Reconciliation in Accounting: Meaning, Process & Examples (2026 Guide)

You can call the reconciliation process the bedrock of accounting control. Banks and other financial institutions depend on it to verify internal records against the external statements to highlight and fix the discrepancies promptly. It safeguards financial accuracy, ensures compliance, and significantly impacts stakeholders' decision-making.

In this article, you explore what reconciliation in accounting is, its types, the entire process and the best practices for a successful close.

What is Reconciliation in Accounting?

Reconciliation in accounting is the process of comparing, verifying and resolving any existing discrepancies from two sets of financial records, like the bank's internal ledger against external statements from payment gateways and card networks. This verification process helps you ensure accuracy by going beyond bank accounts to include credit card settlements and subledgers critical for financial institutions.

Banks and financial institutions deal with high-volume transactions that need a reliable reconciliation process to identify errors, fraud, or timing mismatches to maintain the integrity of financial records required for regulatory purposes.

Why Reconciliation is Important in Accounting?

Reconciliation in accounting builds a solid foundation for reliable reporting. Banks, card providers and treasury services rely on reconciliation in accounting to make sure financial records are accurate.

Ensuring Accuracy of Financial Records

Balance sheets have a high probability of being riddled with discrepancies, and this can lead to wrong asset values or hidden losses. Such errors can harm the financial institution by confusing leaders and investors, resulting in poor decisions on bad data, like overcommitting cash. That's why reconciliation is needed: it helps you identify and fix such errors in the face of the challenging volume of daily transactions.

Detecting Errors and Irregularities

Some sources of discrepancies are manual processes, timing gaps or posting errors. Reconciliation in accounting helps treasury services spot duplicates, fraud or unrecorded fees quickly. This helps you catch and mitigate the damage before it spreads to the high-volume flow of transactions.

Supporting Audits and Compliance

Reconciliation helps you to prepare clear audit trails that are necessary for auditors. It proves that your financial operations align with standards like US SOX controls, India’s Companies Act, 2013, and GCC's SAMA/DFSA rules. And it helps you avoid fines by showing the matched, reconciled records. Such proofs are a must for treasury services to confidently close books and meet deadlines with complete traceability.

