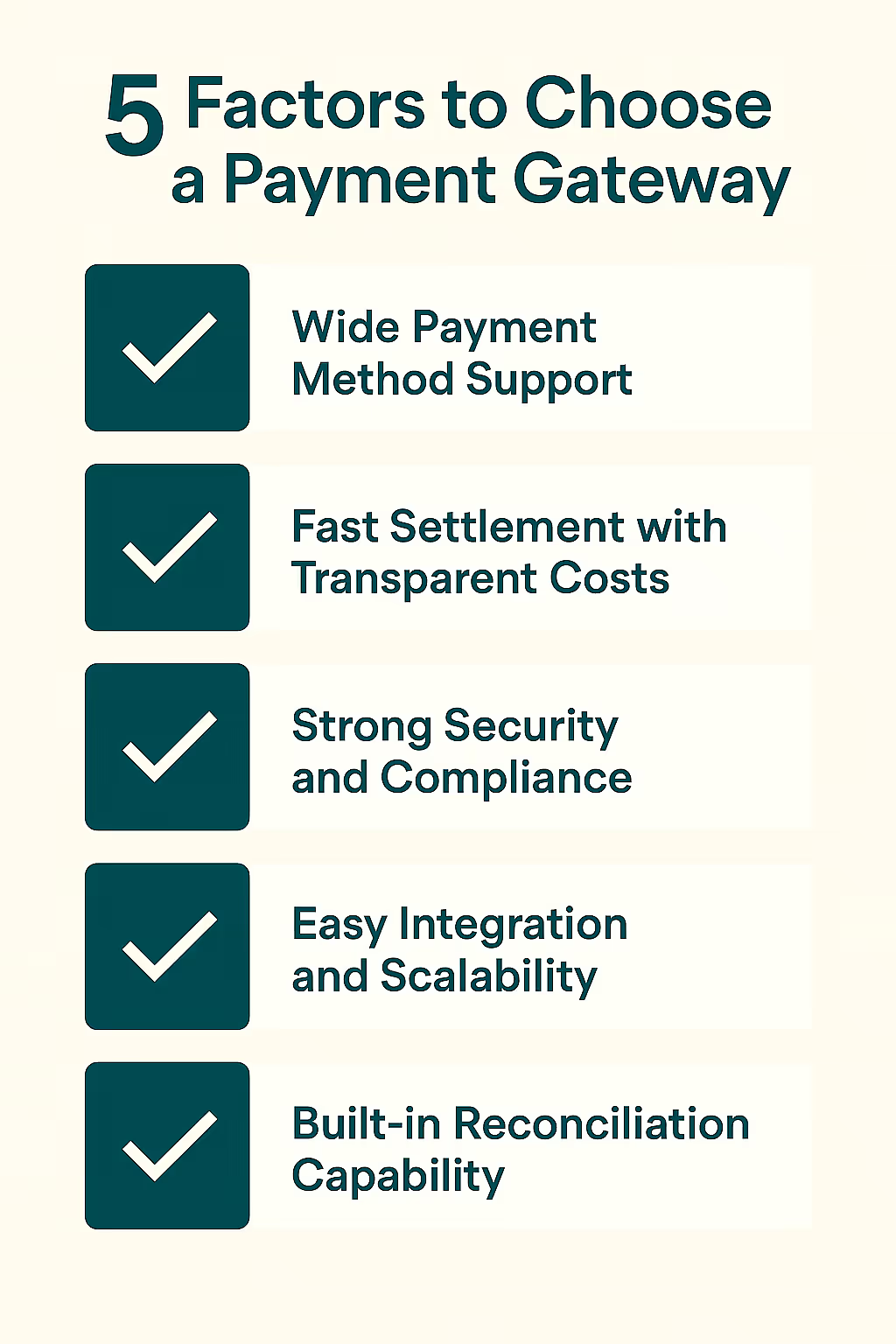

How to Choose the Right Payment Gateway

Choosing a payment gateway can feel overwhelming with so many providers out there. The best way to approach it is to focus on what will make payments reliable, secure, and easy to manage for your business. Here are five factors worth paying attention to.

1. Range of Payment Methods

Look for a gateway that supports multiple ways to pay, like cards, UPI, net banking, and wallets. If you sell internationally, make sure it also handles multi-currency payments. More options mean more successful transactions.

2. Settlement Speed and Costs

Settlement cycles differ between gateways. Some providers transfer funds the next day, while others take a few days. When you combine this with transaction fees and hidden charges, you'll see how much it affects your margins over time. Select a payment gateway that offers a settlement timeline that works best for you, along with transparent fees.

