Audit Reconciliation: Meaning, Process & Best Practices (2026 Guide)

To the outside world, your enterprise’s million-dollar balance sheet may look like a monolith of stability. But to you, the one who is responsible for compliance, it is a daily puzzle of thousands of line items, multiple payment rails, and various legacy systems that don’t always play nice together.

Audit reconciliation helps you make sense of it all. In high-volume environments like fintech platforms processing millions of transactions daily, enterprise businesses operating across multiple entities and currencies, or e-commerce platforms managing chargebacks, refunds, and settlement lags, reconciliation is the risk management infrastructure that holds financial reporting together.

In this article, we carefully look into what audit reconciliation is, the reconciliation audit procedures, and why it matters to your business.

What is Audit Reconciliation?

Audit reconciliation is the process of comparing, verifying and documenting all your financial data that exists across multiple sources to confirm that every transaction is recorded correctly and can be supported fully by evidence. This financial data may come from internal ledgers, bank statements, payment processors, sub-systems, and third-party data feeds.

Audit reconciliation extends beyond basic bank reconciliation, which compares a single account’s ledger against a bank statement. Audit reconciliation also extends beyond period-end balance reviews and spreadsheet-based matching. The purpose here is to create a reliable audit trail, where every item has a documented explanation and every adjustment is authorised and supported.

Why Does Audit Reconciliation Matter in Enterprise Environments

In enterprise environments, the margin for error in your financial records is razor-thin. When dealing with millions of line items across different payment rails and legacy systems, audit reconciliation is a non-negotiable control point to have.

Here’s what could be at stake without audit reconciliation:

1. Exposure to regulatory risk

In regulated sectors like fintech, payments, banking and insurance, bodies like the SEC, RBI, and FCA treat minor slip-ups as proof that your controls are not working. The consequences of this can range from enforcement action to losing your operating license.

2. Unreliable financial statements

External auditors use reconciliation as their primary way of checking that your reported balances are accurate. If your reconciliations are incomplete or missing, auditors can’t trust what you’re telling them, so they dig deeper, take longer, and sometimes issue a qualified opinion on your financials.

3. Regulators expect real-time visibility

In high-volume payment environments, regulators want discrepancies between customer balances and internal records to be caught within 24 hours. This is not possible without a proper reconciliation process in place.

4. Board-level visibility

Audit committees now actively monitor reconciliation health as a barometer for how well the business is controlled. When patterns of unresolved exceptions start showing, the board wants clear answers. You can provide these answers only with the visibility that audit reconciliation provides.

5. Scale makes everything more challenging

The more transactions you process, the more places things can go wrong. A fintech handling 5 million daily transactions can’t manually review every mismatch. Every new payment rail, banking partner, or product you add is another surface where unmatched transactions can remain unseen until audit season.