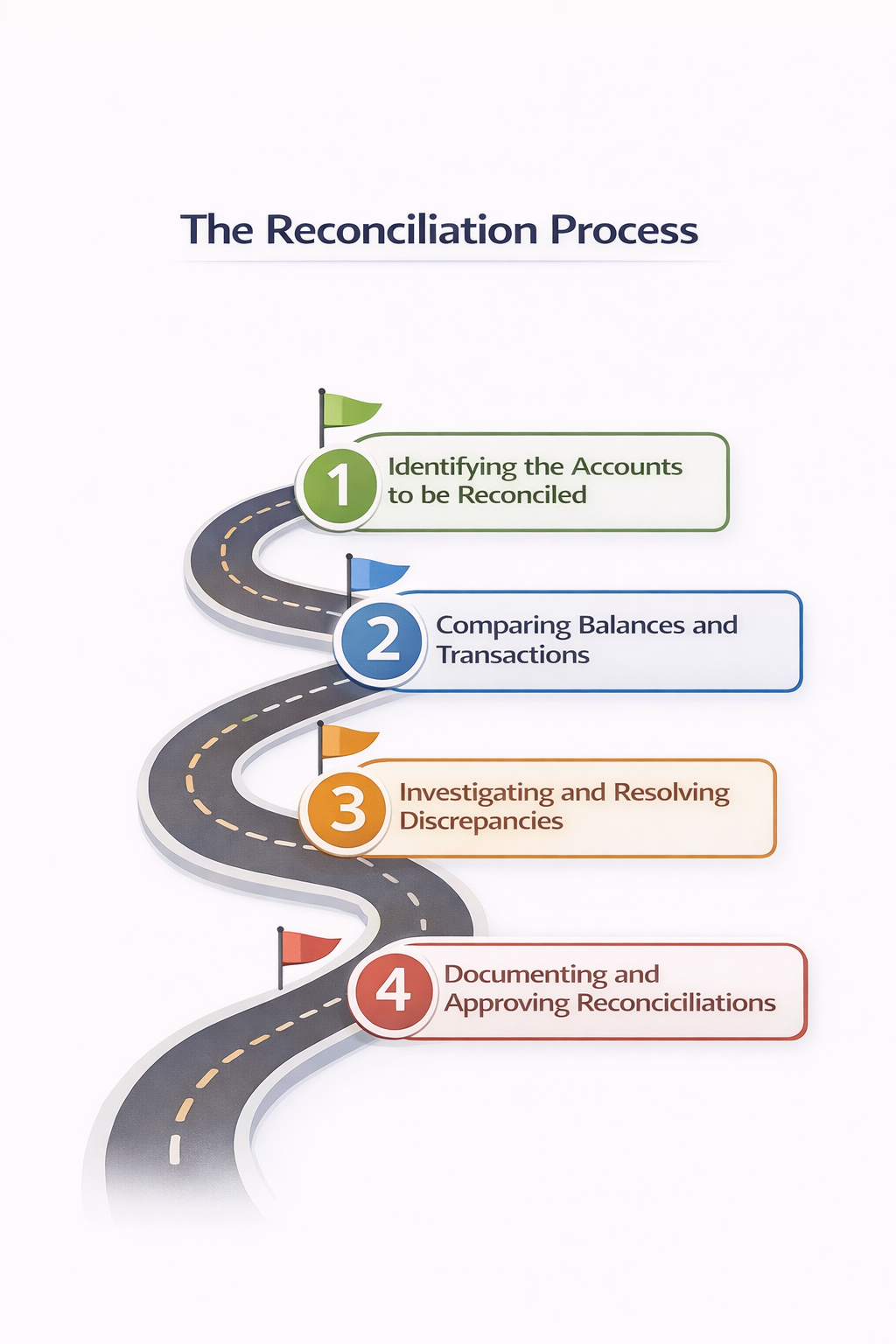

How does the Reconciliation Process Work?

The reconciliation process handles high-volume, complex transaction records, but it is simple to understand. You start by gathering data, performing transaction matching, fixing issues, and ending with documentation.

1. Identifying the Accounts to be Reconciled

You have to begin by choosing your sources for gathering transaction data. These can include key accounts like cash or treasury positions, and you need to compare them with external sources such as bank feeds or vendor bills. Banks might focus on high-risk treasury accounts at this step.

Osfin streamlines this process as a file-format agnostic platform that supports over 170 integrations for collecting transaction data from multiple sources. It also implements custom deviation tolerances to clean poor data, detect duplicates and outliers before pushing the data to the reconciliation process.

2. Comparing Balances and Transactions

All balances and details should be matched line by line, and any unmatched deposits should be flagged. You should consider an automation tool that supports logic-based rules for handling complex transaction matching.

For many-to-one, one-to-many, and 2/3/4/5-way reconciliation cases, Osfin offers logic-based matching. It processes 30 million records in 15 minutes at 100% accuracy by auto-reconciling payment gateways, breaking down commissions, taxes and fees.

3. Investigating and Resolving Discrepancies

All the flagged errors need adjustments or corrections for traceability and accuracy when you are closing the books. You can use Osfin to automate exception handling by raising a 'ticket' for errors with clear reasons and redirecting it to the responsible team for resolution. It also offers live dashboards that show match status, exposure, and queues in real time.

4. Documenting and Approving Reconciliations

It is necessary to log every step of the reconciliation process in accounting. You also need to attach proofs and like sign-offs for creating audit trails for compliance.