3. Security and Compliance

Every transaction involves sensitive customer data. Gateways should meet standards like PCI-DSS and follow regional rules such as GDPR, PSD2, or RBI guidelines. Features like encryption and fraud checks are must-haves.

4. Integration and Scalability

A gateway should connect smoothly with your website, app, or ERP. As your volumes grow, it should scale without slowing down or breaking during peak traffic. Downtime at the checkout is the fastest way to lose customers.

5. Reconciliation Support

Payments don't stop once the customer sees "successful." You still need to match settlements, fees, and refunds accurately. Gateways that work well with reconciliation tools make this process much simpler.

Osfin.ai is a file-format agnostic platform that handles any format and can ingest data from multiple sources using 170+ integrations. It easily connects with your payment gateway, pulls transaction data, and automatically reconciles it with 100% accuracy. Want to see how Osfin works? Book a demo today!

What is Payment Gateway Reconciliation and Why Does it Matter?

For banks and financial institutions that facilitate gateway payments, keeping every transaction aligned across systems is essential. Payment gateway reconciliation is the process of matching sales recorded by the merchant, payment confirmations logged in the payment gateway, settlement reports from the acquiring bank or processor, and the final credits reflected in the core banking system. By reconciling these records, institutions can ensure accuracy at every stage and prevent revenue leakage.

Here's why this matters:

- It helps identify failed, duplicate, or pending transactions that may not have been settled correctly.

- It ensures that fees, taxes, and interchange charges applied by processors match what was agreed upon.

- It provides early visibility into settlement delays, allowing faster resolution with payment partners.

- It maintains accounting accuracy by aligning gateway reports with internal ledgers and bank statements.

- It supports regulatory compliance by keeping a clear audit trail of all processed transactions.

How Osfin Simplifies Payment Gateway Reconciliation

Payment gateway reconciliation requires pulling data from multiple sources, including merchant sales records, payment gateway reports, acquiring bank settlement files, and the core banking system. Traditionally, this meant creating multiple spreadsheets and manually matching transactions line by line.

The problem is that data often arrives in different formats, with varied naming conventions, making manual reconciliation slow, error-prone, and almost impossible at the scale banks and financial institutions handle daily.

This is where Osfin.ai shines. Osfin is an enterprise-grade reconciliation automation platform designed for high-volume, complex transaction matching. It is file-format agnostic, capable of processing CSV, XLS, JSON, XML, MT940, and more. With over 170 pre-built integrations, Osfin ingests data seamlessly from payment gateways, banks, processors, and ERP systems. During ingestion, it applies custom deviation tolerances to filter out poor-quality data before reconciliation begins.

Once the data is ready, Osfin matches transactions across systems using logic-based matching. It can reconcile up to 30 million transactions in just 15 minutes with 100% accuracy. Any anomalies, such as missing entries, duplicates, or settlement mismatches, are automatically flagged, tagged with reasons, and routed to the right teams through its exception handling engine.

Osfin also provides real-time dashboards and audit-ready reports so finance teams can monitor reconciliations live and access a clear history of every transaction. Security is built in, with 256-bit SSL encryption, SOC 2 and ISO 27001 compliance, PCI DSS alignment, GDPR readiness, role-based access control, and two-factor authentication.

{{banner1.1}}

Frequently Asked Questions

1. Is a payment gateway the same as a payment processor?

No, they're not the same. A payment gateway securely collects and transmits customer payment data, while a processor handles the actual movement of money between banks. Both work together to complete a transaction seamlessly.

2. What is the difference between a payment gateway and a POS machine?

A payment gateway is used for online or digital transactions, while a POS machine is used in physical stores to swipe cards. Gateways operate virtually, and POS devices are hardware-based, but both authorize and process payments.

3. How long does a payment gateway take to settle funds?

Settlement times vary by provider, but most gateways transfer funds to the merchant's bank within one to three business days. Some offer faster settlements, while cross-border transactions may take slightly longer depending on banking networks.

4. Can a business use multiple payment gateways at once?

Yes, many businesses use more than one payment gateway. This helps reduce failed transactions, manage costs, and provide customers with more payment options. Having multiple gateways also improves reliability during high-traffic or downtime situations.

5. What happens if a payment gateway server goes down during a transaction?

If a payment gateway server fails mid-transaction, the payment may not go through, and the customer is usually asked to retry. Many providers use backup servers and failover systems to reduce downtime and prevent disruptions.