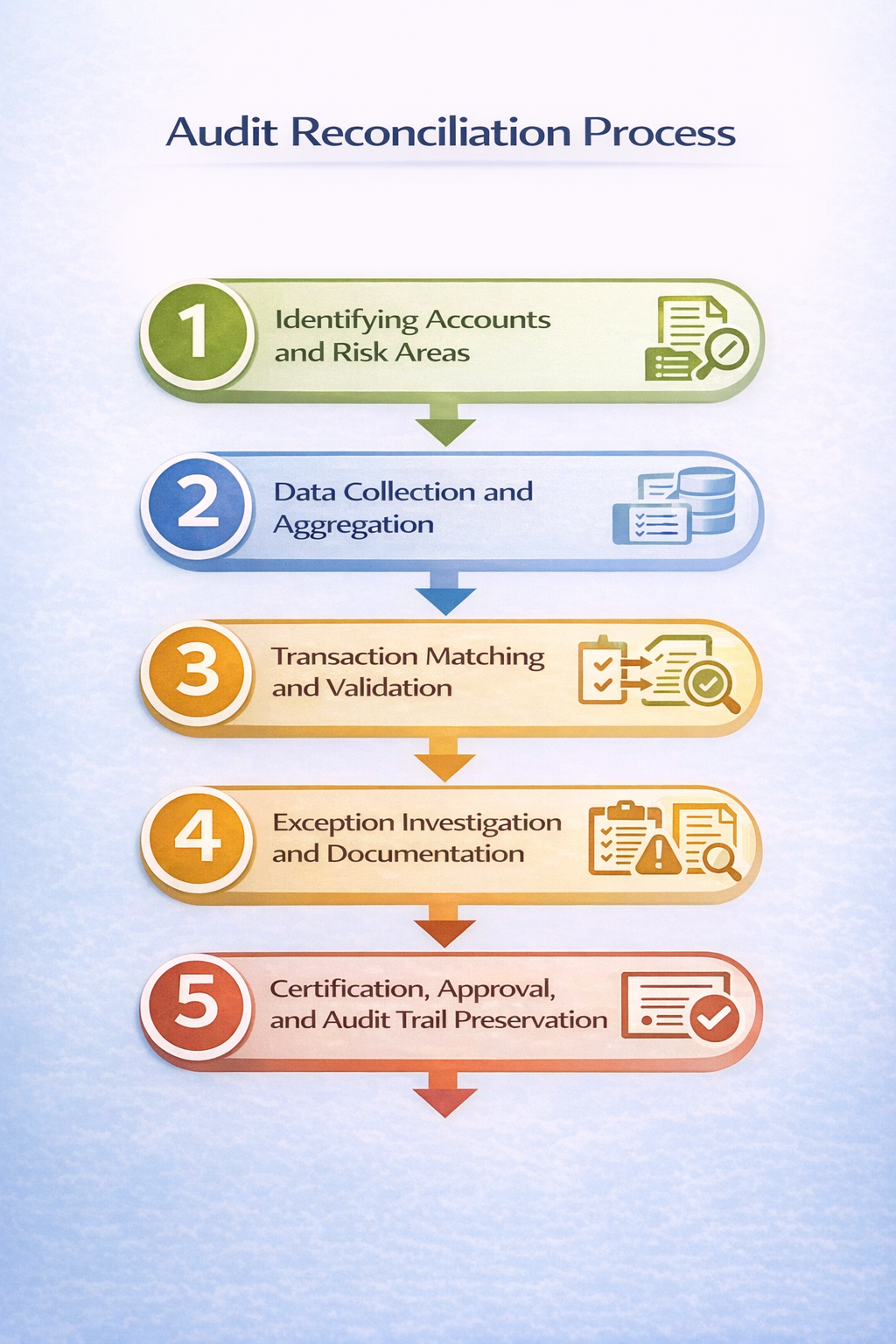

Audit Reconciliation Process: Step-by-Step

1. Identifying Accounts and Risk Areas

You cannot reconcile all your accounts at the same frequency. This would be impractical and wasteful. The first step would be to figure out which of your accounts carries the most risk and needs immediate attention.

High-risk areas are usually:

1. Cash and bank accounts

2. Intercompany balances (money moving between your own entities)

3. Revenue recognition accounts

4. Payment gateway clearing accounts,

5. Any customer liability accounts

Once you’ve identified the risk level of each account, you would need to match it to a reconciliation frequency. High-risk, high-volume accounts need daily or real-time reconciliation. Lower-risk accounts might only need a weekly or monthly check.

2. Data Collection and Aggregation

Once you know what needs reconciling, you need to collect the data. For enterprise businesses, this usually means pulling transaction records from multiple places simultaneously. This means your ERP or accounting system, your bank feeds, payment processors, card network settlement files, e-commerce platforms, tax systems, and FX tools.

This step is to be done carefully, as this is where you may come across issues like duplicate transaction IDs, value dates that don't match across systems, records in different formats or currencies, and missing reference fields that make matching harder. All of this needs to be cleaned and standardised before you start matching.

3. Transaction Matching and Validation

The third step is the main process of your reconciliation workflow. Here, you would take every transaction recorded internally and match it against its corresponding record in an external source. You would also have to do it the other way round to make sure nothing is hiding in the external data that is not in your books.