{{banner1}}

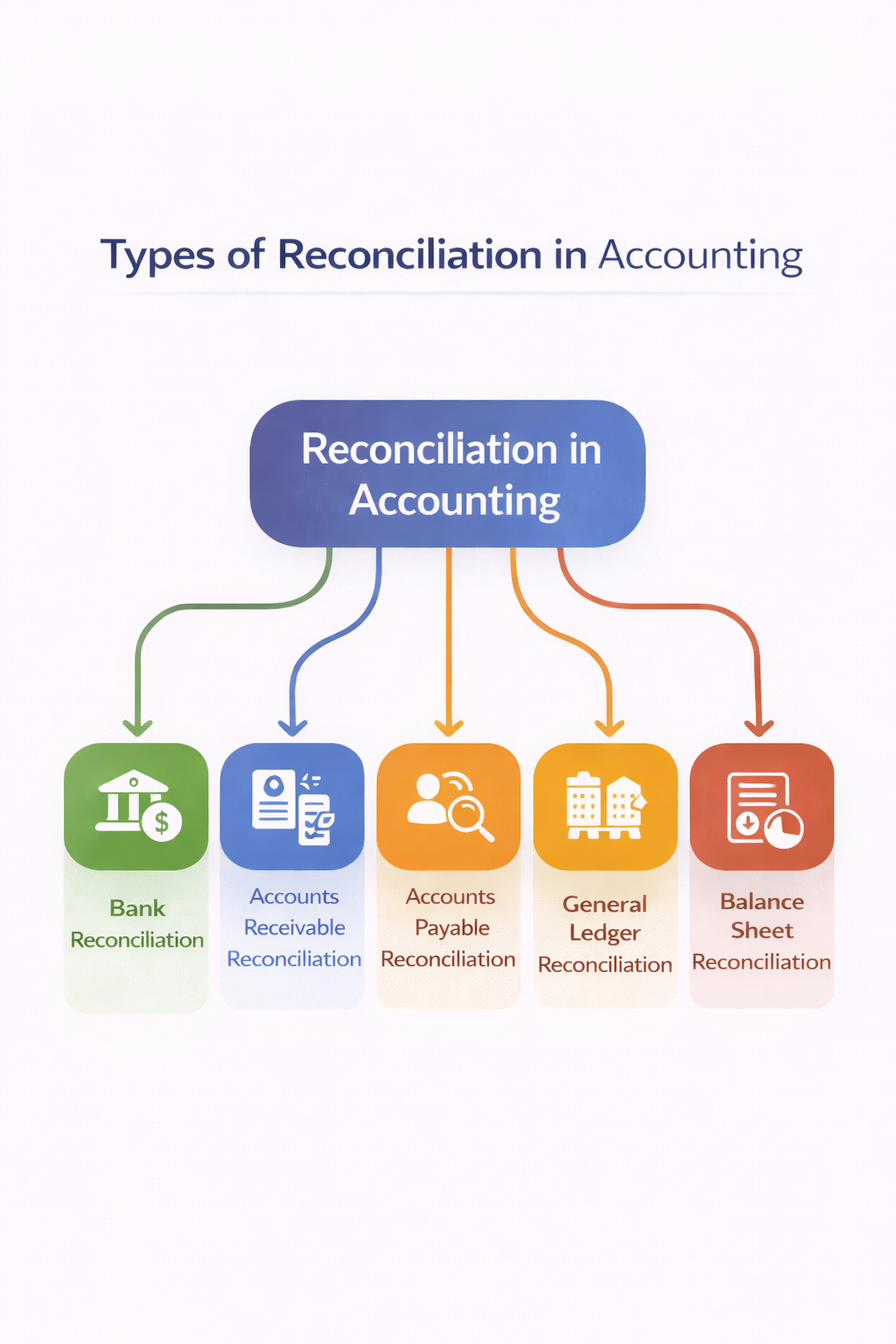

What are the Types of Reconciliation in Accounting?

Reconciliation is an essential process across financial institutions. And there are a variety of types tailored to specific accounts. You need to pick the right one to match operations and needs like cash flow or customer balances.

1. Bank Reconciliation

In this, you match your books to bank statements. Adjustments are made for deposits in transit or any outstanding checks. It is a daily process banks use to track liquidity.

2. Accounts Receivable Reconciliation

Here, the reconciliation is performed by matching customer invoices and payments with your ledger. If any overdues or disputed items are flagged, they will be resolved at the earliest. Card providers mostly perform accounts receivable reconciliation to manage credit risks.

3. Accounts Payable Reconciliation

In accounts payable reconciliation, you need to compare vendor bills to your records. Look for any flagged issues, like overpayments or misses, to resolve. Treasury teams perform this type of reconciliation to ensure accuracy in supplier pays.

4. General Ledger Reconciliation

In general ledger reconciliation, all the sub-ledgers are synced to the main ledger. You need to fix inter-account mismatches to ensure the overall books are balanced.