Different transaction types require different matching logic. Some are simple one-to-one matches. Others involve one internal record matching to several external ones, and some need complex netting arrangements where many records on both sides combine into a single net figure.

During this process, if any items do not get matched, they are flagged for investigation. That leads into the next step.

4. Exception Investigation and Documentation

Every unmatched item needs a proper investigation. You need to identify what caused the discrepancy, how it was fixed, who fixed it and how long it took to fix. If an exception stays open beyond a reasonable time, it needs to be escalated for even more investigation.

At this stage, documenting everything is non-negotiable. Every exception needs a written explanation, a supporting document and approval from someone who didn't prepare the reconciliation. Exceptions closed without evidence will be challenged in any serious audit.

5. Certification, Approval, and Audit Trail Preservation

The final step is turning your completed reconciliation into something an auditor can actually use. After completing the reconciliation, the person preparing it certifies it as complete, and then an independent reviewer approves it.

Once approved, the whole package with source data, matching results, exception log, and resolution evidence is locked and preserved. This is your audit trail.

What are the Most Common Audit Reconciliation Risks?

If not done correctly, audit reconciliation comes with certain risks. Here’s what the most common ones could look like:

1. Aged exceptions that never get resolved

If reconciling items carry forward from one month to the next without any explanation or resolution, auditors see this as a lack of ownership. Aged items can also mask genuine errors that were overlooked during reconciliation.

2. Entries with no supporting evidence

Any adjustment made directly to the ledger without a corresponding reconciliation entry, an approval trail, and backup documentation is an instant audit red flag. These entries bypass the matching process entirely and are scrutinised heavily by auditors.

3. The same exception resolved more than once

In high-volume environments where multiple teams manage overlapping accounts, duplicate adjustments can slip through. They may net to zero on the surface, but they introduce distortions that can be difficult to undo later.

4. Spreadsheet version issues

When reconciliations live in multiple files across multiple people's desktops, version control is even more challenging. If an approval is based on an outdated version of the file, that reconciliation cannot be considered clean and can lead to misstatements.

5. Legacy and homegrown systems that can’t keep up

Older or custom-built reconciliation tools often fail under high transaction volumes. They lack proper approval workflows and produce outputs that don't integrate well with audit review tools. This ends up leading to more manual work.

6. Incomplete reconciliation coverage

If a payment rail, sub-ledger, or entity falls outside your standard reconciliation scope, it can be flagged by your auditor as an imbalance. The challenge here is that coverage gaps can stay invisible until before the audit.

Measuring Audit Reconciliation Performance

As the saying goes, if you can’t measure it, you can’t manage it. Audit reconciliation, too, needs to be measured for effectiveness. So, here are five metrics to help your team get started:

The Role of Automation in Audit Reconciliation

Automation can handle much of the heavy-lifting associated with audit reconciliation. Here’s how it can help you:

1. Automated Data Ingestion: It can automatically pull data from all of your source systems without you spending hours manually downloading files and juggling formats. Every data point is timestamped and automatically logged.

2. High-Speed Transaction Matching: It applies configurable matching rules across millions of records in seconds. This leaves your team with enough time to handle genuine exceptions.

3. Structured Exception Workflows: Advanced reconciliation automation tools like Osfin also come with systems to flag, categorise and route exceptions to the correct team. You can set escalation rules in advance so that no exception is left unhandled.

4. Enterprise Controls and Audit Logs: Automation tools also give you enterprise-level controls like role-based access, approval workflows and period locking. They may also allow you to create audit logs that auditors can then use for their reviews.

Improving Audit Reconciliation Before Automation

Automation can be very helpful, but only if your actual process is already clean. Without a clean process, layering on tech will make your reconciliation even messier instead of fixing it. Here’s what you need to get right before onboarding any tools:

1. Structure your policies

You need to create documented policies for every account in scope. There should be written documentation that mentions how often an account gets reconciled, what an exception is, and who approved it. This maintains consistency even when different people handle reconciliation.

2. Assign clear owners and keep the roles separate

Every reconciliation needs a named preparer and a separate named approver. If the same person does both, that’s not a control, and auditors will flag it. There also needs to be one person responsible for the overall picture of your reconciliation workflow.