5. Balance Sheet Reconciliation

This type of reconciliation is performed at the period end. And you need to verify assets, liabilities, and equity to confirm if everything ties out. All regulated firms close their reconciliation in accounting with this step.

What is the Ideal Timing and Frequency of Reconciliation?

The timing and frequency of reconciliation depend on risk and volume of the transactions. Banks often focus on high-stakes accounts, while other financial institutions stick to routine checks to keep everything current without any overload.

Daily, Monthly, or Periodic

If you identify any potential fraud in transactions, you need to run daily checks on cash and card transactions.

Month-End or Year-End

Month-end reconciliation ties the close periodically, and the year-end reconciliation helps you prepare for audits. Both types lock books quickly to verify that all positions are clean.

Ownership and Accountability

You need to allocate tasks like reviewing and ownership of various stages in reconciliation across teams. This helps to boost control in financial firms.

What are Some Common Reconciliation Issues?

Reconciliation in accounting is about dealing with high-risk accounts and high-volume transactions. This entire process is prone to errors, and here are some common reconciliation issues like timing gaps, manual errors and missing details.

Timing Differences

You can see this issue when there are delayed bank postings or deposits that are still in transit. These errors can misstate monthly reports, and banks combat this by conducting frequent checks on cash accounts.

Data Entry Errors

Manual data entry can lead to errors such as duplicates, omissions, or incorrect postings. These slip-ups can throw the ledgers out of balance, and card providers need to be alert to spot them to avoid any customer disputes.

Missing Documentation

Some balances may lack supporting invoices or statements. And auditors generally label them as 'unsupported' during reviews. That's why you must always attach proofs with each transaction entry.

Unreconciled Balances

All the unmatched items accumulate into compounded risks. This might also look like hidden fraud and can cause delays in closings and raise red flags for financial operations. You need to clear them promptly to avoid unnecessary piling of errors.

{{banner1.1}}

Best Practices for Effective Reconciliation

Simple changes and steps in the reconciliation process can help you reduce errors and speed up closings. Here are some best practices you can implement for effective reconciliation in accounting.

Standardized Procedures

Uniform templates and checklists can help you standardize reconciliation procedures. You also need to train your staff on the rules.

Clear Documentation for Audit Trails

All transaction matches should be recorded with proof. This helps to bring traceability in audits and is non-negotiable for compliance.

Regular Review and Exception Management

Daily prioritizing of exceptions and peer reviews is helpful for the resolution process. This also helps to clear the queues faster.

Continuous Improvement of Reconciliation Processes

You should also analyze patterns in the process, look out for what processes are repetitive, and whether they can be automated. Accordingly, upgrade to industry-specific, trustworthy automation tools annually.

Conclusion

Reconciliation in accounting drives trust through accurate records, effective compliance and reliable financial data to make management-level decisions. It is a must if your financial institution wants to lead in regulated markets.

Osfin makes this effortless by offering automation features in every step of the reconciliation process. More than a perfect automation tool, it acts as your partner that guarantees 100% accuracy and can reconcile 30 million records in 15 minutes.

To streamline reconciliations of all types, schedule a free demo with Osfin today!

FAQs

1. What is reconciliation in accounting?

In accounting, reconciliation is a core process in which you compare two sets of financial records to ensure they match. And if any discrepancies are identified, then an investigation and adjustments are performed to prevent errors and fraud.

2. Why is reconciliation important in accounting?

Reconciliation is important in accounting because it ensures accuracy in financial records, in both internal ledgers and external bank statements. Through this process, we also catch errors and inconsistencies to prevent fraud.

3. What accounts should be reconciled regularly?

Accounts such as tax accounts, cash/bank accounts, credit cards, loans, and investments should be reconciled regularly. Always prioritize high-risk items and high-volume transactions for regular reconciliation to avoid errors and fraud.

4. What is the difference between reconciliation and adjustment?

Reconciliation is the overall process of comparing two sets of financial records. At the same time, adjustments are the necessary actions that are performed, mostly journal entries, to correct the discrepancies uncovered during the transaction matching.

5. How often should reconciliations be performed?

You can perform accounts reconciliations weekly, daily or even continuous reconciliation. But a healthy exercise is to perform reconciliation daily, especially for high-volume transactions and high-risk accounts.