3. Create documentation and evidence guidelines

You need to set standards for documentation to be maintained and how evidence needs to be filed. Without this, finding the right document or matching evidence to an exception can become extremely challenging at high volumes.

How Enterprise Platforms Like Osfin Help in Audit Reconciliation

For your business to benefit from the automation capabilities we discussed above, you need the right platform to support your efforts. Osfin is built to handle financial and payment reconciliation at enterprise scale and deliver audit-ready outputs without any extra manual effort from your team.

Here’s what Osfin offers:

1. Data Ingestion

Osfin is file format agnostic. It doesn’t matter how your source systems export data or what structure they use. With 170+ integrations, it connects directly to payment processors, ERPs, card networks, and other financial platforms to pull data automatically.

At the point of ingestion, Osfin applies custom deviation tolerances to filter out poor-quality data before it enters the reconciliation process. It also detects duplicates and outliers automatically before they create downstream exceptions.

2. The Reconciliation Process

Osfin uses logic-based matching rules that your team configures and controls. It handles many-to-one, one-to-many, and multi-way reconciliations, including two-way, three-way, four-way, and five-way matches, covering the full range of payment and financial reconciliation scenarios businesses actually deal with.

At scale, it reconciles 30 million records in 15 minutes. It also auto-reconciles payment gateway reports with commission, tax, and fee breakdowns. Osfin easily handles the kind of complex, multi-line settlement data that tends to create the most manual work in finance teams.

3. Exception Handling

Unmatched transactions are automatically flagged with an accurate reason code, then routed to the right team member through Osfin’s built-in ticketing and exception handling engine. Live dashboards can also show match status, exposure, and exception queues in real time.

4. Audit-Ready Output

At the end of every reconciliation cycle, Osfin delivers a compliance report with complete transaction history and end-to-end traceability. Every step is logged and auditable. This is what auditors actually ask for, and it’s produced automatically rather than assembled by hand.

All of your data is secured with 256-bit encryption, and access is controlled through maker-checker workflows, role-based permissions, and two-factor authentication. Osfin is compliant with SOC 2, PCI DSS, ISO 27001, and GDPR, which are important standards in enterprise and regulated environments.

{{banner1}}

Frequently Asked Questions

1. What is audit reconciliation?

Audit reconciliation is the process of comparing and verifying your financial records across multiple sources to confirm that every transaction is recorded accurately. It also checks that every record is fully supported by external evidence and is defensible under external audit scrutiny.

2. What is the difference between audit reconciliation and bank reconciliation?

Bank reconciliation compares a single account's internal ledger against a bank statement. Audit reconciliation is broader in scope and higher in rigor as it spans multiple accounts, systems, and data sources. It also requires documented evidence for every exception.

3. Why do auditors flag reconciliation issues?

Auditors flag reconciliation issues because incomplete, untimely, or unsupported reconciliations undermine the reliability of financial statements. Incompleteness in your records is usually taken as a signal of a lack of proper control in your financial statements.

4. How often should reconciliations be performed?

Frequency should be risk-based. High-risk and high-volume accounts, particularly cash, payment clearing, and customer liability accounts, should be reconciled daily or in real time. Lower-risk accounts may be reconciled weekly or monthly.

5. What controls are required for audit-ready reconciliation?

Core controls required for reconciliation would be written policies for every account in scope, named preparers and approvers with proper segregation of duties, clear standards for what counts as acceptable evidence, formal escalation rules for aged exceptions, period locking to prevent retroactive changes, and an immutable log of every action taken.

6. Can reconciliation automation reduce audit risk?

Yes, when it's implemented correctly. Automated platforms eliminate data collection errors, speed up matching to keep exception volumes manageable, enforce structured exception workflows that leave a proper paper trail, and generate audit-grade documentation without any extra effort.

7. Is audit reconciliation only relevant during year-end audits?

No, this is a common and costly misconception. Audit reconciliation matters year-round. Its value comes from maintaining accuracy and catching problems continuously, not just in the weeks before an auditor walks in.